General Motors 2013 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2013 General Motors annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

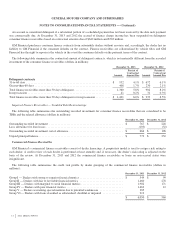

GENERAL MOTORS COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

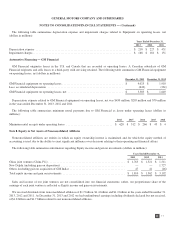

An account is considered delinquent if a substantial portion of a scheduled payment has not been received by the date such payment

was contractually due. At December 31, 2013 and 2012 the accrual of finance charge income has been suspended on delinquent

consumer finance receivables based on contractual amounts due of $642 million and $503 million.

GM Financial purchases consumer finance contracts from automobile dealers without recourse and, accordingly, the dealer has no

liability to GM Financial if the consumer defaults on the contract. Finance receivables are collateralized by vehicle titles and GM

Financial has the right to repossess the vehicle in the event the consumer defaults on the payment terms of the contract.

The following table summarizes the contractual amount of delinquent contracts, which is not materially different from the recorded

investment of the consumer finance receivables (dollars in millions):

December 31, 2013 December 31, 2012

Amount

Percent of

Contractual

Amount Due Amount

Percent of

Contractual

Amount Due

Delinquent contracts

31-to-60 days .......................................................... $ 952 4.1% $ 672 6.1%

Greater-than-60 days .................................................... 408 1.7% 230 2.1%

Total finance receivables more than 30 days delinquent ......................... 1,360 5.8% 902 8.2%

In repossession ......................................................... 41 0.2% 31 0.3%

Total finance receivables more than 30 days delinquent or in repossession .......... $ 1,401 6.0% $ 933 8.5%

Impaired Finance Receivables — Troubled Debt Restructurings

The following table summarizes the outstanding recorded investment for consumer finance receivables that are considered to be

TDRs and the related allowance (dollars in millions):

December 31, 2013 December 31, 2012

Outstanding recorded investment ................................................... $ 767 $ 228

Less: allowance for loan losses ..................................................... (103) (32)

Outstanding recorded investment, net of allowance ..................................... $ 664 $ 196

Unpaid principal balance .......................................................... $ 779 $ 232

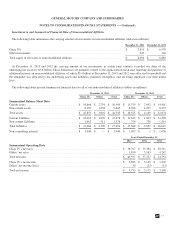

Commercial Finance Receivables

GM Financial’s commercial finance receivables consist of dealer financings. A proprietary model is used to assign a risk rating to

each dealer. A credit review of each dealer is performed at least annually and, if necessary, the dealer’s risk rating is adjusted on the

basis of the review. At December 31, 2013 and 2012 the commercial finance receivables or loans on non-accrual status were

insignificant.

The following table summarizes the credit risk profile by dealer grouping of the commercial finance receivables (dollars in

millions):

December 31, 2013 December 31, 2012

Group I — Dealers with strong to superior financial metrics .............................. $ 549 $ 99

Group II — Dealers with fair to favorable financial metrics .............................. 1,460 278

Group III — Dealers with marginal to weak financial metrics ............................. 1,982 171

Group IV — Dealers with poor financial metrics ....................................... 1,462 12

Group V — Dealers warranting special mention due to potential weaknesses ................ 385

Group VI — Dealers with loans classified as substandard, doubtful or impaired .............. 212

$ 6,050 $ 560

72

2013 ANNUAL REPORT