Toyota 2007 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2007 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

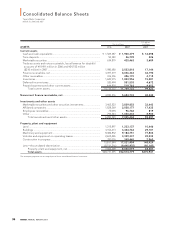

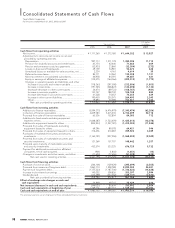

90 ANNUAL REPORT 2007

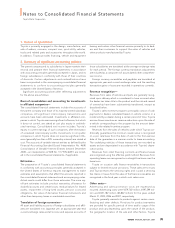

In September 2006, FASB issued FAS No. 157, Fair Value

Measurements ("FAS 157"), which defines fair value, establishes a

framework for measuring fair value and expands disclosures

about fair value measurements. FAS 157 is effective for financial

statements issued for fiscal year beginning after November 15,

2007 and interim period within the fiscal year. Management is

evaluating the impact of adopting FAS 157 on Toyota’s consoli-

dated financial statements.

In September 2006, FASB issued FAS No. 158, Employers’

Accounting for Defined Benefit Pension and Other

Postretirement Plans—an amendment of FASB Statements No.

87, 88, 106, and 132(R) ("FAS 158"). FAS 158 requires employers

to recognize the overfunded or underfunded status of their

defined benefit postretirement plans as an asset or a liability on

their balance sheets, and to recognize changes in that funded

status in the year in which the changes occur through compre-

hensive income. Toyota adopted the provisions regarding recog-

nition of funded status and disclosure under FAS 158 as of the

end of the fiscal year ending after December 15, 2006. See note

19 to the consolidated financial statements for the impact of the

adoption of the provisions on Toyota’s consolidated financial

statements. FAS 158 also requires employers to measure the

funded status of their defined benefit postretirement plans as of

the date of their year-end statement of financial position. This

provision in FAS 158 regarding a measurement date is effective

for fiscal year ending after December 15, 2008. Management is

evaluating the impact of adopting this provision on Toyota’s con-

solidated financial statements.

In February 2007, FASB issued FAS No. 159, The Fair Value

Option for Financial Assets and Financial Liabilities—Including an

amendment of FASB Statement No. 115 (“FAS 159”). FAS 159

permits entities to measure many financial instruments and certain

other assets and liabilities at fair value on an instrument-by-

instrument basis and subsequent change in fair value must be

recorded in earnings at each reporting date. FAS 159 is effective

for fiscal year beginning after November 15, 2007. Management

is evaluating the impact of adopting FAS 159 on Toyota’s consol-

idated financial statements.

In June 2006, FASB issued FASB Interpretation No. 48,

Accounting for Uncertainty in Income Taxes—an interpretation of

FASB Statement No. 109 (“FIN 48”). FIN 48 clarifies the account-

ing for uncertainty in tax positions and requires a company to

recognize in its financial statements, the impact of a tax position,

if that position is more likely than not to be sustained on audit,

based on the technical merits of the position. FIN 48 is effective

for fiscal year beginning after December 15, 2006. Management

is evaluating the impact of adopting FIN 48 on Toyota’s consoli-

dated financial statements.

Critical Accounting Estimates

The consolidated financial statements of Toyota are prepared in

conformity with accounting principles generally accepted in the

United States of America. The preparation of these financial

statements requires the use of estimates, judgments and

assumptions that affect the reported amounts of assets and liabil-

ities at the date of the financial statements and the reported

amounts of revenues and expenses during the periods present-

ed. Toyota believes that of its significant accounting policies, the

following may involve a higher degree of judgments, estimates

and complexity:

■Product Warranty

Toyota generally warrants its products against certain manufac-

turing and other defects. Product warranties are provided for

specific periods of time and/or usage of the product and vary

depending upon the nature of the product, the geographic loca-

tion of the sale and other factors. All product warranties are con-

sistent with commercial practices. Toyota provides a provision for

estimated product warranty costs as a component of cost of sales

at the time the related sale is recognized. The accrued warranty

costs represent management’s best estimate at the time of sale

of the total costs that Toyota will incur to repair or replace prod-

uct parts that fail while still under warranty. The amount of

accrued estimated warranty costs is primarily based on historical

experience as to product failures as well as current information

on repair costs. The amount of warranty costs accrued also con-

tains an estimate of warranty claim recoveries to be received

from suppliers. The foregoing evaluations are inherently uncer-

tain, as they require material estimates and some products’ war-

ranties extend for several years. Consequently, actual warranty

costs will differ from the estimated amounts and could require

additional warranty provisions. If these factors require a signifi-

cant increase in Toyota’s accrued estimated warranty costs, it

would negatively affect future operating results of the automo-

tive operations.

■Allowance for Doubtful Accounts and Credit Losses

• Natures of estimates and assumptions

Sales financing and finance lease receivables consist of retail

installment sales contracts secured by passenger cars and com-

mercial vehicles. Collectibility risks include consumer and dealer

insolvencies and insufficient collateral values (less costs to sell) to

realize the full carrying values of these receivables. As a matter of

policy, Toyota maintains an allowance for doubtful accounts and

credit losses representing management’s estimate of the amount

of asset impairment in the portfolios of finance, trade and other

receivables. Toyota determines the allowance for doubtful

accounts and credit losses based on a systematic, ongoing

review and evaluation performed as part of the credit-risk evalua-

tion process, historical loss experience, the size and composition

of the portfolios, current economic events and conditions, the

estimated fair value and adequacy of collateral and other perti-

nent factors. This evaluation is inherently judgmental and

requires material estimates, including the amounts and timing of

future cash flows expected to be received, which may be suscep-

tible to significant change. Although management considers the

allowance for doubtful accounts and credit losses to be adequate