Cabela's 2014 Annual Report Download

Download and view the complete annual report

Please find the complete 2014 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

LETTER TO SHAREHOLDERS

FORM 10–K

REPORT

2014

Table of contents

-

Page 1

L E T T E R T O S H A R E H O L D E R S 1 0 - K 2014 REPORT F O R M -

Page 2

... Outï¬tter. direct business, we offer a wide and distinctive selection of high-quality outdoor products at competitive prices while providing superior customer service. We also issue the Cabela's CLUB® Visa credit card, which serves as our primary customer loyalty rewards program. Total Revenue... -

Page 3

...ï¬t-per-square-foot basis. In 2014, we opened 14 new stores to thousands of customers waiting in line at each one. These new stores represented roughly one million square feet of retail growth for the year. Our new locations included Augusta, Georgia; Greenville, South Carolina; Anchorage, Alaska... -

Page 4

...of our retail locations. With the ability to fulï¬ll direct-channel orders from our retail stores, we can give our customers access to our inventory assortment across the Company, rather than generating a negative online experience when we do not have a speciï¬c product in our distribution centers... -

Page 5

... balance per active credit card account grew 4.5%, and net charge-offs reached historically low levels, ï¬nishing the year at 1.69%. In 2014, our customers earned roughly $214 million in free merchandise through our CLUB rewards program. Our CLUB members are our very best customers. They shop... -

Page 6

(This page intentionally left blank.) -

Page 7

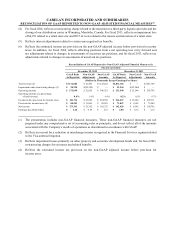

... of GAAP Reported to Non-GAAP Adjusted Financial Measures (1) Fiscal Year Ended December 27, 2014 December 28, 2013 GAAP Basis Non-GAAP Non-GAAP GAAP Basis Non-GAAP Non-GAAP As Reported Adjustments Amounts As Reported Adjustments Amounts (Dollars in Thousands Except Earnings Per Share) $ 3,647,650... -

Page 8

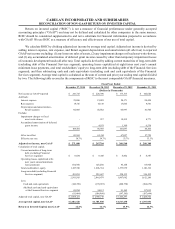

...our distribution center in Winnipeg, Manitoba, Canada. For fiscal 2013, reflects an impairment loss of $4,931 related to a retail store site and $937 of costs related to the closure and relocation of a retail store. Reflects interest adjustments related to certain unrecognized tax benefits. Reflects... -

Page 9

... impairment losses of economic development bonds (all after tax). Total capital is derived by adding current maturities of long-term debt (excluding debt of the Financial Services segment), operating leases capitalized at eight times next year's annual minimum lease payments, and total stockholders... -

Page 10

(This page intentionally left blank.) -

Page 11

...,847 as of June 27, 2014 (the last business day of the registrant's most recently completed second fiscal quarter), based upon the closing price of the registrant's Class A Common Stock on that date as reported on the New York Stock Exchange. Indicate the number of shares outstanding of each of the... -

Page 12

... and credit markets or the availability of capital and credit; our ability to successfully execute our omni-channel strategy; increasing competition in the outdoor sporting goods industry and for credit card products and reward programs; the cost of our products, including increases in fuel prices... -

Page 13

... About Market Risk Financial Statements and Supplementary Data Changes in and Disagreements With Accountants on Accounting and Financial Disclosure Controls and Procedures Other Information PART III Item 10. Item 11. Item 12. Item 13. Item 14. Directors, Executive Officers and Corporate Governance... -

Page 14

... products at competitive prices, while providing superior customer service. We also issue the Cabela's CLUB® Visa credit card, which serves as our primary customer loyalty rewards program. Refer to Note 23 "Segment Reporting" of the Notes to Consolidated Financial Statements and our "Management... -

Page 15

... state and local governments. Refer to Item 2 - "Properties" for additional information on our stores. Direct Business The Direct segment sells products through our e-commerce websites (Cabelas.com and Cabelas.ca) and direct mail catalogs. Our Direct segment generated revenue of $852 million in 2014... -

Page 16

...through a number of channels, including retail stores, our website, inbound telemarketing, and our catalogs. Our customers can apply for the Cabela's CLUB Visa credit card at our retail stores and website through our instant credit process and, if approved, receive reward points available for use on... -

