APC 2003 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2003 APC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

|

|

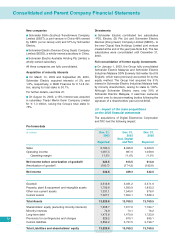

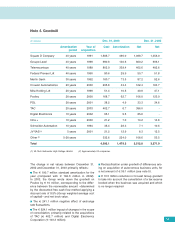

2.6 - Goodwill

Goodwill represents the excess of the cost of acqui-

sition over the fair value of assets acquired and lia-

bilities assumed at the date of acquisition. Goodwill

is amortized on a straight-line basis over the esti-

mated periods to be benefited not to exceed forty

years. When factors such as income, trends,

prospects and competition indicate that there may be

a potential loss in value in the related assets, the

Group evaluates if there is impairment of the value of

goodwill.

The specific indicator used to confirm the existence

and measure the amount of the impairment is

whether or not discounted cash flows from opera-

tions during the amortization period will be sufficient

to recover the carrying amount of the related assets.

2.7 - Intangible assets

Costs incurred by the Group in developing computer

software for internal use are generally expensed

when incurred. However for external and internal

costs related to implementing enterprise resource

planning (ERP) applications, such costs are deferred

and amortized over the period these applications are

used, which generally does not exceed five years.

Other intangible assets, other than brands, are amor-

tized on a straight-line basis over the periods to be

benefited or the period where such assets are pro-

tected by intellectual property laws.

2.8 - Property, plant and equipment

Land, buildings and equipment are recorded at cost.

Property, plant and equipment are depreciated on a

straight-line basis over the estimated useful lives of

the assets, as follows:

■Buildings 20 to 40 years

■Machinery and equipment 3 to 10 years

■Other 3 to 12 years

For operating fixed assets, the useful life is generally

defined as the period that is expected to benefit from

the operations of such fixed assets. However, when a

production line is scheduled to be halted or closed in

advance of the originally expected useful life, the

depreciation period is reduced.

When the Group enters into transactions that qualify

as capital leases, the leased assets are capitalized

and the related debt is recorded as a liability.

2.9 - Investments and marketable securities

Investments are reported at cost. Each year, the car-

rying value is compared to the recoverable amount

and the difference is recorded as an expense in the

consolidated statement of income.

The recoverable amount is determined by reference

to the Group’s equity in the underlying net assets, the

expected future profitability and business prospects

of the company and, in the case of listed securities,

the market value of the stock.

2.10 - Impairment of long-lived assets

For goodwill, an exceptional amortization charge is

recorded when the net book value exceeds the

recoverable amount, as measured by the discounted

free cash flow method.

For fixed assets including real estate and other non-

operating fixed assets, the Group has a policy of reg-

ularly reviewing the value of these assets for insur-

ance purposes and for comparison with market val-

ues of real estate. When those reviews show a per-

manent decline of market or insurance value over the

net book value, an impairment reserve is recorded

for the difference between the net book value and fair

value.

For other long-lived assets (including intangible

assets), management regularly receives third-party

appraisals, market valuations and other financial and

business based valuations. When these valuations

show a permanent reduction of the recoverable

amount over historical costs, impairment reserves

are taken or depreciation is recorded.

2.11 - Inventories and work in process

Inventories and work in process are stated at the

lower of cost (determined by the FIFO or weighted-

average methods) or estimated net realizable value.

The cost of work-in-process, semi-finished and fin-

ished products includes direct materials and labor

costs, subcontracting costs and production over-

head.

2.12 - Accounts receivable

An allowance for doubtful accounts is recorded when

it is probable that receivables will not be collected

and the amount is estimable. The identification of a

doubtful account as well as the related amount of the

provision are based on the analysis of our historical

experience of write-offs, the analysis of an aging

schedule, and a detailed assessment of specific

accounts receivable and related credit risks. Once it

is known with certainty that a doubtful account will

not be collected, the doubtful account and its related

allowance are written off against the reserve for

doubtful accounts.

Consolidated and Parent Company Financial Statements

68