APC 2003 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2003 APC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

|

|

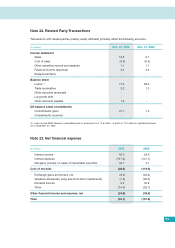

Note 16. Provisions for

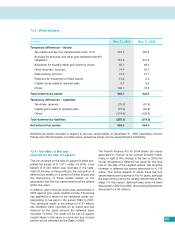

pensions and other post-retirement

benefit obligations

The Group has set up pension, life insurance, length-

of-service award and other post-retirement benefit

plans for its employees. These range from plans pro-

viding for the payment of a lump sum based on years

of service to supplementary pension plans and other

multi-employer plans.

Payments made under defined contribution plans are

recorded in the income statement, under operating

expense, in the year of payment and are in full set-

tlement of the Group’s liability.

The Group’s obligation for the payment of length-of-

service awards mainly concerns French companies

in the Group and is generally calculated based on

the seniority, grade and end-of-career salary of the

employees concerned.

For defined benefit plans, the accrued or prepaid

periodic pension cost is determined using the pro-

jected unit credit method and is recognized in accor-

dance with local accounting standards and tax rules

in the countries concerned. Where necessary, these

amounts are adjusted to comply with Group account-

ing policies.

Actuarial valuations are performed each year for the

main plans and at regular intervals for the other

plans. The assumptions used vary according to the

economic conditions prevailing in the country con-

cerned. Benefit obligations under defined benefit

plans mainly concern the Group’s North American

subsidiaries and are funded through payments to

external funds. The majority of plan assets are

invested in equities and bonds not issued by the

Group and, occasionally, in real estate.

16.1 - Provisions for pensions and

length-of-service awards

Annual changes in obligations, the market value of

investments and related assets and liabilities are

reflected in the consolidated balance sheet as fol-

lows:

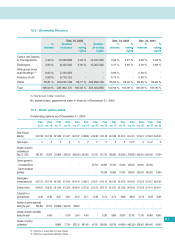

89

(

€

millions)

O/w US plans O/w US plans

Dec. 31, 2003

Dec. 31, 2003

Dec. 31, 2002

Dec. 31, 2002

1. Amounts recognized in the accounts

Other non-current assets 315.6

295.2

274.4

236.9

Deferred taxes 6.6 140.2

128.2

Provisions for pensions and

other post-retirement benefit obligations (407.5)

(13.3)

(521.6)

(160.1)

A

mounts recognized in the balance sheet

(85.3)

281.9

(107.0)

205.0

Comments on amounts recorded in the accounts of US subsidiaries:

In 2002, due to the sharp fall in the stock market indexes used as the benchmark for the majority of plan assets, the funded

status of the plans was determined based on the accumulated benefit obligation instead of the projected benefit obligation,

as was the case in the past. This led to the recognition of an additional minimum liability corresponding to the difference

between the fair market value of the plan assets and the accumulated benefit obligation at December 31, 2002.

Since the additional minimum liability was due to the deferral of actuarial losses and unrecognized prior service costs, an

equivalent amount, net of deferred taxes, was recorded on the assets side of the balance sheet under “Other non-current

assets” in the amount of

€

236.9 million net of deferred taxes.

In 2003, the Group paid an additional

€

143.3 million contribution to its US plans. As a result of this contribution and

the improved yield on plan assets, plan assets once again represented more than the accumulated benefit obligation.

The Group therefore wrote off the amount recorded under "Other non-current assets" in 2002 and reduced provisions for

pensions and other post-retirement benefits by the same amount, net of the deferred tax asset.