Page 17

...our own Cabela's brand. Our product assortment includes merchandise and equipment for hunting, fishing, marine use, and camping, along with casual and outdoor apparel and footwear, optics, wildlife and land management products and services, vehicle accessories, and gifts and home furnishings with an... -

Page 18

... on our merchandise through enhanced customer targeting, expanded use of digital marketing channels in mobile marketing and social networking and other technology-based approaches, the development and marketing of new products, and continued focus on specialty catalogs. Our Cabela's brand platform... -

Page 19

..., product information, and service operations. Distribution and Fulfillment We operate distribution centers located in Sidney, Nebraska; Prairie du Chien, Wisconsin; Wheeling, West Virginia; and Winnipeg, Manitoba, Canada. These distribution centers comprise approximately 3.3 million square feet of... -

Page 20

...to states in which our retail stores are physically located. As we open more retail stores, we will be subject to tax in an increasing number of state and local taxing jurisdictions. Intellectual Property Cabela's®, Cabela's CLUB®, Cabelas.com®, World's Foremost Outfitter®, World's Foremost Bank... -

Page 21

...Goods, and Big 5 Sporting Goods; retailers that currently compete with us through retail businesses that may enter the direct business; mass merchandisers, warehouse clubs, discount stores, and department stores, such as Wal-Mart, Target, and Amazon; and casual outdoor apparel and footwear retailers... -

Page 22

... new stores in locations with high concentrations of our Direct business customers. As a result of this competition, we may need to spend more on advertising and promotion. Some of our mass merchandising competitors, such as Wal-Mart, do not currently compete in many of the product lines we offer... -

Page 23

... on our information technology systems to manage and replenish inventory, to take customer orders, to deliver products to our customers in an efficient manner, to collect payments from our customers, and to provide accurate financial data and reporting for our business. Although we continually... -

Page 24

... adjust the fixed costs of a catalog mailing to reflect subsequent sales of the products marketed in the catalog; and increases in United States Postal Service rates, paper costs, and printing costs resulting in higher catalog production costs and lower profits for our Direct business. Any one or... -

Page 25

...website posting; shipping companies, such as United Parcel Service, the United States Postal Service, and common carriers, for timely delivery of our catalogs, shipment of merchandise to our customers, and delivery of merchandise from our vendors to us and from our distribution centers to our retail... -

Page 26

... United States or foreign labor strikes, work stoppages, or boycotts, could increase the cost or reduce the supply of merchandise available to us or may require us to modify our current business practices, any of which could hurt our profitability. Due to the seasonality of our business, our annual... -

Page 27

... centers in Sidney, Nebraska; Prairie du Chien, Wisconsin; Wheeling, West Virginia; and Winnipeg, Manitoba, Canada, to handle our distribution needs. We also currently lease a distribution center in Tooele, Utah. We are building a 600,000 square foot distribution center in Tooele, Utah, to support... -

Page 28

... expanded distribution centers into our inventory control process, we may not be able to deliver inventory to our retail stores in a timely manner, which could have a material adverse effect on the revenue and cash flows of our Retail business. We may incur costs from litigation relating to products... -

Page 29

... our Financial Services segment, which could limit growth of the business and decrease our profitability. Our Financial Services segment requires a significant amount of cash to operate. These cash requirements will increase if our credit card originations increase or if our cardholders' balances or... -

Page 30

... our Retail and Direct businesses to meet the capital needs of our Financial Services segment, which could alter our retail store expansion program. WFB must satisfy the capital maintenance requirements of government regulators and its agreement with Visa U.S.A., Inc. ("Visa"). At the end of 2014... -

Page 31

...with increased use of advertising, target marketing, reward programs, mobile payment solutions, and pricing competition in interest rates and cardholder fees as both traditional and new credit card issuers seek to expand or to enter the market and compete for customers. Economic downturns and social... -

Page 32

... of credit, savings, and payment services and products, and WFB is subject to its regulation. While the Bureau does not currently examine WFB, it receives information from the FDIC, WFB's primary regulator. The Bureau also has rulemaking and interpretive authority under existing and future consumer... -

Page 33

...between the interest rate we pay on our borrowings and the fees we earn from these accounts may change and our profitability may be materially adversely affected. Credit card industry litigation and regulation could adversely impact the amount of revenue our Financial Services segment generates from... -

