Toyota 2007 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2007 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

Other comprehensive income—

Other comprehensive income refers to revenues, expenses,

gains and losses that, under accounting principles generally

accepted in the United States of America are included in com-

prehensive income, but are excluded from net income as these

amounts are recorded directly as an adjustment to sharehold-

ers’ equity. Toyota’s other comprehensive income is primarily

comprised of unrealized gains/losses on marketable securities

designated as available-for-sale, foreign currency translation

adjustments and adjustments attributed to minimum pension

liabilities associated with Toyota’s defined benefit pension

plans.

Accounting changes—

In November 2004, the Financial Accounting Standard Board

(“FASB”) issued FAS No. 151, Inventory Costs – an amendment

of ARB No. 43, Chapter 4 (“FAS 151”). FAS 151 amends the

guidance in Accounting Research Bulletin (“ARB”) No. 43,

Chapter 4 (“ARB 43, Chapter 4”), Inventory Pricing, to clarify the

accounting for abnormal amounts of idle facility expense,

freight, handling costs, and wasted material (spoilage).

Paragraph 5 of ARB 43, Chapter 4, previously stated that “. . .

under some circumstances, items such as idle facility expense,

excessive spoilage, double freight, and rehandling costs may

be so abnormal as to require treatment as current period

charges. . . .” FAS 151 requires that those items be recognized

as current-period charges regardless of whether they meet the

criterion of “so abnormal.” In addition, this Statement requires

that allocation of fixed production overheads to the costs of

conversion be based on the normal capacity of the production

facilities. Toyota adopted FAS 151 effective for inventory costs

incurred during fiscal year begun after June 15, 2005. The adop-

tion of FAS 151 did not have material impact on Toyota’s con-

solidated financial statements.

In December 2004, FASB issued FAS 123(R). FAS 123(R) is a

revision of FAS 123 and supersedes APB 25 and its related

implementation guidance. FAS 123(R) requires a public entity to

measure the cost of employee services received in exchange for

an award of equity instruments based on the grant-date fair

value of the award. That cost will be recognized over the period

during which an employee is required to provide service in

exchange for the award. FAS 123(R) also requires a public entity

102 ANNUAL REPORT 2007

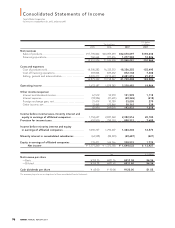

Net income per share—

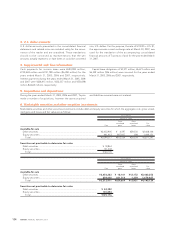

Basic net income per common share is calculated by dividing

net income by the weighted-average number of shares out-

standing during the reported period. The calculation of diluted

net income per common share is similar to the calculation of

basic net income per share, except that the weighted-average

number of shares outstanding includes the additional dilution

from the assumed exercise of dilutive stock options.

Stock-based compensation—

Toyota measures compensation expense for its stock-based

compensation plan based on the grant-date fair value of the

award from the fiscal year beginning on April 1, 2006. Toyota

accounts for the stock-based compensation plans in accordance

with FAS No. 123(R), Share – Based Payment (revised 2004)

(“FAS 123(R)”).

Prior to the adoption of FAS 123(R), Toyota measured com-

pensation expense using the intrinsic value method under the

recognition and measurement principles of the Accounting

Principles Board (“APB”) Opinion No. 25 (“APB 25”), Accounting

for Stock Issued to Employees, and related Interpretations. No

stock-based compensation expense was reflected in net

income, as all options granted under Toyota’s stock-based

compensation plan had an exercise price higher than the mar-

ket value of the underlying common stock on the date of grant.

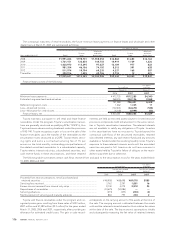

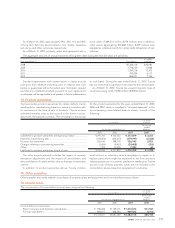

The following table illustrates the effect on net income and

earnings per share for the prior years to the adoption of FAS

123(R) that ended March 31, 2005 and 2006, if the company had

applied the fair value recognition provisions of FAS No. 123,

Accounting for Stock-Based Compensation (“FAS 123”), to

stock-based employee compensation. See note 18 to the con-

solidated financial statements for weighted-average assump-

tions used in option pricing model.

Yen in millions

For the years ended March 31,

2005 2006

Net income

As reported............................................................................................................................................... ¥1,171,260 ¥1,372,180

Deduct: Total stock-based compensation expenses determined

under fair value based method for all awards, net of related tax effects...................................... (1,571) (1,449)

Pro forma .................................................................................................................................................. ¥1,169,689 ¥1,370,731

Net income per share

—Basic As reported............................................................................................................. ¥355.35 ¥421.76

Pro forma ................................................................................................................ 354.87 421.32

—Diluted As reported.............................................................................................................¥355.28 ¥421.62

Pro forma ................................................................................................................ 354.80 421.18