Humana 2005 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2005 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

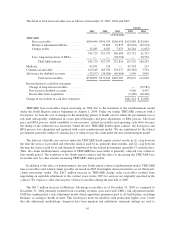

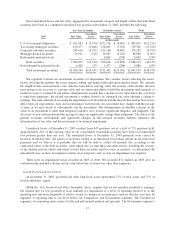

The CMS risk adjustment model pays more for members with predictably higher costs, as more fully

described on page 5. Under this risk adjustment methodology, diagnosis data from inpatient and ambulatory

treatment settings are used to calculate the risk adjusted premium payment to us. We collect, capture, and submit

the necessary diagnosis data to CMS within prescribed deadlines. We estimate risk adjustment revenues based

upon the diagnosis data submitted to CMS and ultimately accepted by CMS.

CMS is transitioning to the risk adjustment model while the old demographic model is phased out. The

demographic model based the monthly premiums paid to health plans on factors such as age, sex and disability

status. The monthly premium amount for each member is separately determined under both the risk adjustment

and demographic model. These separate payment amounts are then blended according to the transition schedule.

CMS is transitioning to the risk adjustment model for Medicare Advantage plans as follows: 50% in 2005, 75%

in 2006 and 100% in 2007. The PDP payment methodology is based 100% on the risk adjustment model

beginning in 2006. As a result of this process and the phasing in of the risk adjustment model, as well as budget

neutrality as described on page 5, our CMS monthly premium payments per member may change materially,

either favorably or unfavorably.

Premium revenues and ASO fees are estimated by multiplying the membership covered under the various

contracts by the contractual rates. In addition, we adjust revenues for estimated changes in an employer’s

enrollment and customers that ultimately may fail to pay. Enrollment changes not yet reported by an employer

group, an individual, or the government, also known as retroactive membership adjustments, are estimated based

on historical trends. We monitor the collectibility of specific accounts, the aging of receivables, as well as

prevailing and anticipated economic conditions, and reflect any required adjustments in the current period’s

revenue.

We bill and collect premium and ASO fee remittances from employer groups, the federal and state

governments, and individual Medicare Advantage members monthly. Premium and ASO fee receivables are

presented net of allowances for estimated uncollectible accounts and retroactive membership adjustments.

Premiums and ASO fees received prior to the period members are entitled to receive services are recorded as

unearned revenues.

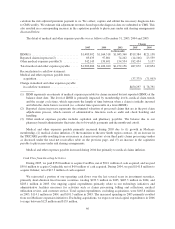

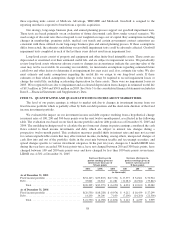

TRICARE Contract

In 2005, TRICARE revenues represented 17% of total premiums and administrative services fees. The

single TRICARE contract for the South Region includes multiple revenue generating activities and as such was

evaluated under Emerging Issues Task Force (EITF) Issue No. 00-21, Accounting for Revenue Arrangements

with Multiple Deliverables. We allocate the consideration to the various components based on the relative fair

values of the components. TRICARE revenues consist generally of (1) an insurance premium for assuming

underwriting risk for the cost of civilian health care services delivered to eligible beneficiaries; (2) health care

services provided to beneficiaries which are in turn reimbursed by the federal government; and (3) administrative

service fees related to claim processing, customer service, enrollment, disease management and other services.

We recognize the insurance premium as revenue ratably over the period coverage is provided. Health care

services reimbursements are recognized as revenue in the period health care services are provided.

Administrative service fees are recognized as revenue in the period services are performed.

The TRICARE contract contains provisions whereby the federal government bears a substantial portion of

the risk associated with financing the cost of health benefits. Annually, we negotiate a target health care cost

amount, or target cost, with the federal government and determine an underwriting fee. Any variance from the

target cost is shared. We earn more revenue or incur additional costs based on the variance in actual health care

costs versus the negotiated target cost. We receive 20% for any cost underrun, subject to a ceiling that limits the

underwriting profit to 10% of the target cost. We pay 20% for any cost overrun, subject to a floor that limits the

underwriting loss to negative 4% of the target cost. A final settlement occurs 12 to 18 months after the end of

each contract year to which it applies. We defer the recognition of any revenues for favorable contingent

underwriting fee adjustments related to cost underruns until the amount is determinable and the collectibility is

55