Humana 2005 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2005 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

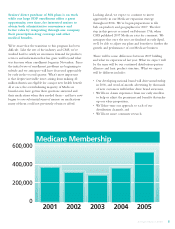

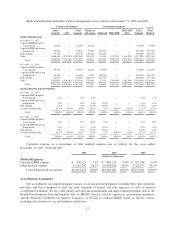

PPO plans. Prior to 2006, PPO plans were offered on a local basis only. Most Medicare Advantage plans must

offer the prescription drug benefit as part of the basic plan, subject to cost sharing and other limitations. Medicare

Advantage plans may charge beneficiaries monthly premiums and other copayments for Medicare-covered

services or for certain extra benefits.

Our Medicare HMO and PPO plans, which cover Medicare-eligible individuals residing in certain counties,

may eliminate or reduce coinsurance or the level of deductibles on many other medical services while seeking

care from participating in-network providers, or in emergency situations. Except in emergency situations, HMO

plans provide no out-of-network benefits. PPO plans carry an out-of network benefit that is subject to higher

member cost-sharing. In many cases, these beneficiaries also may be required to pay a monthly premium to the

HMO or PPO plan, in addition to the monthly Part B premium they are required to pay the Medicare program.

Our Medicare PFFS plans, which cover eligible Medicare beneficiaries in certain states, have no preferred

network. Individuals in these plans pay us a monthly premium to receive enhanced prescription drug benefits and

have the freedom to choose any health care provider that accepts individuals at reimbursement rates equivalent to

traditional Medicare payment rates.

Medicare uses monthly rates per person for each county to determine the fixed monthly payments per

member to pay to managed care plans. In the last decade, Congress has made several changes to how CMS must

calculate these rates. The old (pre-1998) methodology was based on the Adjusted Average Per Capita Cost

methodology, or AAPCC. Under AAPCC, CMS projected average county-level fee-for-service spending for the

coming year to set the fixed monthly payments for Medicare health plans at 95 percent of the full AAPCC

amount.

Under the AAPCC system, payment rates per county varied widely. For example, the 1997 payment rate for

beneficiaries 65 and older for Part A and Part B services ranged from a low of $220.92 in Arthur County,

Nebraska to a high of $767.35 in Richmond County, Staten Island, New York. Some states saw differences of

more than 20 percent between adjacent counties. Since county fee-for-service costs were used to estimate county

managed care payment rates, the rates reflected differences among counties and regions in fee-for-service

utilization patterns and cost structures.

In the Balanced Budget Act of 1997 (BBA), Congress created a new rate-setting methodology, eliminating

the direct link in the AAPCC method between managed care rates and local fee-for-service costs. As a result, the

wide disparities in county payment rates were reduced, bringing all payment rates closer to the national average.

Additionally, the BBA required CMS to implement a risk adjustment payment system for Medicare health

plans. Risk adjustment uses health status indicators to improve the accuracy of payments and establish incentives

for plans to enroll and treat less healthy Medicare beneficiaries. CMS initially phased-in this payment

methodology with a risk adjustment model that based payment on principal hospital inpatient diagnoses, as well

as demographic factors such as gender, age, and Medicaid eligibility. From 2000 to 2003, risk adjusted payment

accounted for only 10 percent of Medicare health plans payment, with the remaining 90 percent being based on

demographic factors.

Pursuant to the Benefits and Improvements Protection Act of 2000 (BIPA), CMS implemented a new risk

adjustment model that uses additional diagnosis data from ambulatory treatment settings (hospital outpatient

department and physician visits). CMS has also redesigned its data collection and processing system to further

reduce administrative data burden on Medicare health plans. In 2005, the portion of risk adjusted payment was

increased to 50 percent, from 30 percent in 2004. The phase-in of risk adjusted payment will be increased to 75%

in 2006 and to 100% in 2007. Under the new risk adjustment methodology, all managed care organizations must

capture, collect, and submit the necessary diagnosis code information to CMS within prescribed deadlines.

Commensurate with phase-in of the new risk-adjustment methodology, payments to Medicare Advantage

plans have been increased by a “budget neutrality” factor. The budget neutrality factor was implemented to

prevent overall health plan payments from being reduced during the transition to the new risk-adjustment

5