Page 34

...Center Retail Store Concept Center (1) Customer Care Center, Bank Operations, and Administrative Offices (3) Data Information Center Marketing and Information Technology Center (1) Administrative Offices Data Information Center (1) Location Wheeling, West Virginia Prairie du Chien, Wisconsin Sidney... -

Page 35

...Connecticut; Christiana, Delaware; Bowling Green, Kentucky; Louisville, Kentucky; Kalispell, Montana; Missoula, Montana; Cheektowaga, New York; Tualatin, Oregon; Greenville, South Carolina; Lubbock, Texas; Union Gap, Washington; Charleston, West Virginia; and Green Bay, Wisconsin. In Canada, we have... -

Page 36

... name" accounts through brokers or banks. The following table sets forth, for the fiscal quarters indicated, the high and low sales prices per share of our common stock as reported on the New York Stock Exchange: 2014 High First Quarter Second Quarter Third Quarter Fourth Quarter Low High 2013 Low... -

Page 37

...graph and table show Cabela's cumulative total shareholder return on a semi-annual basis as of the last respective trading date for the five fiscal years ended December 27, 2014. The graph and table also show the cumulative total returns of the Standard and Poor's ("S&P") 500 Retailing Index and the... -

Page 38

... ended 2014, 2013, 2012, 2011, and 2010, respectively. Regulatory restrictions limit our ability to use this cash for non-banking operations, including its use as working capital for our Retail or Direct businesses, or for retail store expansion. Includes restricted credit card loans of the Cabela... -

Page 39

... retail square footage of 6.9 million, an increase of 17% over 2013. Our Direct business segment is comprised of our highly acclaimed website and supplemented by our catalog distributions as a selling and marketing tool. World's Foremost Bank ("WFB," "Financial Services segment," or "Cabela's CLUB... -

Page 40

... hunting equipment product category, decreased significantly comparing 2014 to 2013. We believe the decreases in firearms and ammunition sales have begun to level out, and we expect firearms and ammunition sales in 2015 to return to more normalized, pre-surge 2013, levels. In 2013, demand increased... -

Page 41

... in generating cash flows, thereby creating value in our Company. We offer our customers integrated opportunities to access and use our retail store, e-commerce websites (Cabelas.com and Cabelas.ca), and catalog channels. Our in-store pick-up program allows customers to order products through... -

Page 42

... with plans to increase retail square footage approximately one million square feet annually over the next several years. Our total retail store square footage at the end of 2014 was 6.9 million square feet, an increase of 17% compared to the end of 2013. For 2015, we have announced plans to open 13... -

Page 43

... active account management. Comparing Cabela's CLUB results for 2014 to 2013: Financial Services revenue increased $55 million, or 14.5%; the average number of active accounts increased 7.6% to 1.8 million, and the average balance per active account increased 4.5%; the average balance of our credit... -

Page 44

... of credit, savings, and payment services and products, and WFB is subject to its regulation. While the Bureau does not currently examine WFB, it receives information from the FDIC, WFB's primary regulator. The Bureau also has rulemaking and interpretive authority under existing and future consumer... -

Page 45

... on the securitization market and the Financial Services segment is also unclear at this time. Visa Litigation Settlement - In June 2005, a number of entities, each purporting to represent a class of retail merchants, sued Visa and several member banks, and other credit card associations, alleging... -

Page 46

... our hunting and fishing outfitter services, fees for our full-service travel agency business, real estate rental income and land sales, and other complementary business services. We have added our retail stores to our distribution network, so customers who order through our call centers or website... -

Page 47

...a wide variety of firearms, ammunition, optics, archery products, and related accessories and supplies. The general outdoors merchandise category includes a full range of equipment and accessories supporting all outdoor activities, including all types of fishing and tackle products, boats and marine... -

Page 48

... our new retail store growth. Our hunting equipment and general outdoors categories were the largest dollar volume contributors to our Direct revenue for 2014. The number of active Direct customers, which we define as those customers who have purchased merchandise from us in the last twelve months... -

Page 49

...'s CLUB Visa credit card loyalty program allows customers to earn points whenever and wherever they use their credit card, and then redeem earned points for products and services at our retail stores or through our Direct business. The percentage of our merchandise sold to customers using the Cabela... -

Page 50

... related to our retail stores, website, distribution centers, product procurement, Cabela's CLUB credit card operations, and overhead costs, including: advertising and marketing, catalog costs, employee compensation and benefits, occupancy costs, information systems processing, and depreciation and... -

