Humana 2005 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2005 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

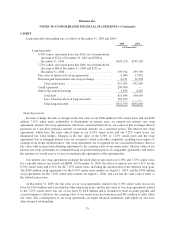

Humana Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Stock-Based Compensation

We have stock-based employee compensation plans, which are described more fully in Note 11. We account

for stock options granted to our employees under Accounting Principles Board Opinion No. 25, Accounting for

Stock Issued to Employees and related interpretations, or APB No. 25. No employee compensation cost is

reflected in net income related to fixed-based stock option awards because these options had an exercise price

equal to the market value of the underlying common stock on the date of grant. Generally, if a fixed-based stock

option award is subsequently modified, compensation expense, if any, is recorded for the amount that the market

price of Humana common stock exceeds the option’s exercise price on the date the option is modified.

Compensation expense for performance-based stock options is recognized over the performance period which

varies based on the market value of the underlying common stock at the end of each period. Compensation

expense is recorded for restricted stock grants ratably over their vesting periods, generally three years from the

date of grant, based on fair value, which is equal to the market price of Humana common stock on the date of the

grant. The effect on net income and earnings per common share if we had applied the fair value recognition

provisions of SFAS No. 123, Accounting for Stock-Based Compensation, or SFAS 123, to our fixed-based stock

option awards using the Black-Scholes pricing model was as follows for the years ended December 31, 2005,

2004 and 2003.

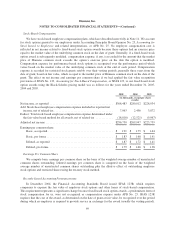

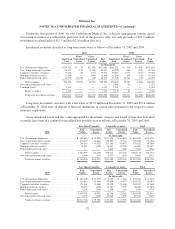

2005 2004 2003

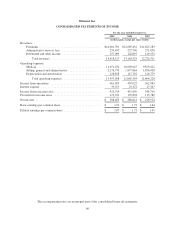

(in thousands, except per share

results)

Net income, as reported ........................................... $308,483 $280,012 $228,934

Add: Stock-based employee compensation expense included in reported net

income, net of related tax ........................................ 7,063 2,456 3,872

Deduct: Total stock-based employee compensation expense determined under

the fair value based method for all awards, net of related tax ............ (18,816) (12,521) (9,067)

Adjusted net income .............................................. $296,730 $269,947 $223,739

Earnings per common share:

Basic, as reported ............................................ $ 1.91 $ 1.75 $ 1.44

Basic, pro forma ............................................. $ 1.83 $ 1.68 $ 1.41

Diluted, as reported .......................................... $ 1.87 $ 1.72 $ 1.41

Diluted, pro forma ........................................... $ 1.79 $ 1.66 $ 1.38

Earnings Per Common Share

We compute basic earnings per common share on the basis of the weighted average number of unrestricted

common shares outstanding. Diluted earnings per common share is computed on the basis of the weighted

average number of unrestricted common shares outstanding plus the dilutive effect of outstanding employee

stock options and restricted shares using the treasury stock method.

Recently Issued Accounting Pronouncements

In December 2004, the Financial Accounting Standards Board issued SFAS 123R, which requires

companies to expense the fair value of employee stock options and other forms of stock-based compensation.

This requirement represents a significant change because fixed-based stock option awards, a predominate form of

stock compensation for us, were not recognized as compensation expense under APB No. 25. SFAS 123R

requires that the cost of the award, as determined on the date of grant at fair value, be recognized over the period

during which an employee is required to provide service in exchange for the award (usually the vesting period).

69