Electronic Arts 2010 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2010 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

|

|

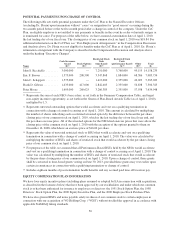

including the NEOs, contain this provision. Under the standard provisions of our employee stock option plans, an

optionee generally has three months following his or her termination of employment to exercise his or her stock

options that had vested as of his or her termination date. After three months, these options expire. For an optionee

whose length of service to the Company plus age equals 60 or above, and whose length of service is at least

10 years, this special retirement provision extends this post-termination exercise period up to 60 months

following termination of employment (but in no event beyond the original term of the stock option).

Stock Ownership Requirements

We maintain stock ownership requirements for all of our executive officers who are subject to Section 16 of the

Securities Exchange Act of 1934. These requirements are based on multiples of the executive officer’s base

salary, and range from one to six times an individual’s annual base salary depending on his or her level within

the Company. In some cases, these requirements are phased in on the basis of the executive officer’s tenure.

The Committee monitors these stock ownership requirements and believes that they further align the interests of

our executive officers with those of our stockholders. As of March 31, 2010, each of our executive officers,

including the NEOs, had either met his or her then-applicable ownership requirement or had not yet reached the

date on which he or she is required to meet his or her ownership requirement.

Stock Trading Policy

We have adopted a policy designed to promote compliance by all of our employees with both federal and state

insider trading laws. Under this policy, certain employees (including all of our executive officers) who regularly

have access to material, non-public information about the Company are prohibited from buying or selling shares

of the Company’s common stock during periods when the Company’s trading window is closed (unless such

transactions are made pursuant to a pre-approved Exchange Act Rule 10b5-1 trading plan). When the trading

window is open, these employees (including all of our executive officers) are prohibited from buying or selling

shares of the Company’s common stock while in possession of material, non-public information about the

Company and must request a trading clearance from our General Counsel prior to engaging in a trading

transaction (unless such transaction is made pursuant to a pre-approved Exchange Act Rule 10b5-1 trading plan).

In addition, we believe it is improper and inappropriate for any of our employees to engage in any transaction

designed to result in a benefit from a decline in the trading price of the Company’s common stock. As such, our

directors, executive officers, and other employees may not engage in short sales of shares of the Company’s

common stock under any circumstances, including trading in puts and calls that increase in value from a decline

in the trading price of our stock.

Tax and Accounting Policies

Section 162(m)

Section 162(m) of the Internal Revenue Code limits a public company’s ability to take a federal income tax

deduction for the remuneration of its chief executive officer and named executive officers other than its chief

financial officer (the “covered employees”) in excess of $1 million, except for certain compensation which

qualifies as “performance-based compensation”. Under this exception, certain types of performance-based

compensation in excess of $1 million are deductible if certain conditions are satisfied and the plan or

arrangement is approved by stockholders. The Executive Bonus Plan is designed to qualify for this exception;

however, no bonuses were funded and paid under the Executive Bonus Plan in fiscal 2010. Cash bonuses paid

under the Discretionary Bonus Plan in fiscal 2010 do not qualify as “performance-based compensation” within

the meaning of Section 162(m).

The Committee has structured our use of stock options in a manner intended to ensure deductibility of the

amounts realized upon an option exercise. While the Committee has the ability to grant performance-based

restricted stock units that qualify for the “performance-based compensation” exception to Section 162(m), the

Performance-Based RSUs do not qualify as “performance-based compensation” within the meaning of

Section 162(m) of the Internal Revenue Code, due to the subsequent extension to the terms of these awards to

extend the performance period by an additional two years. The Committee also reviews the terms of those

non-equity arrangements most likely to be subject to the $1 million limitation of Section 162(m).

40