Cabela's 2014 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2014 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

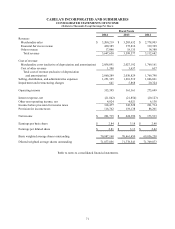

77

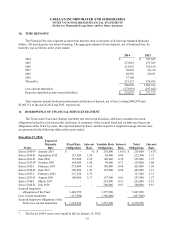

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in Thousands Except Share and Per Share Amounts)

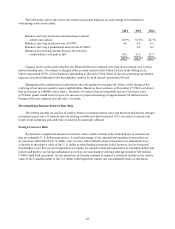

$8,269, $7,139, and $7,158 for 2014, 2013, and 2012, respectively. Redemption of these points was recognized

as revenue in merchandise sales at fair value, along with the related cost of sales. Merchandise sales recognized

from the redemption of points was $200,933, $188,634, and $164,530 for 2014, 2013, and 2012, respectively. Costs

incurred under our loyalty rewards programs recognized as a reduction in Financial Services segment revenue was

$210,190, $198,687, and $176,882 for 2014, 2013, and 2012, respectively.

Financial Services revenue includes credit card interest and fees relating to late payments, payment

assurance, and cash advance transactions. Interest and fees are accrued in accordance with the terms of the

applicable cardholder agreements on credit card loans until the date of charge-off unless placed on non-accrual

and fixed payment plans. Interchange income is earned when a charge is made to a customer’s account.

Cost of Revenue and Selling, Distribution, and Administrative Expenses – The Company’s cost of

revenue primarily consists of merchandise acquisition costs, including freight-in costs, as well as shipping costs.

The Company’s selling, distribution, and administrative expenses consist of the costs associated with selling,

marketing, warehousing, retail store replenishment, and other operating expense activities. All depreciation and

amortization expense is associated with selling, distribution, and administrative activities, and accordingly, is

included in this category in the consolidated statements of operations.

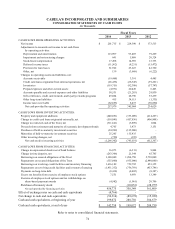

Cash and Cash Equivalents – Cash equivalents include credit card and debit card receivables from other

banks, which settle within one to four business days. Receivables from other banks totaled $22,345 and $14,209 at

the end of 2014 and 2013, respectively. Unpresented checks, net of available cash bank balances, are classified as

current liabilities. Cash and cash equivalents of the Financial Services segment were $49,294 and $94,112 at the end

of 2014 and 2013, respectively. Due to regulatory restrictions on WFB, the Company cannot use WFB’s cash for

non-banking operations.

Credit Card Loans – The Financial Services segment grants individual credit card loans to its customers and

is diversified in its lending with borrowers throughout the United States. Credit card loans are reported at their

principal amounts outstanding plus deferred credit card origination costs, less the allowance for loan losses. As part

of collection efforts, a credit card loan may be closed and placed on non-accrual or restructured in a fixed payment

plan prior to charge-off. The fixed payment plans require payment of the loan within 60 months and consist of a

lower interest rate, reduced minimum payment, and elimination of fees. Loans on fixed payment plans include

loans in which the customer has engaged a consumer credit counseling agency to assist them in managing their

debt. Customers who miss two consecutive payments once placed on a payment plan or non-accrual will resume

accruing interest at the rate they had accrued at before they were placed on a plan. Payments received on non-

accrual loans are applied to principal. The Financial Services segment does not record any liabilities for off-balance

sheet risk of unfunded commitments through the origination of unsecured credit card loans, as it has the right to

refuse or cancel these available lines of credit at any time.

The direct credit card account origination costs associated with costs of successful credit card originations

incurred in transactions with independent third parties, and certain other costs incurred in connection with credit

card approvals, are deferred credit card origination costs included in credit card loans and are amortized on a

straight-line basis over 12 months. Other account solicitation costs, including printing, list processing, and postage

are expensed as solicitation occurs.

Allowance for Loan Losses – The allowance for loan losses represents management’s estimate of probable

losses inherent in the credit card loan portfolio. The allowance for loan losses is established through a charge to the

provision for loan losses and is evaluated by management for adequacy. Loans on a payment plan or non-accrual

are segmented from the rest of the credit card loan portfolio into a restructured credit card loan segment before

establishing an allowance for loan losses as these loans have a higher probability of loss. Management estimates

losses inherent in the credit card loans segment and restructured credit card loans segment based on models which