Cabela's 2014 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2014 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

98

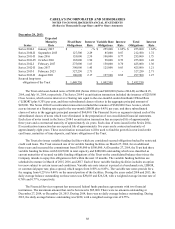

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in Thousands Except Share and Per Share Amounts)

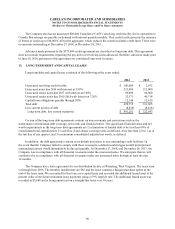

Under various grant programs, state or local governments provide funding for certain costs associated

with developing and opening a new retail store. The Company generally receives grant funding in exchange for

commitments, such as assurance of agreed employment and wage levels at the retail store or that the retail store

will remain open, made by the Company to the state or local government providing the funding. The commitments

typically phase out over approximately five to 10 years. If the Company failed to maintain the commitments

during the applicable period, the funds received may have to be repaid or other adverse consequences may arise,

which could affect the Company’s cash flows and profitability. At December 27, 2014, and December 28, 2013,

the total amount of grant funding subject to a specific contractual remedy was $44,112 and $43,536, respectively.

No grant funding subject to contractual remedy was received in 2014 or 2013. At December 27, 2014, and

December 28, 2013, the amount the Company had recorded in current liabilities in the consolidated balance sheets

relating to these grants was $22,887 and $22,536, respectively.

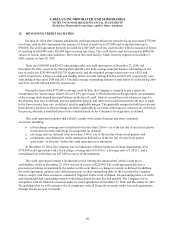

The Company operates an open account document instructions program, which provides for Cabela’s-issued

letters of credit. We had obligations to pay participating vendors $43,105 and $48,409 at December 27, 2014, and

December 28, 2013, respectively.

The Financial Services segment enters into financial instruments with off-balance sheet risk in the normal

course of business through the origination of unsecured credit card loans. Unsecured credit card accounts are

commitments to extend credit and totaled $30,491,000 and $25,255,000 at December 27, 2014, and December 28,

2013, respectively. These commitments are in addition to any current outstanding balances of a cardholder.

Unsecured credit card loans involve, to varying degrees, elements of credit risk in excess of the amount recognized

in the consolidated balance sheets. The principal amounts of these instruments reflect the Financial Services

segment’s maximum related exposure. The Financial Services segment has not experienced and does not anticipate

that all customers will exercise the entire available line of credit at any given point in time. The Financial Services

segment has the right to reduce or cancel the available lines of credit at any time.

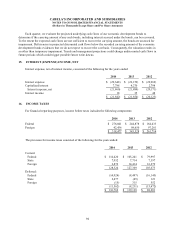

Visa Litigation Settlement – In June 2005, a number of entities, each purporting to represent a class of

retail merchants, sued Visa and several member banks, and other credit card associations, alleging, among

other things, that Visa and its member banks have violated United States antitrust laws by conspiring to fix the

level of interchange fees. On July 13, 2012, the parties to this litigation announced that they had entered into a

memorandum of understanding, which subject to certain conditions, including court approval, obligated the parties

to enter into a settlement agreement to resolve the claims brought by the class members. On December 13, 2013,

the settlement received final court approval. The settlement agreement required, among other things, (i) the

distribution to class merchants of an amount equal to 10 basis points of default interchange across all credit rate

categories for a period of eight consecutive months, which otherwise would have been paid to issuers like WFB,

(ii) Visa to change its rules to allow merchants to charge a surcharge on credit card transactions subject to a cap,

and (iii) Visa to meet with merchant buying groups that seek to negotiate interchange rates collectively. To date,

WFB has not been named as a defendant in any credit card industry lawsuits. Based on the information in the

proposed settlement, management determined that the 10 basis point reduction of default interchange across all

credit rate categories for the period of eight consecutive months from July 29, 2013, through March 28, 2014, would

result in a reduction of interchange income of approximately $12,500 in the Financial Services segment. Therefore,

a liability of $12,500 was recorded as of December 29, 2012, to accrue for this settlement.

At December 28, 2013, the remaining liability related to the settlement was $4,687, reflecting the reduction of

10 basis points of interchange fees, adjustments relating to plaintiff opt-outs of the settlement, and reevaluation of

the merchant charge volume based on Visa interchange reduction assessments. The remaining liability was settled

in the first half of 2014; therefore, at December 27, 2014, there was no remaining liability for this settlement.