Humana 2005 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2005 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

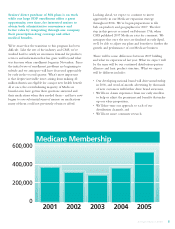

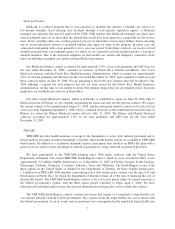

|

|

200,000

0

400,000

600,000 Medicare Membership

2001 2002 2003 2004 2005

2 Annual Report 2005 5

Seniors’ direct purchase of MA plans is on track

while our large PDP enrollment offers a great

opportunity, over time, for interested seniors to

obtain both administrative convenience and

better value by integrating through one company

their prescription drug coverage and other

medical benefi ts.

We’re aware that the transition to this program has been

diffi cult. Like the rest of the industry and CMS, we’ve

worked hard to satisfy an enormous demand for products,

services and information that has gone well beyond what

was foreseen when enrollment began in November. Since

the initial wave of enrollment, problems are beginning to

subside and we anticipate will have decreased appreciably

by early in the second quarter. What’s most important

is that despite inevitable issues arising from making 42

million Americans eligible for a major new health benefi t

all at once, the overwhelming majority of Medicare

benefi ciaries have gotten their questions answered and

their medications when they needed them – and have now

begun to save substantial sums of money on medications

many of them could not previously obtain or afford.

Looking ahead, we expect to continue to invest

aggressively in our Medicare expansion strategy

throughout 2006. We’ve begun preparations to fi le

bids on products and geographies for 2007. The fi rst

step in this process occurred on February 17th, when

CMS published 2007 Medicare rates for comment. We

anticipate that once the rates are fi nalized in early April,

we’ll be able to adjust our plans and benefi ts to further the

growth and performance of our Medicare business.

There will be some differences between 2007 bidding

and what we experienced last year. What we expect will

be the same will be our continued distribution-partner

alliances and basic product structure. What we expect

will be different includes:

• Our developing national brand will drive membership

in 2006, and word-of-mouth advertising by thousands

of new customers will further drive brand awareness,

• We’ll have claims experience from our early enrollees

to help us adjust the premiums and benefi ts that make

up our value proposition,

• We’ll fi ne-tune our approach to each of our

distribution channels, and

• We’ll have more consumer research.