Page 51

... administrative expenses are presented below for the years ended: Increase (Decrease) 2014 Selling, distribution, and administrative ("SD&A") expenses $ SD&A expenses as a percentage of total revenue Retail store pre-opening costs $ 2013 % Change (Dollars in Thousands) 1,251,325 $ 34.3% 24,338... -

Page 52

... and (ii) at least annually for recurring fair value measurements and for those assets not subject to amortization. In 2014 and 2013, we evaluated the recoverability of economic development bonds, property (including existing store locations and future retail store sites), equipment, goodwill, other... -

Page 53

... corporate overhead costs. Comparisons and analysis of operating income are presented below for the years ended: Increase (Decrease) 2014 Total operating income Total operating income as a percentage of total revenue Operating income by business segment: Retail Direct Financial Services Operating... -

Page 54

... CLUB Visa credit card portfolio. In addition, among other items, the agreement requires the Financial Services segment to reimburse the Retail and Direct segments for certain promotional costs, which are recorded as a reduction to Financial Services segment revenue and as a reduction to merchandise... -

Page 55

... led by an increase in the hunting equipment product category primarily from increases in firearms and ammunition, hunting apparel, archery, and optics, as well as men's apparel and general outdoors. Ammunition sales, while still above prior year levels, slowed during the third quarter of 2013 and... -

Page 56

... efforts on utilizing Direct marketing programs to increase traffic to our website and social media networks. Our hunting equipment and clothing and footwear categories were the largest dollar volume contributor to our Direct revenue for 2013. The number of active Direct customers, which we define... -

Page 57

... of our merchandise sold to customers using the Cabela's CLUB Visa credit card approximated 30% for 2013. The dollar amounts related to points are accrued as earned by the cardholder and recorded as a reduction in Financial Services revenue. The dollar amount of unredeemed credit card points and... -

Page 58

... million in employee compensation, benefits, and contract labor primarily due to the opening of new retail stores and increases in staff for other retail stores, merchandising support areas, distribution centers, credit card growth support, and general corporate overhead support; an increase of $23... -

Page 59

... of $13 million in advertising, promotional, and direct marketing costs to support customer relationships, for new store openings, and from an increase in account origination costs in our Financial Services segment; an increase of $10 million in professional fees; and an increase of $6 million in... -

Page 60

... in the third quarter of 2011. The developer's purchase offer expired in 2012, and the Company continued to market the property for sale and sought an appraisal. In January 2013, we received an appraisal report on the Colorado Property. This appraisal report concluded that the carrying value of the... -

Page 61

...to increases in comparable and new store costs and related support areas. Under an Intercompany Agreement, the Financial Services segment pays to the Retail and Direct business segments a fixed license fee equal to 70 basis points on all originated charge volume of the Cabela's CLUB Visa credit card... -

Page 62

... use the scores of Fair Isaac Corporation ("FICO"), a widely-used financial metric for assessing an individual's credit rating, as the primary credit quality indicator. The median FICO score of our credit cardholders was 795 at the end of 2014 and 793 at the end of 2013. The following table reports... -

Page 63

... end of 2013 primarily as a result of our conservative underwriting criteria and active account management. The table below shows delinquent, non-accrual, and restructured loans as a percentage of our credit card loans, including any accrued interest and fees, at the years ended: 2014 Number of days... -

Page 64

... increase in recovery rates, and declining loan balances in our restructured loan portfolio. Aging of Credit Cards Loans Outstanding The following table shows our credit card loans outstanding at the end of 2014 and 2013 segregated by the number of months passed since the accounts were opened. 2014... -

Page 65

... tax costs in the future if our expectations or the amount of cash held by our foreign subsidiaries change. Retail and Direct Segments - The primary cash requirements of our merchandising business relate to capital for new retail stores, purchases of inventory, investments in our management... -

Page 66

... by Nebraska banking law and the Visa U.S.A., Inc. membership rules, and its ability to pay dividends is also limited by Nebraska and Federal banking law. If there are any disruptions in the credit markets, the Financial Services segment, like many other financial institutions, may increase its... -

Page 67

... our business and cause the Financial Services segment to lose an important source of capital. The Reform Act, which was signed into law in July 2010, will also affect a number of significant changes relating to asset-backed securities, including additional oversight and regulation of credit rating... -

Page 68

... years ended: 2014 Cash paid for property and equipment additions Proceeds from retirements and maturities of economic development bonds Number of new retail stores opened during the year, including the Winnipeg relocation in 2013 Number of retail stores at the end of the year Retail square footage... -

