APC 2003 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2003 APC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

|

|

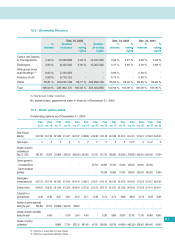

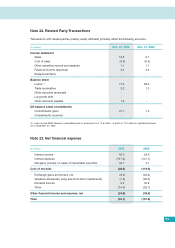

Note 21. Financial Instruments

The Group uses financial instruments to hedge its

exposure to risks related to fluctuations in interest

rates, currency rates and metal prices.

21.1 - Currency risk

Because of its international business base, the

Group is exposed to currency risk, notably when sub-

sidiaries carry out transactions in currencies other

than their functional currency. Currency risks on

operating receivables and payables are hedged by

means of forward sale contracts.

Currency risks on local currency intercompany loans

and borrowings are hedged using currency swaps.

21.2 - Interest rate risk

The Group chooses to issue fixed- or variable-rate

debt instruments depending on its overall exposure

and market conditions. To optimize financing costs,

and depending on market conditions, the Group

hedges its interest rate risk using swaps, caps and

floors and other financial instruments.

Interest rate swaps and other financial instruments

are also used to hedge interest rate risks on invest-

ments.

21.3 - Commodity price risk

In its manufacturing operations, the Group uses met-

als such as copper, silver, aluminum and nickel that

are traded on the commodity markets. The risk of

fluctuations in the market prices of these metals is

hedged using futures, swaps and options.

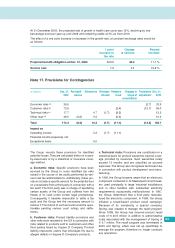

97

21.4 - Notional value of derivative

instruments (off-balance sheet)

(

€

millions)

Dec. 31, 2003 Dec. 31, 2002

Forward purchases

and sales of foreign

currencies

(note 21.5)

2,076.0 611.3

Interest rate swaps

(note 21.6)

1,360.4 568.7

Other currency

hedging instruments (1) 107.0 -

Currency options (1) 54.0 -

Metal price hedges –

futures 38.8 92.5

Metal price hedges –

options 0.4 10.3

Total derivative

instruments 3,636.6 1,282.8

(1) Hedges of 2004 operating cash flows

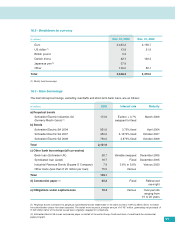

21.5 - Currency hedges

Forward hedging positions by currency

(

€

millions)

December 31, 2003

Sales Purchases Net

USD 814.8 1.5 813.3

JPY 160.4 24.3 136.1

AUD 375.1 375.1

SEK 291.7 5.5 286.2

DKK 123.9 33.6 90.3

CAD 89.4 89.4

GBP 68.9 20.7 48.2

CHF 55.1 0.6 54.5

ZAR 39.2 2.5 36.7

SGD 37.6 37.6

HKD 19.1 19.1

NOK 10.1 10.1

NZD 10.1 10.1

HUF 5.1 5.1

Other 64.2 64.2

Total 2,164.7 88.7 2,076.0

Currency hedges mainly concern intercompany

transactions and balances that are eliminated in con-

solidation.

The notional value of currency options is calculated

by adding together the absolute values of put and

call options. In the case of tunnels, the notional

amount is taken into account only once.

Forward currency hedging positions include

€1,482.1 million in hedges of intercompany loans

and borrowings and €593.9 million in hedges of

operating cash flows.

Sensitivity to changes in exchange rates

A 1% change in the exchange rate against the euro

of the US dollar, the Hong Kong dollar and the British

pound –corresponding to the three main sources of

the Group’s exposure to currency risks– would have

the effect of increasing or reducing the value of the

hedges on these currencies by approximately €2.7

million