Cabela's 2014 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2014 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

92

CABELA’S INCORPORATED AND SUBSIDIARIES

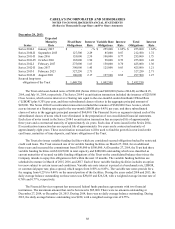

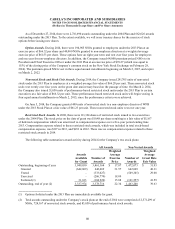

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in Thousands Except Share and Per Share Amounts)

Retail Store Properties:

In November 2006, the Company entered into agreements providing for financial incentives, including,

among other benefits, the receipt of land for a nominal amount and an incentive of $5,000 upon completion of a

new retail store. In exchange, the Company agreed to open the retail store within one year, and to refrain from

opening another retail store within a defined radius restriction area for a five year period. We opened this retail

store in November 2007. In November 2011, after attempting to negotiate a release of the radius restriction, the

Company filed a declaratory judgment action to challenge the validity and enforceability of the radius restriction.

In April 2012, we opened another retail store within the radius restriction associated with the 2007 store. On

June 18, 2013, a U. S. district court (the “Court”) ruled that the radius restriction was enforceable, but requested

additional briefing on the remaining outstanding issues. On July 30, 2013, the Court reversed its decision and

denied the defendant’s first motion for summary judgment, finding that although the Company had breached

the radius restriction, the defendant had not established its right to recovery. The defendant filed a motion for

reconsideration of the Court’s July 30, 2013, ruling and the Company filed its own motion for summary judgment.

These motions were heard on October 31, 2013. At this hearing, the Court again reversed its decision and granted

the defendant’s motion for reconsideration of the Court’s July 30, 2013, ruling, granted the defendant’s motion

for summary judgment, and denied the Company’s motion for summary judgment. This ruling resulted in the

Court ordering the Company to repay the $5,000 incentive. In addition, trial by jury was set to determine the

award related to the real property received by the Company in 2007. Trial was held beginning January 27, 2014,

and on January 31, 2014, a jury determined that the Company pay $8,625 to the defendant relating to the real

property received in 2007. On February 4, 2014, the Court entered a judgment against the Company in the amount

of $13,625. At December 28, 2013, pursuant to this judgment, the Company recognized a liability of $14,125,

including an estimated amount for legal fees and costs, in its consolidated balance sheet. The Company is currently

in the process of appealing the Court’s ruling.

Recognition of this liability at December 28, 2013, to repay these grants resulted in the Company recording

an increase to the carrying amount of the related retail store property through a reduction in deferred grant income

by the amount repayable, plus legal and other costs. The cumulative additional depreciation that would have been

recognized through December 28, 2013, as an expense in the absence of the grant was recognized in 2013 as

depreciation expense. Therefore, the adjustment that reduced the deferred grant income of this retail store property

at December 27, 2014, resulted in an increase in depreciation expense of $4,931 in 2013, which was included

in impairment and restructuring charges in the consolidated statements of income. This impairment loss was

recognized in the Retail segment.

On March 21, 2014, through a supplemental judgment, the Court ordered that the Company pay interest in

the amount of $1,062 to the defendant. At December 27, 2014, the Company’s liability relating to this judgment

totaled $15,707. The increase to this liability resulted in the Company recording an increase to the carrying amount

of the related retail store property through a reduction in deferred grant income by the additional amounts accrued,

plus legal and other costs. The additional depreciation adjustment that reduced the deferred grant income of this

retail store property resulted in an increase in depreciation expense of $831 that was recognized in the three

months ended March 29, 2014. This increase in depreciation expense was included in selling, distribution, and

administrative expenses in the consolidated statements of income and was recognized in the Retail segment. There

was no additional depreciation expense adjustments recognized after March 29, 2014.

In 2013, we also recognized an impairment loss totaling $937 related to the store closure of our former

Winnipeg, Manitoba, Canada, retail site. This impairment loss included leasehold improvements write-offs as well

as lease cancellation and restoration costs. This impairment loss was recognized in the Retail segment ($820) and

the Corporate Overhead and Other segment ($117).

Local economic trends, government regulations, and other restrictions where we own properties may impact

management projections that could change undiscounted cash flows in future periods and trigger possible future

write downs.