APC 2003 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2003 APC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

|

|

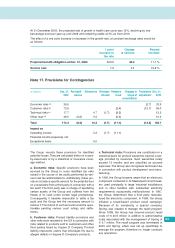

Note 17. Provisions for Contingencies

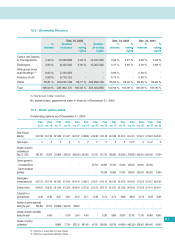

(

€

millions)

Dec. 31, Reclassifi- Allowances Releases Releases Changes in Translation Dec. 31,

2002 cations Unused Used scope of adjustment 2003

consolidation

Economic risks (a) 36.6 (2.7) 33.9

Customer risks (b) 73.5 (2.4) (12.1) 59.0

Technical risks (c) 17.7 4.7 (1.7) (8.2) 12.5

Other risks (d) 46.5 (0.2) 5.5 (0.5) 51.3

Total 174.3 (0.2) 10.2 (1.7) (11.1) (14.8) 156.7

Impact on

Operating income 5.2 (1.7) (11.1)

Financial income (expense), net

Exceptional items 5.0

93

The Group records these provisions for identified

potential losses. They are calculated either on a case-

by-case basis or by a statistical or insurance cover-

age method.

a. Economic risks: Specific provisions have been

accrued by the Group to cover identified tax risks

raised in the course of tax audits performed by vari-

ous local tax administrations. Additionally, these pro-

visions include a specific amount for the potential loss

on a receivable from a third party in connection with a

tax audit. The third party was in charge of liquidating

certain assets of the Group and suffered from the

freeze of its cash under certain legal proceedings.

Consequently, it became impossible to settle a tax

audit and the Group lent the necessary amount to

resolve it.The refund of such amounts could be ques-

tionable pending various court rulings and settle-

ments.

b. Customer risks: Product liability provisions and

other risks were recorded in the US in connection with

risks related to products sold to customers and other

third parties faced by Square D Company. Product

liability represents claims that individuals file due to

alleged defects in Square D Company’s products.

c. Technical risks: Provisions are constituted on a

statistical basis for product warranties beyond cover-

age provided by insurance. Such warranties rarely

exceed 12 months and are classified as accrued

expenses. The Group also recognizes technical risks

in connection with product development and manu-

facturing.

In 1996, the Group became aware that an electronic

component contained in its Masterpact circuit break-

ers used principally in large industrial installations

and in other facilities with substantial electricity

requirements occasionally malfunctioned. In 1997,

the Group determined that a third party manufac-

tured the electronic component. In 1998, the Group

initiated a broad-based product recall campaign.

Because of its complexity, a special company,

Spring, was created to manage the recall program.

Since 1998, the Group has incurred product recall

costs of € 40.9 million in addition to administrative

costs associated with the management of Spring of

€ 6.7 million. The recall program was terminated in

2003 and Spring, which was set up specifically to

manage the program, therefore no longer conducts

any operations.

At 31 December 2003, the projected rate of growth in health care costs was 12%, declining by one

percentage point per year up until 2009 and remaining stable at 5% as from 2010.

The effect of a one point increase or decrease in the growth rate, at constant exchange rates would be

as follows:

1 point Change Percent

increase in €millions increase

the rate

Projected benefit obligation at Dec. 31, 2003 460.6 46.2 11.1 %

Service cost 7.9 1.1 16.2 %