APC 2012 Annual Report Download - page 201

Download and view the complete annual report

Please find page 201 of the 2012 APC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

|

|

2012 REGISTRATION DOCUMENT SCHNEIDER ELECTRIC 199

CONSOLIDATED FINANCIAL STATEMENTS AT DECEMBER31, 2012

5

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Valuation of stock grants

In accordance with the accounting policies described in note1.20,

the stock grant plans have been valued on the basis of an average

estimated life of between four and fi ve years using the following

assumptions:

•a payout rate of between 3.0% and 4.5%;

•a discount rate of between 1.6% and 4.5%, corresponding to a

risk-free rate over the life of the plans (source: Bloomberg).

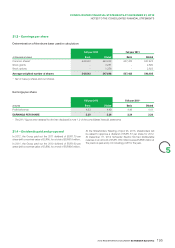

Based on these assumptions, the amount recorded under “Selling, general and administrative expenses” for stock grant plans set up after

November7, 2002 breaks down as follows:

Full year 2012 Full year 2011

Plan 5 -2

Plan 6 12

Plan 7 --

Plan 8 -5

Plan 9 56

Plan 10 14 16

Plan 11 12 13

Plan 10 bis --

Plan 11 bis --

Plan 12 --

Plan 13 11 -

Plan 14 10 -

TOTAL 53 44

21.5.2 Worldwide Employee Stock Purchase Plan

Schneider Electric gives its employees the opportunity to become

group shareholders thanks to employee share issues. Employees

in countries that meet legal and fi scal requirements have the choice

between a classic and a leveraged plan.

Under the classic plan, employees may purchase Schneider

Electric shares at a 15% to20% discount to the price quoted for

the shares on the stock market. Employees must then hold their

shares for fi ve years, except in certain cases provided for by law.

The share-based payment expense recorded in accordance with

IFRS2 is measured by reference to the fair value of the discount on

the locked-up shares. The lock-up cost is determined on the basis

of a two-step strategy that involves fi rst selling the locked-up shares

on the forward market and then purchasing the same number of

shares on the spot market (i.e., shares that may be sold at any time)

using a bullet loan.

This strategy is designed to refl ect the cost that, the employee

would incur during the lock-up period to avoid the risk of carrying

the shares subscribed under the classic plan. The borrowing cost

corresponds to the cost of borrowing for the employees concerned,

as they are the sole potential buyers in this market. It is based on

the average interest rate charged by banks for an ordinary, non-

revolving personal loan with a maximum maturity of fi ve years

granted to an individual with an average credit rating.

Under the leveraged plan, employees may also purchase Schneider

Electric shares at a 15% to20% discount from the price quoted on

the stock market. However, the leveraged plan offers a different yield

profi le as a third-party bank tops up the employee’s initial investment,

essentially multiplying the amount paid by the employee. The total

is invested in Schneider Electric shares at a preferential price. The

bank converts the discount transferred by the employee into funds

with a view to securing the yield for the employee and increasing the

indexation on a leveraged number (factor of 4.4 in2012) of directly

subscribed shares.

As with the classic plan, the share-based payment expense is

determined by reference to the fair value of the discount on the

locked-up shares (see above). In addition, it includes the value of the

benefi t corresponding to the issuer’s involvement in the plan, which

means that employees have access to share prices with a volatility

profi le adapted to institutional investors rather than to the prices and

volatility profi le they would have been offered if they had purchased

the shares through their retail banks. The volatility differential is

treated as a discount equivalent that refl ects the opportunity gain

offered to employees under the leveraged plan.

As regards the fi rst semester 2012, Schneider Electric offers to

its employees the opportunity to purchase shares at a price of

EUR36.66 or EUR34.50 per share, depending on the country, as

part of its commitment to employee share ownership, on June14,

2012. This represented a 15% to20% discount to the reference

price of EUR43.12 calculated as the average opening price quoted

for the share during the 20 days preceding the Management

Board’s decision to launch the employee share issue.

Altogether, 3.5 million shares were subscribed, increasing the

Company’s capital by EUR124 million as of July 19, 2012. Due

to signifi cant changes in valuation assumptions, specifi cally the

interest rate available to market participant, the value of the lock-up

period is higher than the discount cost. Therefore the Group did not

recognize any cost related to the transaction.