Cabela's 2014 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2014 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

|

|

89

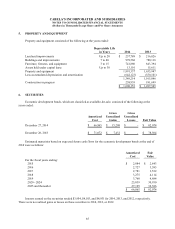

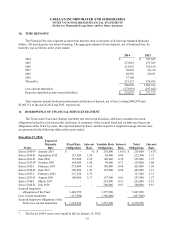

CABELA’S INCORPORATED AND SUBSIDIARIES

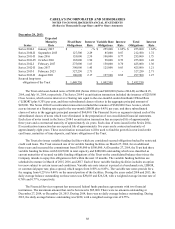

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in Thousands Except Share and Per Share Amounts)

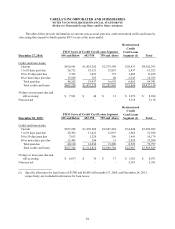

12. REVOLVING CREDIT FACILITIES

On June 18, 2014, the Company amended its credit agreement which now provides for an unsecured $775,000

revolving credit facility and permits the issuance of letters of credit up to $75,000 and swing line loans up to

$30,000. The credit agreement formerly provided for a $415,000 revolving credit facility with the issuance of letters

of credit up to $100,000 and a $20,000 limit on swing line loans. The credit facility may be increased to $800,000

subject to certain terms and conditions. The term of the credit facility, which formerly expired on November 2,

2016, expires on June 18, 2019.

There was $180,000 and $2,932 outstanding under our credit agreements at December 27, 2014, and

December 28, 2013, respectively. During 2014 and 2013, the daily average principal balance outstanding on the

line of credit was $255,499 and $130,729, respectively, and the weighted average interest rate was 1.42% and

1.44%, respectively. Letters of credit and standby letters of credit totaling $20,064 and $17,378, respectively, were

outstanding at the end of 2014 and 2013. The daily average outstanding amount of total letters of credit during 2014

and 2013 was $21,746 and $20,536, respectively.

During the term of the $775,000 revolving credit facility, the Company is required to pay a quarterly

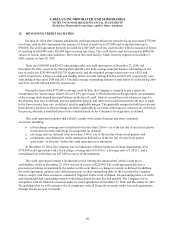

commitment fee, which ranges from 0.15% to 0.25% (previously 0.30% before the credit agreement was amended)

of the average daily unused principal balance on the line of credit. Interest on each base rate advance is equal to

the alternate base rate, as defined, plus the applicable margin; and interest on each Eurocurrency advance is equal

to the Eurocurrency base rate, as defined, plus the applicable margin. The applicable margin for both base rate and

Eurocurrency advances is the percentage rate that is applicable at such time with respect to advances as set forth in

the pricing schedule, a stratified interest rate schedule based on the Company’s leverage ratio, as defined.

The credit agreement requires that Cabela’s comply with certain financial and other customary

covenants, including:

x a fixed charge coverage ratio (as defined) of no less than 2.00 to 1 as of the last day of any fiscal quarter

for the most recently ended four fiscal quarters (as defined);

x a leverage ratio (as defined) of no more than 3.00 to 1 as of the last day of any fiscal quarter; and

x a minimum consolidated net worth standard (as defined) as of the last day of each fiscal quarter

(previously “at all times” before the credit agreement was amended).

At December 27, 2014, the Company was in compliance with the financial covenant requirements of its

$775,000 credit agreement with a fixed charge coverage ratio of 8.50 to 1, a leverage ratio of 1.20 to 1, and a

consolidated net worth that was $633,430 in excess of the minimum.

The credit agreement includes a dividend provision limiting the amount that Cabela’s could pay to

stockholders, which at December 27, 2014, was not in excess of $226,699. The credit agreement also has a

provision permitting acceleration by the lenders in the event there is a change in control, as defined. In addition,

the credit agreement contains cross default provisions to other outstanding debt. In the event that the Company

fails to comply with these covenants, a default is triggered. In the event of default, all outstanding letters of credit

and all principal and outstanding interest would immediately become due and payable. The Company was in

compliance with all financial covenants under its credit agreements at December 27, 2014, and December 28, 2013.

We anticipate that we will continue to be in compliance with all financial covenants under our credit agreements

through at least the next 12 months.