Coca Cola 2014 Annual Report Download - page 124

Download and view the complete annual report

Please find page 124 of the 2014 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

122

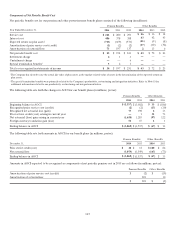

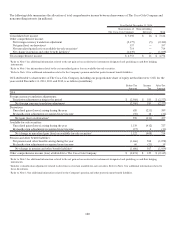

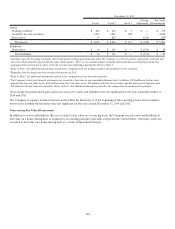

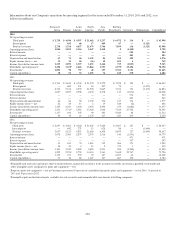

The following table presents the amounts and line items in our consolidated statements of income where adjustments reclassified from

AOCI into income were recorded during the year ended December 31, 2014 (in millions):

Description of AOCI

Component

Financial Statement Line Item

Amount Reclassified

from

AOCI into

Income

Derivatives:

Foreign currency

contracts

Net operating

revenues

$

(121)

Foreign currency and commodity contracts Cost of goods sold (37

)

Foreign currency contracts

Other income (loss) — net

108

Income before income

taxes

$

(50)

Income

taxes

18

Consolidated net

income

$

(32)

Available-for-sale securities:

Sale of

securities

Other income (loss) — net

$

(17)

Income before income

taxes

$

(17)

Income

taxes

4

Consolidated net

income

$

(13)

Pension and other benefit

liabilities:

Amortization of net actuarial loss * $ 79

Amortization of prior service cost

(credit)

* (19

)

Income before income

taxes

$

60

Income

taxes

(21

)

Consolidated net

income

$

39

* This component of AOCI is included in the Company’s computation of net periodic benefit cost and is not reclassified out of AOCI into a single line item

in our consolidated statements of income in its entirety. Refer to Note 13 for additional information.

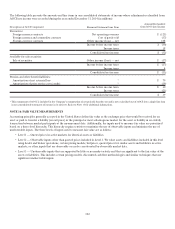

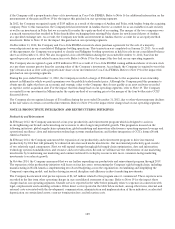

NOTE 16: FAIR VALUE MEASUREMENTS

Accounting principles generally accepted in the United States define fair value as the exchange price that would be received for an

asset or paid to transfer a liability (an exit price) in the principal or most advantageous market for the asset or liability in an orderly

transaction between market participants at the measurement date. Additionally, the inputs used to measure fair value are prioritized

based on a three-level hierarchy. This hierarchy requires entities to maximize the use of observable inputs and minimize the use of

unobservable inputs. The three levels of inputs used to measure fair value are as follows:

• Level 1 — Quoted prices in active markets for identical assets or liabilities.

• Level 2 — Observable inputs other than quoted prices included in Level 1. We value assets and liabilities included in this level

using dealer and broker quotations, certain pricing models, bid prices, quoted prices for similar assets and liabilities in active

markets, or other inputs that are observable or can be corroborated by observable market data.

• Level 3 — Unobservable inputs that are supported by little or no market activity and that are significant to the fair value of the

assets or liabilities. This includes certain pricing models, discounted cash flow methodologies and similar techniques that use

significant unobservable inputs.