Coca Cola 2014 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2014 Coca Cola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

63

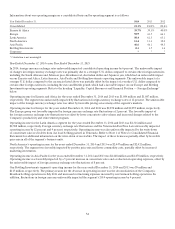

model provides the Company with an incentive to keep these bottlers viable. It is our expectation that the credit rating agencies will

continue using this methodology. If our credit ratings were to be downgraded as a result of changes in our capital structure, our major

bottlers’ financial performance, changes in the credit rating agencies’ methodology in assessing our credit strength, or for any other

reason, our cost of borrowing could increase. Additionally, if certain bottlers’ credit ratings were to decline, the Company’s equity

income could be reduced as a result of the potential increase in interest expense for those bottlers.

We monitor our financial ratios and, as indicated above, the rating agencies consider these ratios in assessing our credit ratings.

Each rating agency employs a different aggregation methodology and has different thresholds for the various financial ratios. These

thresholds are not necessarily permanent, nor are they always fully disclosed to our Company.

Our global presence and strong capital position give us access to key financial markets around the world, enabling us to raise funds at a

low effective cost. This posture, coupled with active management of our mix of short-term and long-term debt and our mix of fixed-

rate and variable-rate debt, results in a lower overall cost of borrowing. Our debt management policies, in conjunction with our share

repurchase programs and investment activity, can result in current liabilities exceeding current assets.

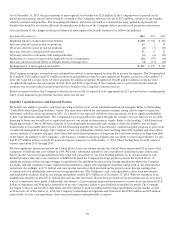

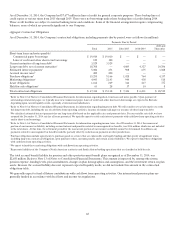

Issuances and payments of debt included both short-term and long-term financing activities. On December 31, 2014, we had

$7,677 million in lines of credit available for general corporate purposes. These backup lines of credit expire at various times from

2015 through 2019. There were no borrowings under these backup lines of credit during 2014. These credit facilities are subject to

normal banking terms and conditions.

In 2014, the Company had issuances of debt of $41,674 million, which included net issuances of $317 million of commercial paper

and short-term debt with maturities of 90 days or less and $37,799 million of issuances of commercial paper and short-term debt with

maturities greater than 90 days. The Company’s total issuances of debt also included long-term debt issuances of $3,558 million, net of

related discounts and issuance costs.

During 2014, the Company made payments of $36,962 million, which included $35,921 million for payments of commercial paper and

short-term debt with maturities greater than 90 days or less and long-term debt payments of $1,041 million.

In 2013, the Company had issuances of debt of $43,425 million, which included $35,944 million of issuances of commercial paper and

short-term debt with maturities greater than 90 days. The Company’s total issuances of debt also included long-term debt issuances of

$7,481 million, net of related discounts and issuance costs.

During 2013, the Company made payments of debt of $38,714 million, which included $70 million of net payments of commercial

paper and short-term debt with maturities of 90 days or less, $35,199 million of payments of commercial paper and short-term debt

with maturities greater than 90 days and long-term debt payments of $3,445 million. The long-term debt payments included the

extinguishment of $2,154 million of long-term debt prior to maturity, which resulted in associated charges of $53 million, including

hedge accounting adjustments reclassified from accumulated other comprehensive income, in the line item interest expense in our

consolidated statement of income during the year ended December 31, 2013.

In 2012, the Company had issuances of debt of $42,791 million, which included $40,008 million of issuances of commercial paper and

short-term debt with maturities greater than 90 days. The Company’s total issuances of debt also included long-term debt issuances of

$2,783 million, net of related discounts and issuance costs.

During 2012, the Company made payments of debt of $38,573 million. Total payments of debt included $1,553 million of net payments

of commercial paper and short-term debt with maturities of 90 days or less, and $35,118 million of payments of commercial paper and

short-term debt with maturities greater than 90 days. The Company’s total payments of debt also included long-term debt payments of

$1,902 million.

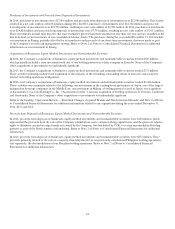

The carrying value of the Company’s long-term debt included fair value adjustments related to the debt assumed from CCE of

$464 million and $514 million as of December 31, 2014 and 2013, respectively. These fair value adjustments are being amortized

over the number of years remaining until the underlying debt matures. As of December 31, 2014, the weighted-average maturity

of the assumed debt to which these fair value adjustments relate was approximately 20 years. The amortization of these fair value

adjustments will be a reduction of interest expense in future periods, which will typically result in our interest expense being less than

the actual interest paid to service the debt. Total interest paid was $498 million, $498 million and $574 million in 2014, 2013 and 2012,

respectively. Refer to Note 10 of Notes to Consolidated Financial Statements for additional information related to the Company’s

long-term debt balances.

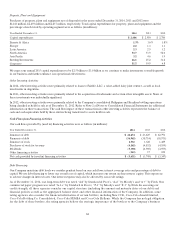

Issuances of Stock

The issuances of stock in 2014, 2013 and 2012 were primarily related to the exercise of stock options by Company employees.