APC 2003 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2003 APC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

|

|

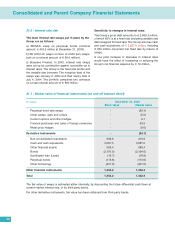

Consolidated and Parent Company Financial Statements

98

21.6 - Interest rate risk

The main interest rate swaps put in place by the

Group are as follows:

a) SEISAS: swap on perpetual bonds (notional

amount: €443.5 million at December 31, 2003).

b) SE (UK) Ltd: swaps on lines of credit (two swaps,

both on a notional amount of €58.9 million).

c) Boissière Finance: In 2003, interest rate swaps

were set up as a protection against a possible cut in

interest rates. The Group is the fixed rate lender and

the variable rate borrower. The inception date of the

swaps was January 2, 2004 and their expiry date is

July 4, 2004. The portfolio comprises two contracts

on a total notional amount of €800 million.

Sensitivity to changes in interest rates

The Group’s gross debt amounts to €2,688.3 million,

of which 85% is at a fixed rate (including variable rate

debt swapped for fixed rate. The Group also has cash

and cash equivalents of €3,087.5 million, including

€800 million converted into fixed rate by means of

swaps.

A one point increase or decrease in interest rates

would have the effect of increasing or reducing the

Group’s net financial expense by €19 million.

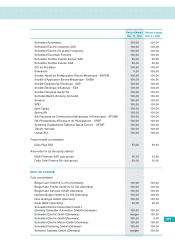

21.7 - Market value of financial instruments (on and off balance sheet)

(

€

millions)

December 31, 2003

Book value Market value

Perpetual bond rate swaps - (83.1)

Other swaps, caps and collars - (5.0)

Current options and other hedges - 9.1

Forward purchases and sales of foreign currencies - 63.9

Metal price hedges - (9.0)

Derivative instruments - (24.1)

Non-consolidated investments 369.6 416.9

Cash and cash equivalents 3,087.5 3,087.5

Other financial assets 585.4 585.4

Bonds (2,151.0) (2,194.0)

Syndicated loan (Lexel) (16.7) (18.8)

Perpetual bonds (113.6) (113.6)

Other borrowings (407.0) (407.0)

Other financial instruments 1,354.2 1,356.4

Total 1,354.2 1,332.3

The fair value of swaps is estimated either internally, by discounting the future differential cash flows at

current market interest rate, or by third party banks.

For other derivative instruments, fair value has been obtained from third-party banks.