Humana 2005 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2005 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

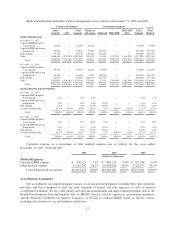

|

|

CMS regulations require submission of quarterly and annual financial statements. In addition, CMS requires

certain disclosures to CMS and to Medicare beneficiaries concerning operations of a health plan contracted under

the Medicare program. CMS’s rules require disclosure to members upon request of information concerning

financial arrangements and incentive plans between the plan and physicians in the plan’s networks. These rules

also require certain levels of stop loss coverage to protect contracted physicians against major losses relating to

patient care, depending on the amount of financial risk they assume. The reporting of certain health care data

contained in HEDIS is another important CMS disclosure requirement.

Fraud and abuse laws

Enforcement of health care fraud and abuse laws has become a top priority for the nation’s law enforcement

entities. The funding of such law enforcement efforts has increased dramatically in the past few years and is

expected to continue. The focus of these efforts has been directed at participants in federal government health

care programs such as Medicare, Medicaid, and the FEHBP. We participate extensively in these programs and

have continued our stringent regulatory compliance efforts for these programs. The programs are subject to very

technical rules. When combined with law enforcement intolerance for any level of noncompliance, these rules

mean that compliance efforts in this area continue to be challenging.

Federal HMO Act

Of our nine licensed and active HMO subsidiaries as of February 1, 2006, eight are qualified under the

Federal Health Maintenance Organization Act of 1973, as amended. To obtain federal qualification, an HMO

must meet certain requirements, including conformance with benefit, rating, and financial reporting standards.

Federal qualification allows us to participate in the FEHBP program. In certain markets, and for certain products,

we operate HMOs that are not federally qualified because this provides greater flexibility with respect to product

design and pricing than is possible for federally qualified HMOs.

Privacy regulations

The use of individually identifiable data by our business is regulated at federal and state levels. These laws

and rules are changed frequently by legislation or administrative interpretation. Various state laws address the

use and maintenance of individually identifiable health data. Most are derived from the privacy provisions in the

federal Gramm-Leach-Bliley Act and the Health Insurance Portability and Accountability Act of 1996, or

HIPAA. HIPAA includes administrative provisions directed at simplifying electronic data interchange through

standardizing transactions, establishing uniform health care provider, payer, and employer identifiers and seeking

protections for confidentiality and security of patient data. Violations of these rules could subject us to significant

penalties.

State and local regulation

We are also subject to substantial regulation by the states in which we do business. We regularly are audited

and subject to various enforcement actions by state departments of insurance. These departments enforce laws

relating to all aspects of our operations, including benefit offerings, marketing, claim payments and premium

setting, especially with regard to our small group business. Although any of the pending government actions

could result in assessment of damages, civil or criminal fines or penalties, and other sanctions against us,

including exclusion from participation in government programs, we do not believe the results of any of these

actions, individually or in the aggregate, will have a material adverse effect on our financial position, results of

operations, or cash flows.

Our Medicaid products are regulated by the applicable state agency in the state in which we sell a Medicaid

product and by the Puerto Rico Health Insurance Administration, in conformance with federal approval of the

applicable state plan, and are subject to periodic reviews by these agencies. The reviews are similar in nature to

those performed by CMS.

15