Cabela's 2011 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2011 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

80

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in Thousands Except Share and Per Share Amounts)

WFB retained certain interests in securitized loans, including a transferor’s interest, servicing rights, interest-

only strips, cash reserve accounts, and in some cases cash accounts. WFB classified the interest-only strips and

cash reserve accounts as retained interests in securitized loans. A servicing asset or liability was not recognized as

WFB received adequate compensation relative to current market servicing rates.

In addition, WFB owned asset-backed securities from its securitizations, which in some cases were

subordinated to other notes issued as retained interests in securitized loans. The asset-backed securities were

classified as trading securities or available-for-sale securities. Asset-backed trading securities fluctuated daily

based on the short-term operational needs of WFB. Advances and pay downs on the trading securities were at

par value. Therefore, the par value of the asset-backed trading securities approximated fair value. Asset-backed

available-for-sale securities were carried at fair value with changes reflected in accumulated other comprehensive

income. For asset-backed available-for-sale securities, WFB estimated fair value using discounted cash flow

projection estimates based upon management’s evaluation of contractual principal and interest cash flows.

WFB retained rights to future cash flows from (i) finance charge collections, certain fee collections,

allocated interchange, and recoveries on charged-off accounts net of collection costs arising after investors had

received the return for which they were entitled; (ii) reimbursement for charged-off accounts; and (iii) after certain

administrative costs, such as servicing fees. This portion of the retained interests was known as interest-only strips

and was subordinate to investor’s interests. For interest-only strips and cash reserve accounts, WFB estimated

related fair values based on the present value of future expected cash flows using assumptions for credit losses,

finance charge yields, payment rates, and discount rates commensurate with the risks involved but did not include

interchange income since interchange income was earned only when a charge was made to a customer’s account.

The value of the interest-only strips and cash reserve accounts were subject to credit, payment rate, and interest

rate risks on the loans sold. For cash accounts, WFB estimated related fair values based on the present value of

future expected cash flows using discount rates commensurate with the risks involved. Fair value changes in

the interest-only strips and cash reserve accounts were recorded in securitization income included in Financial

Services revenue.

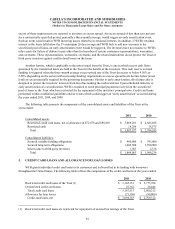

4. CABELA’S MASTER CREDIT CARD TRUST

WFB utilizes the Trust for the purpose of routinely selling and securitizing credit card loans and issuing

beneficial interest to investors. The Trust issues variable funding facilities and long-term notes each of which has

an undivided interest in the assets of the Trust. WFB must retain a minimum 20 day average of 5% of the loans in

the securitization trust which ranks pari passu with the investors’ interests in the securitized trusts. In addition,

WFB owns notes issued by the Trust from some of the securitizations, which in some cases may be subordinated

to other notes issued. The consolidated assets of the Trust are subject to credit, payment, and interest rate risks on

the transferred credit card loans. The secured borrowings still contain the legal isolation requirements which would

protect the assets pledged as collateral for the securitization investors as well as protecting Cabela’s and WFB from

any liability from default on the notes.

To protect investors, the securitization structures include certain features that could result in earlier-than-

expected repayment of the securities, which could cause WFB to sustain a loss of one or more of its retained

interests and could prompt the need for WFB to seek alternative sources of funding. The primary investor

protection feature relates to the availability and adequacy of cash flows in the securitized pool of loans to meet

contractual requirements, the insufficiency of which triggers early repayment of the securities. WFB refers to

this as the “early amortization” feature. Investors are allocated cash flows derived from activities related to the

accounts comprising the securitized pool of loans, the amounts of which reflect finance charges collected, certain

fee assessments collected, allocations of interchange, and recoveries on charged-off accounts. These cash flows are

considered to be restricted under the governing documents to pay interest to investors, servicing fees, and to absorb

the investor’s share of charge-offs occurring within the securitized pool of loans. Any cash flows remaining in