Page 69

... the borrowing activities of our merchandising business and the Financial Services segment for the years ended: 2014 Borrowings on revolving credit facilities and inventory financing, net of repayments Secured obligations of the Trust, net Repayments of long-term debt Borrowings, net of repayments... -

Page 70

... to economic development bonds in 2014 or 2013. However, at December 27, 2014, we identified economic development bonds totaling $39 million where the actual tax revenues associated with these properties were lower than previously projected. We will continue to closely monitor the amounts and timing... -

Page 71

... to be received from our economic development bonds. Please refer to Note 1 "Nature of Business and Summary of Significant Accounting Policies" of the Notes to Consolidated Financial Statements under the section entitled "Economic Development Bonds" for information on our procedures used to analyze... -

Page 72

... costs and potentially limit our ability to grow the business of the Financial Services segment. Unfavorable conditions in the asset-backed securities markets generally, including the unavailability of commercial bank liquidity support or credit enhancements, could have a similar effect. In 2015... -

Page 73

... 27, 2014, the Financial Services segment had $806 million of certificates of deposit outstanding with maturities ranging from January 2015 to July 2023 and with a weighted average effective annual fixed rate of 2.25%. This outstanding balance compares to $1.1 billion at December 28, 2013, with... -

Page 74

... related to the development, construction, and completion of new retail stores, a new distribution center, and expansion of our corporate offices. The table does not include any amounts for contractual obligations associated with retail store locations where we are in the process of certain... -

Page 75

... Revenue Recognition Revenue is recognized on our Direct sales when merchandise is delivered to the customer at the point of delivery, with the point of delivery based on our estimate of shipping time from our distribution centers to the customer. We recognize reserves for estimated product returns... -

Page 76

...or property tax revenues generated from our retail store locations or additional developments in the local development or tax increment financing district. Each quarter we revalue each economic development bond using discounted cash flow models based on available market interest rates and management... -

Page 77

... development bonds in 2014. However, at December 27, 2014, we identified economic development bonds with carrying values of $39 million where the actual tax revenues associated with these properties were lower than previously projected. We will continue to closely monitor the amounts and timing... -

Page 78

... on the credit cards issued by the Financial Services segment were priced at a margin over various defined lending rates. No interest is charged if the account is paid in full within 25 days of the billing cycle, which represented 29.5% of total balances outstanding at the end of 2014. Some of... -

Page 79

... 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA TABLE OF CONTENTS Page REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM CONSOLIDATED FINANCIAL STATEMENTS: Consolidated Statements of Income Consolidated Statements of Comprehensive Income Consolidated Balance Sheets Consolidated Statements of... -

Page 80

... PUBLIC ACCOUNTING FIRM To the Board of Directors and Stockholders of Cabela's Incorporated and Subsidiaries Sidney, Nebraska We have audited the accompanying consolidated balance sheets of Cabela's Incorporated and Subsidiaries (the "Company") as of December 27, 2014 and December 28, 2013, and... -

Page 81

CABELA'S INCORPORATED AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF INCOME (Dollars in Thousands Except Earnings Per Share) 2014 Revenue: Merchandise sales Financial Services revenue Other revenue Total revenue Cost of revenue: Merchandise costs (exclusive of depreciation and amortization) Cost of ... -

Page 82

... adjustments (14,821) Unrealized gain (loss) on economic development bonds, net of taxes of $2,938, $(923), and $2,035 4,839 Cash flow hedges, net of taxes of $70 in 2012 Total other comprehensive income (loss) (9,982) Comprehensive income $ 191,733 Fiscal Years 2013 $ 224,390 (5,126) (2,141... -

Page 83

... taxes receivable and deferred income taxes Total current assets Property and equipment, net Economic development bonds Other assets Total assets LIABILITIES AND STOCKHOLDERS' EQUITY CURRENT Accounts payable, including unpresented checks of $38,790 and $22,717 Gift instruments, credit card rewards... -

Page 84

... current assets Accounts payable and accrued expenses and other liabilities Gift certificates, credit card rewards, and loyalty rewards programs Other long-term liabilities Income taxes receivable Net cash provided by operating activities CASH FLOWS FROM INVESTING ACTIVITIES: Property and equipment... -

