General Motors 2013 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2013 General Motors annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

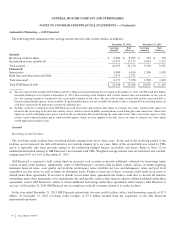

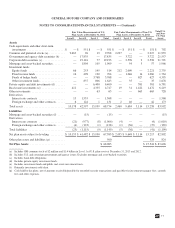

GENERAL MOTORS COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

The following table summarizes estimated amounts to be amortized from Accumulated other comprehensive loss into net periodic

benefit cost in the year ending December 31, 2014 based on December 31, 2013 plan measurements (dollars in millions):

U.S. Pension

Plans

Non-U.S. Pension

Plans

U.S. Other

Benefit Plans

Non-U.S. Other

Benefit Plans

Amortization of prior service cost (credit) .......................... $ (4) $ 19 $ (2) $ (14)

Amortization of net actuarial (gain) loss ........................... (91) 159 14 (6)

$ (95) $ 178 $ 12 $ (20)

Assumptions

Investment Strategies and Long-Term Rate of Return

Detailed periodic studies conducted by outside actuaries and an internal asset management group are used to determine the long-

term strategic mix among asset classes, risk mitigation strategies, and the expected long-term return on asset assumptions for the U.S.

pension plans. The U.S. study includes a review of alternative asset allocation and risk mitigation strategies, anticipated future long-

term performance and risk of the individual asset classes that comprise the plans’ asset mix. Similar studies are performed for the

significant non-U.S. pension plans with the assistance of outside actuaries and asset managers. While the studies incorporate data

from recent plan performance and historical returns, the expected long-term return on plan asset assumptions are determined based on

long-term, prospective rates of return.

The strategic asset mix and risk mitigation strategies for the plans are tailored specifically for each plan. Individual plans have

distinct liabilities, liquidity needs, and regulatory requirements. Consequently, there are different investment policies set by individual

plan fiduciaries. Although investment policies and risk mitigation strategies may differ among plans, each investment strategy is

considered to be appropriate in the context of the specific factors affecting each plan.

In setting new strategic asset mixes, consideration is given to the likelihood that the selected mixes will effectively fund the

projected pension plan liabilities, while aligning with the risk tolerance of the plans’ fiduciaries. The strategic asset mixes for U.S.

defined benefit pension plans are increasingly designed to satisfy the competing objectives of improving funded positions (market

value of assets equal to or greater than the present value of the liabilities) and mitigating the possibility of a deterioration in funded

status.

Derivatives may be used to provide cost effective solutions for rebalancing investment portfolios, increasing or decreasing exposure

to various asset classes and for mitigating risks, primarily interest rate and currency risks. Equity and fixed income managers are

permitted to utilize derivatives as efficient substitutes for traditional physical securities. Interest rate derivatives may be used to adjust

portfolio duration to align with a plan’s targeted investment policy. Alternative investment managers are permitted to employ

leverage, including through the use of derivatives, which may alter economic exposure.

In December 2013 an investment policy study was completed for the U.S. pension plans. The study resulted in new target asset

allocations being approved for the U.S. pension plans with resulting changes to the expected long-term rate of return on assets. The

weighted-average long-term rate of return on assets increased from 5.8% at December 31, 2012 to 6.5% at December 31, 2013 due

primarily to higher yields on fixed income securities. The expected long-term rate of return on plan assets used in determining pension

expense for non-U.S. plans is determined in a similar manner to the U.S. plans.

97