Humana 2005 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2005 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

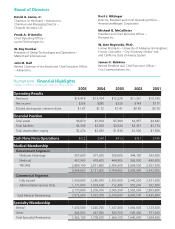

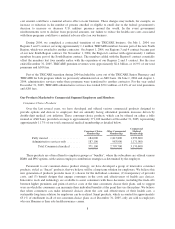

Commercial Segment

The Commercial segment in 2005 saw membership

increases in our three areas of strategic focus:

Administrative Services Only (ASO), individual and

consumer plans. The company’s HumanaOne individual

product membership grew 25 percent year-over-year,

ASO membership grew by 15 percent and consumer-

choice membership was up 52 percent in 2005. Growth

in each of these areas is consistent with our ongoing

Commercial strategy of migrating our group book of

business away from fully insured slice accounts and

toward self-funded and higher-margin consumer offerings

(including our Smart product family), while at the same

time expanding the membership and geographic reach of

our individual plans.

Much has been said of the market for consumer-oriented

health benefi ts. As a leader as well as an early entrant in

this fi eld, we’ve taken a keen interest in the developing

dialogue, and in the related phenomenon of a growing

convergence between health services and fi nancial services

through Flexible Spending Accounts (FSAs), Health

Savings Accounts (HSAs) and other tax-advantaged

funding arrangements. Here is our view of consumer

plans’ immediate prospects:

• First, the market is moving in the right direction and

we’re seeing numerous competitors get into this space,

which benefi ts us both by building market momentum

and by validating our strategy.

• However, there’s still a lot more talk than action. Most

of the focus on consumerism is on modest product

enhancement and cost shifting, rather than on a full-

scale adoption of real consumer engagement, in line

with the way we view the business.

• Employers are realizing that consumerism is the wave of

the future and we’re starting to see the erosion of their

reluctance to embrace change.

• HSAs will increasingly be a driving force in this

business and will be pivotal in getting consumers and

employers to adopt consumerism.

• Insurers who have not embraced the consumer

and have not invested in consumer-empowering

technologies will fall by the wayside.

We believe employers eventually will opt in great numbers

for a holistic total solution where permanent savings come

not from cost-shifting but from turning passive health-care

users into active health-care consumers through actionable

information. Our Smart approach is just such a solution,

with sustained mid-single-digit medical cost trend for our

Smart customers over multiple years. This compares to an

overall medical cost trend over the same period of

between 11 and 14 percent annually. We’re committed

to this approach on a long-term basis because it works,

because the market for it is large and because we’re

starting to see employers come around to it.

$2.5

$0

$5.0

$7.5 Total Assets (in Billions)

2001 2002 2003 2004 2005

6 Annual Report 2005