Page 85

... on employee stock option exercises BALANCE, end of 2013 70,630,866 Net income Other comprehensive loss Stock-based compensation Exercise of employee stock options and tax withholdings on share-based payment awards 462,350 Excess tax benefit on employee stock option exercises BALANCE, end of 2014 71... -

Page 86

... of hunting, fishing, and outdoor gear, offering products through its retail stores, U. S. and Canada websites, and regular and specialty catalog mailings. Cabela's operates 64 retail stores, 57 located in 31 states and seven located in Canada. World's Foremost Bank ("WFB," "Financial Services... -

Page 87

... within one to four business days. Receivables from other banks totaled $22,345 and $14,209 at the end of 2014 and 2013, respectively. Unpresented checks, net of available cash bank balances, are classified as current liabilities. Cash and cash equivalents of the Financial Services segment were $49... -

Page 88

... totaled $3,564, $2,623, and $3,049 for 2014, 2013, and 2012, respectively. Store Pre-opening Expenses - Non-capital costs associated with the opening of new stores are expensed as incurred. Leases - The Company leases certain retail locations, distribution centers, office space, equipment, and land... -

Page 89

...revenue. Other property with a carrying value of $17,900 and $15,109 at the end of 2014 and 2013, respectively, was included in other assets in the consolidated balance sheets. Government Economic Assistance - When Cabela's constructs a new retail store or retail development, the Company may receive... -

Page 90

... be received from its economic development bonds. We revalue each economic development bond using discounted cash flow models based on available market interest rates (Level 2 inputs) and management estimates, including the estimated amounts and timing of expected future tax payments (Level 3 inputs... -

Page 91

..., and the Cabela's CLUB points issued never expire. The total cost incurred for all credit card rewards and loyalty programs was $210,190, $198,687, and $176,882 for 2014, 2013, and 2012, respectively. Income Taxes - The Company files consolidated federal and state income tax returns with its wholly... -

Page 92

...at the end of a reporting period. Gains and losses from translation into United States dollars are included in accumulated other comprehensive income (loss) in our consolidated balance sheets. Revenues and expenses are translated at average monthly currency exchange rates. Earnings Per Share - Basic... -

Page 93

CABELA'S INCORPORATED AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Dollars in Thousands Except Share and Per Share Amounts) 4. CREDIT CARD LOANS AND ALLOWANCE FOR LOAN LOSSES The following table reflects the composition of the credit card loans at the years ended: 2014 2013 $ 3,956... -

Page 94

...CONSOLIDATED FINANCIAL STATEMENTS (Dollars in Thousands Except Share and Per Share Amounts) The tables below provide information on current, non-accrual, past due, and restructured credit card loans by class using the respective fourth quarter FICO score at the years ended: Restructured Credit Card... -

Page 95

... Losses $ $ - Amortized Cost December 27, 2014 December 28, 2013 $ $ 66,865 71,072 Fair Value $ $ 82,074 78,504 Estimated maturities based on expected future cash flows for the economic development bonds at the end of 2014 were as follows: Amortized Cost For the fiscal years ending: 2015... -

Page 96

... of the following at the years ended: 2014 Prepaid expenses and other current assets: Financial Services segment - accrued interest and other receivables Other Other assets: Other property Long-term notes and other receivables Financial Services segment - deferred financing costs Goodwill and other... -

Page 97

... net of fees, totaling $802,076 and $1,062,312 at the end of 2014 and 2013, respectively. 11. BORROWINGS OF FINANCIAL SERVICES SEGMENT The Trust issues fixed and floating (variable) rate term securitizations, which are considered secured obligations backed by restricted credit card loans. A summary... -

Page 98

...unused portion of the facilities. During the years ended 2014 and 2013, the daily average balance outstanding on these notes was $29,603 and $26,328, with a weighted average interest rate of 0.76% and 0.77%, respectively. The Financial Services segment has unsecured federal funds purchase agreements... -

Page 99

... balance outstanding on the line of credit was $255,499 and $130,729, respectively, and the weighted average interest rate was 1.42% and 1.44%, respectively. Letters of credit and standby letters of credit totaling $20,064 and $17,378, respectively, were outstanding at the end of 2014 and 2013... -

Page 100

...June 2036. The monthly installments are $83 and the lease contains a bargain purchase option at the end of the lease term. We accounted for this lease as a capital lease and recorded the additional leased asset at the present value of the future minimum lease payments using a 5.9% implicit rate. The... -

