General Motors 2013 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2013 General Motors annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

GENERAL MOTORS COMPANY AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

declined notwithstanding our actions. As a result we performed a recoverability test of the GME asset group by weighting various

undiscounted cash flow scenarios and concluded the GME asset group was not recoverable. Accordingly we recorded asset

impairment charges of $3.7 billion at December 31, 2012 to adjust the carrying amount of the GME real and personal property to fair

value of $0.4 billion. These charges were recorded in our GME segment with $3.5 billion recorded in Automotive cost of sales and

$0.2 billion recorded in Automotive selling, general and administrative expense. Our recoverability test of the GME asset group also

included Intangible assets, net and other long-lived assets resulting in additional impairment charges of $1.8 billion, for total

impairment charges of $5.5 billion. Refer to Note 11 for additional information regarding the impairment of Intangible assets, net.

Fair Value Measurements

To determine the estimated fair value of real and personal property, the cost approach, market approach and income approach were

considered. Under the cost approach, the determination of fair value considered the estimates of the cost to construct or purchase a

new asset of equal utility at current prices with adjustments in value for physical deterioration, functional obsolescence, and economic

obsolescence. Under the market approach, the determination of fair value considered the market prices in transactions for similar

assets and certain direct market values based on quoted prices from brokers and secondary market participants for similar assets.

Under the income approach, the determination of fair value considered the estimate of the present worth of future benefits derived

from ownership, usually measured through the capitalization of a specific level of income which can be derived from the subject asset

with adjustments in value for demolition costs and for the effect of an estimated holding period. Under the income approach, it was

assumed fair value could not exceed the present value of the net cash flows discounted at a rate commensurate with the level of risk

inherent in the subject asset. An in-exchange premise was determined to be the highest and best use.

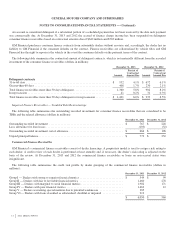

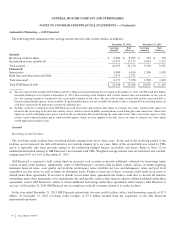

The following table summarizes the significant Level 3 inputs for real and personal property measurements:

Valuation Technique(s) Unobservable Input(s) Range

GM India personal property ............................ Market approach Economic obsolescence (a) 72% - 100%

Holden real property .................................. Income approach Holding period (b) 0 - 3 years

Discount rate (c) 11% - 12%

GME real property ................................... Market approach Demolition costs (d) 6% - 23%

Cost approach Holding period (b) 0 - 4 years

Income approach Discount rate (c) 11.2% - 14.5%

GME personal property ............................... Market approach Physical deterioration (e) 52% - 69%

Cost approach Functional obsolescence (f) 8% - 28%

Economic obsolescence (a) 17% - 23%

(a) Represents estimated loss in asset value caused by factors external to the asset such as legislative enactments, changes in use, social change and

change in supply and demand.

(b) Represents estimated marketing period for each property which dictates the amount of property specific holding costs to be incurred such as real

estate taxes.

(c) Represents the discount rate for the specific property based on local market sources and available benchmarking data.

(d) Represents estimated gross cost to demolish and clear the structures on the property as a percentage of replacement cost new.

(e) Represents estimated loss in asset value due to wear and tear, action of the elements and other physical factors that reduce the life and

serviceability of the asset.

(f) Represents estimated loss in asset value caused by inefficiencies and inadequacies of the asset itself.

The personal property in our Holden asset group was determined to have a nominal fair value because of anticipated losses during

the wind-down period and limited to no salvage value given the decline in the automotive manufacturing base in Australia.

80

2013 ANNUAL REPORT