Cabela's 2011 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2011 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

51

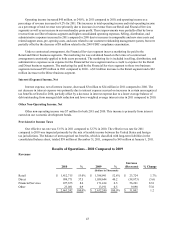

tax benefits, which is classified with long-term liabilities in the consolidated balance sheet, totaled $43 million at

January 1, 2011, compared to $3 million at January 2, 2010. The increase was due primarily to our current year

assessment of uncertain tax positions reflected on prior year tax returns.

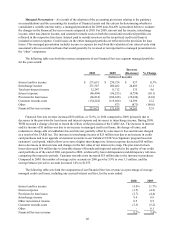

Bank Asset Quality

Delinquencies and Non-Accrual

We consider the entire balance of an account, including any accrued interest and fees, delinquent if the

minimum payment is not received by the payment due date. Our aging method is based on the number of

completed billing cycles during which a customer has failed to make a required payment. As part of collection

efforts, a credit card loan may be closed and placed on non-accrual or restructured in a fixed payment plan prior to

charge off. Our fixed payment plans consist of a lower interest rate, reduced minimum payment, and elimination of

fees. Loans on fixed payment plans include loans in which the customer has engaged a consumer credit counseling

agency to assist them in managing their debt. Non-accrual loans with two consecutive missed payments will

resume accruing interest at the rate they had accrued at before they were placed on non-accrual. Payments received

on non-accrual loans will be applied to principal and reduce the amount of the loan.

The following table shows delinquent, non-accrual, and restructured loans as a percentage of our credit card

loans, including any accrued interest and fees, at the years ended:

2011 2010 2009

Number of days delinquent and still accruing:

Greater than 30 days 0.64% 0.74% 1.07%

Greater than 60 days 0.38 0.47 0.66

Greater than 90 days 0.20 0.25 0.36

Non-accrual 0.20 0.24 0.18

Restructured (excluded from percentages above) 1.91 2.90 3.52

The following table reports delinquencies, including any delinquent non-accrual and restructured credit card

loans, as a percentage of our credit card loans, including any accrued interest and fees, in a manner consistent with

our monthly external reporting for the years ended:

2011 2010 2009

Number of days delinquent:

Greater than 30 days 0.87% 1.13% 1.79%

Greater than 60 days 0.53 0.72 1.09

Greater than 90 days 0.27 0.37 0.56

Delinquencies declined as a result of improvements in the economic environment and our conservative

underwriting criteria and active account management.

Allowance for Loan Losses and Charge-offs

The allowance for loan losses represents management’s estimate of probable losses inherent in the credit

card loan portfolio. The allowance for loan losses is established through a charge to the provision for loan losses

and is regularly evaluated by management for adequacy. Loans on a payment plan or non-accrual are segmented

from the rest of the credit card loan portfolio into a restructured credit card loan segment before establishing an

allowance for loan losses as these loans have a higher probability of loss. Management estimates losses inherent in

the credit card loans segment and restructured credit card loans segment based on a model which tracks historical

loss experience on delinquent accounts, bankruptcies, death, and charge-offs, net of estimated recoveries. WFB