Toyota 2007 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2007 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

86 ANNUAL REPORT 2007

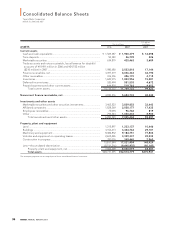

receivables through special purpose entities and obtained pro-

ceeds from securitization transactions, net of purchased and

retained interests totaling ¥69.0 billion during fiscal 2007.

Marketable securities and other securities investments,

including those included in current assets, increased during fiscal

2007 by ¥227.9 billion, or 5.6%, to ¥4,265.3 billion, primarily

reflecting the increase of U.S. treasury notes held by a subsidiary

in North America, and Japanese government bonds held by the

parent company.

Property, plant and equipment increased during fiscal 2007

by ¥993.9 billion, or 14.1%, primarily reflecting an increase in capital

expenditures which was partially offset by the depreciation

charges during the year.

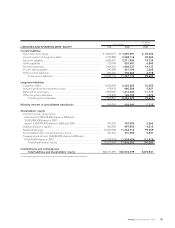

Accounts payable increased during fiscal 2007 by ¥125.0

billion, or 6.0%, reflecting the impact of increased trading volumes

and the impact of fluctuations in foreign currency translation rates.

Accrued expenses increased during fiscal 2007 by ¥204.1

billion, or 13.9%, reflecting the increase in expenses due to the

expansion of the business.

Income taxes payable increased during fiscal 2007 by ¥73.7

billion, or 21.2%, principally as a result of the increase in taxable

income.

Toyota’s total borrowings in-

creased during fiscal 2007 by

¥1,731.7 billion, or 16.7%. Toyota’s

short-term borrowings consist of

loans with a weighted-average

interest rate of 3.17% and commer-

cial paper with a weighted-average

interest rate of 4.95%. Short-term

borrowings increased during fiscal

2007 by ¥464.3 billion, or 15.3%, to

¥3,497.3 billion. Toyota’s long-term

debt consists of unsecured and

secured loans, medium-term notes,

unsecured notes and long-term

capital lease obligations with inter-

est rates ranging from 0.01% to

18.00%, and maturity dates ranging

from 2007 to 2047. The current por-

tion of long-term debt increased

during fiscal 2007 by ¥644.3 billion, or 37.4%, to ¥2,368.1 billion

and the non-current portion increased by ¥623.1 billion, or 11.0%,

to ¥6,263.5 billion. The increase in total borrowings reflects the

expansion of the financial services operations. At March 31, 2007,

approximately 39% of long-term debt was denominated in U.S.

dollars, 24% in Japanese yen, 11% in euros and 26% in other cur-

rencies. Toyota hedges fixed rate exposure by entering into

interest rate swaps. There are no material seasonal variations in

Toyota’s borrowings requirements.

As of March 31, 2007, Toyota’s total interest bearing debt

was 102.5% of total shareholders’ equity, compared to 98.5% as

of March 31, 2006.

Toyota’s long-term debt was rated “AAA” by Standard &

Poor’s Ratings Group, “Aaa” by Moody’s Investors Services and

“AAA” by Rating and Investment Information, Inc. as of March

31, 2007. These ratings represent the highest long-term debt rat-

ings published by each of the respective rating agencies. A credit

rating is not a recommendation to buy, sell or hold securities. A

credit rating may be subject to withdrawal or revision at any time.

Each rating should be evaluated separately of any other rating.

Toyota’s treasury policy is to maintain controls on all expo-

sures, to adhere to stringent counterparty credit standards, and

to actively monitor marketplace exposures. Toyota remains cen-

tralized, and is pursuing global efficiency of its financial services

operations through Toyota Financial Services Corporation.

The key element of Toyota’s financial policy is maintaining a

strong financial position that will allow Toyota to fund its research

and development initiatives, capital expenditures and financing

operations on a cost effective basis even if earnings experience

short-term fluctuations. Toyota believes that it maintains suffi-

cient liquidity for its present requirements and that by maintain-

ing its high credit ratings, it will continue to be able to access

funds from external sources in large amounts and at relatively low

costs. Toyota’s ability to maintain its high credit ratings is subject

to a number of factors, some of which are not within Toyota’s

control. These factors include general economic conditions in

Japan and the other major markets in which Toyota does busi-

ness, as well as Toyota’s successful implementation of its busi-

ness strategy.

Toyota’s unfunded pension liabilities decreased during fiscal

2007 by ¥24.2 billion, or 7.9% to ¥282.5 billion. The unfunded

pension liabilities relate primarily to the parent company and its

Japanese subsidiaries. The unfunded amounts will be funded

through future cash contributions by Toyota or in some cases will

be funded on the retirement date of each covered employee.

The unfunded pension liabilities decreased in fiscal 2007 com-

pared to the prior year mainly due to cash contributions to the

plans and the increase in the market value of plan assets. See

note 19 to the consolidated financial statements.

Off-Balance Sheet Arrangements

■Securitization Funding

Toyota uses its securitization program as part of its funding for its

financial services operations. Toyota believes that the securitiza-

tions are an important element of its financial services operations

as it provides a cost-effective funding source.

Securitization of receivables allows Toyota to access a highly

liquid and efficient capital market while providing Toyota with an

alternative source of funding and investor diversification. See

note 7 to the consolidated financial statements with respect to

the impact on the balance sheet, income statement, and cash

flows of these securitizations.

Toyota’s securitization program involves a two-step transac-

tion. Toyota sells discrete pools of retail finance receivables to a

wholly-owned bankruptcy remote special purpose entity (“SPE”),

which in turn transfers the receivables to a qualified special purpose

12,000 80

6,000 40

3,000 20

9,000 60

00

Shareholders’ Equity

and Equity Ratio

(¥ Billion) (%)

FY ’04’03 ’05 ’06 ’07

Equity ratio (Right scale)