Page 101

... 2014, 2013, and 2012, we evaluated the recoverability of our economic development bonds, property (including existing store locations and future retail store sites), equipment, goodwill, other property, and other intangible assets. Canada Distribution Center: On June 11, 2014, the Company announced... -

Page 102

... 29, 2014. In 2013, we also recognized an impairment loss totaling $937 related to the store closure of our former Winnipeg, Manitoba, Canada, retail site. This impairment loss included leasehold improvements write-offs as well as lease cancellation and restoration costs. This impairment loss was... -

Page 103

... in the third quarter of 2011. The developer's purchase offer expired in 2012, and the Company continued to market the property for sale and sought an appraisal. In January 2013, we received an appraisal report on the Colorado Property. This appraisal report concluded that the carrying value of the... -

Page 104

... reporting purposes, income before taxes includes the following components: 2014 Federal Foreign $ 276,041 42,436 $ 318,477 $ $ 2013 244,878 98,650 343,528 2012 $ 164,433 97,281 $ 261,714 The provision for income taxes consisted of the following for the years ended: 2014 Current: Federal State... -

Page 105

... tax liabilities: Prepaid expenses Property and equipment Inventories Credit card loan fee deferral U.S. income tax on foreign earnings Economic development bonds Other Total deferred tax liabilities Net deferred tax (asset) liability Less current deferred income taxes Long-term deferred income tax... -

Page 106

... $9,122 at the end of 2013 that was included in other long-term liabilities. The total amount of unrecognized tax benefits that, if recognized, would affect the effective tax rate was $11,016. The Company's tax years 2007 through 2011 are under examination by the Internal Revenue Service ("IRS"). In... -

Page 107

... various new retail store site locations. At December 27, 2014, the Company estimated it had total cash commitments of approximately $523,500 outstanding for projected expenditures related to the development, construction, and completion of new retail stores, a new distribution center, and corporate... -

Page 108

... and Per Share Amounts) Under various grant programs, state or local governments provide funding for certain costs associated with developing and opening a new retail store. The Company generally receives grant funding in exchange for commitments, such as assurance of agreed employment and wage... -

Page 109

... FINANCIAL STATEMENTS (Dollars in Thousands Except Share and Per Share Amounts) Litigation and Claims - The Company is party to various legal proceedings arising in the ordinary course of business. These actions include commercial, intellectual property, employment, regulatory, and product... -

Page 110

...AND EMPLOYEE BENEFIT PLANS Stock-Based Compensation - The Company recognized total stock-based compensation expense of $17,498, $14,969, and $13,733 in 2014, 2013, and 2012, respectively. Compensation expense related to the Company's stock-based payment awards is recognized in selling, distribution... -

Page 111

... and one year for non-employee directors. In addition, the Company issued 64,000 premium-priced NSOs to its President and Chief Executive Officer under the 2013 Plan at an exercise price of $76.27 (which was equal to 115% of the closing price of the Company's common stock on the New York Stock... -

Page 112

CABELA'S INCORPORATED AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Dollars in Thousands Except Share and Per Share Amounts) The following table provides information relating to the Company's equity share-based payment awards at December 27, 2014: Weighted Average Remaining ... -

Page 113

... other comprehensive loss, net of related taxes, are as follows for the years ended: 2014 2013 9,521 $ 4,682 (21,227) (6,406) $ (11,706) $ (1,724) Accumulated net unrealized holding gains on economic development bonds Cumulative foreign currency translation adjustments Total accumulated other... -

Page 114

CABELA'S INCORPORATED AND SUBSIDIARIES NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Dollars in Thousands Except Share and Per Share Amounts) The following table reconciles the Company's treasury stock activity for the years ended: 2014 Balance, beginning of year Purchase of treasury stock at a cost ... -

Page 115

... e-commerce websites (Cabelas.com and Cabelas.ca) and direct mail catalogs. The Financial Services segment issues co-branded credit cards. Revenues included in Corporate Overhead and Other are primarily made up of amounts received from outfitter services, real estate rental income, land sales, and... -

Page 116

... Share and Per Share Amounts) Financial information by segment is presented below for the following years: Corporate Overhead and Other $ 14,842 14,842 14,842 (306,627) N/A 38,623 879,844 126,016 Fiscal Year 2014: Merchandise sales $ Non-merchandise revenue: Financial Services Other Total revenue... -

