Target 2014 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2014 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

|

|

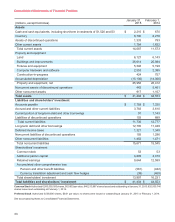

final liquidation value of the Canada Subsidiaries and may vary significantly from our current estimates. See Note 6

of the Financial Statements for further information.

Insurance/self-insurance: We retain a substantial portion of the risk related to certain general liability, workers'

compensation, property loss and team member medical and dental claims. However, we maintain stop-loss coverage

to limit the exposure related to certain risks. Liabilities associated with these losses include estimates of both claims

filed and losses incurred but not yet reported. We use actuarial methods which consider a number of factors to estimate

our ultimate cost of losses. General liability and workers' compensation liabilities are recorded at our estimate of their

net present value; other liabilities referred to above are not discounted. Our workers' compensation and general liability

accrual was $566 million and $576 million at January 31, 2015 and February 1, 2014, respectively. We believe that

the amounts accrued are appropriate; however, our liabilities could be significantly affected if future occurrences or

loss developments differ from our assumptions. For example, a 5 percent increase or decrease in average claim costs

would impact our self-insurance expense by $28 million in 2014. Historically, adjustments to our estimates have not

been material. Refer to Item 7A, Quantitative and Qualitative Disclosures About Market Risk, for further disclosure of

the market risks associated with these exposures. We maintain insurance coverage to limit our exposure to certain

events, including network security matters. Since the Data Breach, we have recognized $90 million of expected

insurance recoveries related to the Data Breach. As of January 31, 2015, we have a $60 million insurance-recovery

receivable relating to the Data Breach because we believe recovery is probable. However, it is possible that the

insurance carriers could dispute our claims and that we may be unable to collect the recorded receivable.

Income taxes: We pay income taxes based on the tax statutes, regulations and case law of the various jurisdictions

in which we operate. Significant judgment is required in determining the timing and amounts of deductible and taxable

items, and in evaluating the ultimate resolution of tax matters in dispute with tax authorities. The benefits of uncertain

tax positions are recorded in our financial statements only after determining it is likely the uncertain tax positions would

withstand challenge by taxing authorities. We periodically reassess these probabilities, and record any changes in the

financial statements as appropriate. Liabilities for uncertain tax positions, including interest and penalties, were

$195 million and $241 million at January 31, 2015 and February 1, 2014, respectively. We believe the resolution of

these matters will not have a material adverse impact on our consolidated financial statements. Income taxes are

described further in Note 21 of the Financial Statements.

Pension and postretirement health care accounting: We maintain a funded qualified, defined benefit pension plan,

as well as several smaller and unfunded nonqualified plans and a postretirement health care plan for certain current

and retired team members. The costs for these plans are determined based on actuarial calculations using the

assumptions described in the following paragraphs. Eligibility and the level of benefits varies depending on team

members' full-time or part-time status, date of hire and/or length of service. The benefit obligation and related expense

for these plans are determined based on actuarial calculations using assumptions about the expected long-term rate

of return, the discount rate and compensation growth rates. The assumptions used to determine the period-end benefit

obligation also establish the expense for the next year, with adjustments made for any significant plan or participant

changes.

Our expected long-term rate of return on plan assets of 7.5 percent is determined by the portfolio composition, historical

long-term investment performance and current market conditions. Our compound annual rate of return on qualified

plans' assets was 12.1 percent, 8.3 percent, 7.0 percent and 9.7 percent for the 5-year, 10-year, 15-year and 20-year

periods, respectively. A one percentage point decrease in our expected long-term rate of return would increase annual

expense by $31 million.

The discount rate used to determine benefit obligations is adjusted annually based on the interest rate for long-term

high-quality corporate bonds, using yields for maturities that are in line with the duration of our pension liabilities. Our

benefit obligation and related expense will fluctuate with changes in interest rates. A 0.5 percentage point decrease

to the weighted average discount rate would increase annual expense by $29 million.

Based on our experience, we use a graduated compensation growth schedule that assumes higher compensation

growth for younger, shorter-service pension-eligible team members than it does for older, longer-service pension-

eligible team members.

Pension and postretirement health care benefits are further described in Note 26 of the Financial Statements.

Legal and other contingencies: We are exposed to other claims and litigation arising in the ordinary course of business

and use various methods to resolve these matters in a manner that we believe serves the best interest of our

shareholders and other constituents. When a loss is probable, we record an accrual based on the reasonably estimable

loss or range of loss. When no point of loss is more likely than another, we record the lowest amount in the estimated

range of loss and disclose the estimated range. We do not record liabilities for reasonably possible loss contingencies,

but do disclose a range of reasonably possible losses if they are material and we are able to estimate such a range.

26