Cabela's 2014 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2014 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

33

We continue to make progress in our print-to-digital transformation. We believe that mobile marketing and

social networking technologies will continue to build our brand, build our customer databases, and enhance the

management of contacts with our customers. We are continuing to transform our legacy catalog business into an

omni-channel enterprise supporting digital, e-commerce, and mobile capabilities while optimizing the customer

experience with our growing retail footprint. We recognize that the catalog business is mature, and we have

continued to evaluate our print programs and strategies by balancing the optimal mix of print advertising with new

emerging digital technologies.

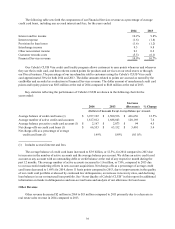

Direct segment results for 2014 compared to 2013 were as follows:

x revenue decreased $122 million, or 12.5%;

x operating income decreased $45 million, or 28.3%; and

x operating income as a percentage of Direct segment revenue decreased 290 basis points to 13.2%.

The decreases in Direct revenue and operating income were primarily due to a decrease in the hunting

equipment product category, mostly due to a substantial decrease in sales of ammunition and other shooting related

products compared to 2013, and expected cannibalization from our new retail stores.

Cabela’s CLUB continues to manage credit card delinquencies and charge-offs below industry average by

adhering to our conservative underwriting criteria and active account management. Comparing Cabela’s CLUB

results for 2014 to 2013:

x Financial Services revenue increased $55 million, or 14.5%;

x the average number of active accounts increased 7.6% to 1.8 million, and the average balance per active

account increased 4.5%;

x the average balance of our credit card loans increased 12.5% to $3.9 billion; and

x net charge-offs as a percentage of average credit card loans decreased 11 basis points to 1.69% in 2014.

In 2014, the Financial Services segment renewed one of its variable funding facilities for an additional three

years and increased the commitment from $350 million to $500 million, and completed term securitizations of

$300 million and $400 million that will mature in March 2017 and July 2019, respectively.

Current Business Environment

Macroeconomic Environment – In 2014, we experienced a decrease in sales of firearms and ammunition as

well as a challenging consumer environment across all business channels. To address these trends, we increased

our promotional activity, adjusted our marketing spending, and implemented operating expense controls to levels

consistent with how our business was performing. We will continue to manage our operating costs accordingly

in future periods. The Financial Services segment continues to monitor developments in the securitization

and certificates of deposit markets to ensure adequate access to liquidity. We expect our charge-off rates and

delinquency levels to remain below industry averages.

Developments in Legislation and Regulation – Since the latter part of 2012, there has been significant

discussion regarding enacted gun control legislation and potential gun control legislation, primarily aimed at

modern sporting rifles, certain semiautomatic pistols, and high capacity magazines. For example, the States of

Colorado, Connecticut, Maryland, and New York enacted legislation that prohibits the sale of certain high capacity

magazines and, in some cases, the sale of certain firearms. We do not expect the recently enacted state legislation

to have a significant impact on our business. Any new federal legislation that prohibits the sale of certain modern

sporting rifles, semiautomatic pistols, or ammunition could negatively impact our hunting equipment sales.

The Federal Deposit Insurance Corporation (“FDIC”) conducted compliance examinations in 2009, 2011, and

2013 and found that certain practices of WFB were improper. As a result of these compliance examinations, the

FDIC issued consent orders and WFB was required to take corrective action and pay restitution and civil money

penalties. WFB has resolved all consent requirements and is not currently subject to any consent orders.