Page 117

...for the years ended: 2014 Interest and fee income Interest expense Provision for loan losses Net interest income, net of provision for loan losses Non-interest income: Interchange income Other non-interest income Total non-interest income Less: Customer rewards costs Financial Services revenue $ 400... -

Page 118

... values of the Company's economic development bonds were estimated using discounted cash flow projection estimates. These estimates are based on available market interest rates and the estimated amounts and timing of expected future payments to be received from municipalities under tax development... -

Page 119

...using significant unobservable inputs. This evaluation included existing store locations and future retail store sites. Impairment losses consisted of the following for the years ended: 2014 Carrying value of other property and other assets Fair value of related assets Impairment losses $ $ $ $ 2013... -

Page 120

... fair value of the credit card loans does not represent the underlying value of the established cardholder relationship. Time Deposits. Time deposits are pooled in homogeneous groups, and the future cash flows of those groups are discounted using current market rates offered for similar products for... -

Page 121

... FINANCIAL STATEMENTS (Dollars in Thousands Except Share and Per Share Amounts) 25. QUARTERLY FINANCIAL INFORMATION (Unaudited) The following table sets forth unaudited financial and operating data in each quarter for years 2014 and 2013: 2014 by Quarter Second Third 2013 by Quarter Second... -

Page 122

... Costs and of Year Balance Expenses Year Ended December 27, 2014: Allowance for doubtful accounts on accounts receivable balances Reserve for sales returns (1) Reserve on notes receivable Allowance for credit card loan losses Year Ended December 28, 2013: Allowance for doubtful accounts on accounts... -

Page 123

... to allow timely decisions regarding required disclosure. In connection with this annual report on Form 10-K, our Chief Executive Officer and Chief Financial Officer evaluated, with the participation of our management, the effectiveness of our disclosure controls and procedures as of the end of the... -

Page 124

...with the standards of the Public Company Accounting Oversight Board (United States), the consolidated financial statements and financial statement schedule as of and for the year ended December 27, 2014, of the Company and our report dated February 17, 2015, expressed an unqualified opinion on those... -

Page 125

... and Ethics. These policies satisfy the SEC's requirements for a "code of ethics," and apply to all of our directors, officers, and employees. Our Business Code of Conduct and Ethics is posted on our website at www.cabelas.com. We intend to satisfy the disclosure requirements under Item 5.05 of Form... -

Page 126

... of this report: 1. Financial Statements: Report of Independent Registered Public Accounting Firm Consolidated Statements of Income - Years ended December 27, 2014, December 28, 2013, and December 29, 2012 Consolidated Statements of Comprehensive Income - Years ended December 27, 2014, December 28... -

Page 127

... by reference from Exhibit 10.13 of our Annual Report on Form 10-K, filed on February 20, 2013, File No. 001-32227)* Form of 2004 Stock Plan Employee Stock Option Agreement (incorporated by reference from Exhibit 10.13 of our Registration Statement on Form S-1, filed on March 23, 2004, Registration... -

Page 128

... and Restated Management Change of Control Severance Agreement (World's Foremost Bank) (incorporated by reference from Exhibit 10.3 of our Current Report on Form 8-K, filed on December 17, 2009, File No. 001-32227)* Credit Agreement dated as of November 2, 2011, among Cabela's Incorporated, various... -

Page 129

...and U.S. Bank National Association, as Administrative Agent (incorporated by reference from Exhibit 10.2 of our Current Report on Form 8-K, filed on November 8, 2011, File No. 001-32227) Cabela's Incorporated 2013 Stock Plan (incorporated by reference to Appendix C to our Proxy Statement on Schedule... -

Page 130

... 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized. CABELA'S INCORPORATED Dated: February 17, 2015 By: /s/ Thomas L. Millner Thomas L. Millner President and Chief Executive Officer Pursuant to the requirements of the Securities... -

Page 131

... Vice President and Chief Marketing and E-Commerce Ofï¬cer Corporate Headquarters Cabela's Incorporated One Cabela Drive Sidney, Nebraska 69160 Telephone: (308) 254-5505 Independent Registered Public Accounting Firm Deloitte & Touche LLP First National Tower 1601 Dodge Street, Suite 3100 Omaha... -

Page 132

C abe la's Inc. O ne Ca b e la Drive S id n e y, N E 6916 0 3 08 -2 5 4 -5 5 0 5 c abel as . co m NY SE :C A B