APC 2003 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2003 APC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

|

|

59

Other intangible assets declined by €11 million to

€271 million. Recognition of the Digital brand, in an

amount of €44 million, was offset by reclassifica-

tions under goodwill of differences arising on the

acquisition of autonomous business units, in an

amount of €59 million, and the negative impact of

currency fluctuations, in an amount of €15 million.

Property, plant and equipment (at cost) decreased by

€134 million to €1,439 million, due primarily to lower

capital spending in 2003 and a €93 million negative

currency effect.

Investments totaled €1,015 million, up €314 million

primarily as a result of the Clipsal acquisition.

Schneider Electric Australia Holding acquired shares

in Clipsal Australia for €185 million and in the joint

venture in Asia for €49 million. The Group also

assumed €259 million in debt and placed €32 mil-

lion in an escrow account to cover an additional pay-

ment due in 2007. The increase was partially offset

by a €223 decrease in non-consolidated invest-

ments following the consolidation of Digital

Electronics.

Other non-current assets include net actuarial gains

and losses and unamortized prior service costs on

pension obligations in the United States, in an

amount of €295 million. In 2003, the Group paid an

additional €143 million contribution to its US plans.

This increased plan assets and allowed the Group to

reduce provisions for pensions and other post-retire-

ment benefits.

Current assets

Current assets declined 2.9% to € 7,367 million and

represented 52.9% of total assets. The main compo-

nent, cash and cash equivalents, decreased by 4%

to € 3,087 million due to the financing of the TAC and

Clipsal acquisitions.

Inventories and work in process edged back 2% to

€1,124 million, while trade account receivables fell

by 1.7% to € 1,781 million.

Other accounts receivable and prepaid expenses

declined 10% to € 627 million due to a reduction in

tax receivables.

Deferred tax assets came to € 747 million, primarily

reflecting a deferred tax asset of € 464 million in

respect of the loss incurred on the sale of Legrand.

An initial deferred tax asset of € 453 million was rec-

ognized on this loss in 2002 and a further € 114 mil-

lion was recognized in 2003 following a change in

French tax rules concerning loss carryforwards. At

the same time, the € 97 million carryback credit rec-

ognized in 2002 was reclassified under "Prepaid and

recoverable taxes" in 2003.

At December 31, 2003, total cash and cash equiva-

lents stood at € 3,087 million compared with € 3,214

million the year before.

Since the end of 2002, following the divestment of its

Legrand shares, the Group has had a positive net

cash position. This position declined to € 398 million

at December 31, 2003 from € 844 million the year

before due to financing of the TAC and Clipsal acqui-

sitions (€ 452 million and € 404 million, respective-

ly), dividend payments (€ 326 million), share buy-

backs (€ 111 million), and a contribution to the US

pension plans (€ 143 million), partially offset by free

cash flow of € 989 million. Free cash flow equals

operating cash flow - net capital expenditure +/-

change in working capital.

Shareholders’ equity

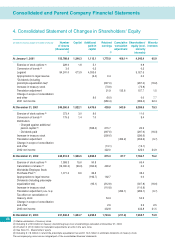

Shareholders’ equity (excluding minority interests)

totaled € 7,659 million, or 55% of the balance sheet

total. The € 126 million decrease over the year is the

net result of the following: capital increases in an

amount of € 102 million, income for the year of € 433

million, the dividend paid in 2002 (including pré-

compte equalization tax) in an amount of € 308 mil-

lion, changes in treasury stock in an amount of € 111

million, and a translation adjustment of € 299 million.

Minority interests were stable at € 75 million.

Provisions for contingencies and charges

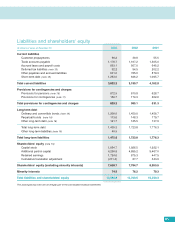

Provisions for contingencies and charges totaled

€829 million, or 6% of the balance sheet total.

Primarily comprising provisions for pensions and

similar benefits, they were down € 156 million from

the year before due to the above-mentioned € 143

million contribution to the US pension plans.

Long-term debt

Total long-term debt stood at € 1,435 million, or

10.3% of the balance sheet total. The € 289 million

decline from 2002 reflects reclassification of a € 951

million bond issue under short-term debt and a new

bond issue in an amount of € 750 million.

Other long-term liabilities, in an amount of € 40 mil-

lion, correspond to part of the acquisition price of

Clipsal (€ 8 million is due in 2004 and € 32 million in

2007).

Short-term debt

Short-term debt amounted to € 1,253 million, or 9%

of the balance sheet total. This item increased by

€607 million over the year, primarily due to the

reclassification of the € 951 million bond issue from

long-term debt and redemption of commercial paper

in an amount of € 335 million.