Proctor and Gamble 2013 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2013 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

The Procter & Gamble Company 33

disproportionate growth in developing regions, which have

lower than segment average selling prices. Global market

share of the Beauty segment decreased 0.3 points. Volume

increased mid-single digits in developing regions while

developed region volume decreased low single digits.

Volume in Hair Care and Color grew mid-single digits

behind high single-digit growth in developing regions led by

Pantene initiatives and Head & Shoulders geographic

expansion. Volume in developed regions was down low

single digits due to competitive activity. Global market

share of the hair care category was unchanged. Volume in

Beauty Care decreased mid-single digits due to the Zest and

Infasil divestitures and the impact of competitive activity in

North America and Western Europe which contributed to

about half a point of global share loss. Volume in Salon

Professional was down high single digits mainly due to

market contraction in Europe and the impact of competitive

activity. Volume in Prestige Products increased mid-single

digits driven by initiative activity, partially offset by minor

brand divestitures.

Net earnings decreased 6% to $2.4 billion as higher net sales

were more than offset by a 100-basis point decrease in net

earnings margin. Net earnings margin decreased due to

gross margin contraction partially offset by lower SG&A as

a percentage of net sales. Gross margin decreased primarily

due to an increase in commodity costs and unfavorable

geographic and product mix, partially offset by

manufacturing cost savings and higher pricing. SG&A as a

percentage of net sales decreased due to scale leverage from

increased sales.

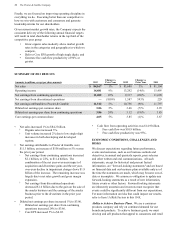

GROOMING

($ millions) 2013

Change vs

2012 2012

Change vs

2011

Volume n/a -1% n/a +1%

Net sales $8,038 -4% $8,339 +1%

Net earnings $1,837 +2% $1,807 +2%

% of Net Sales 22.9% 120 bps 21.7% 10 bps

Fiscal year 2013 compared with fiscal year 2012

Grooming net sales decreased 4% to $8.0 billion in 2013 on

a 1% decrease in unit volume. Organic sales were up 2% on

organic volume that was in line with the prior year period.

Price increases contributed 2% to net sales growth.

Unfavorable foreign exchange reduced net sales by 4%. The

impact of the Braun household appliances business

divestiture reduced net sales by 1%. Global market share of

the Grooming segment increased 0.4 points. Volume

increased low single digits in developing regions and

decreased mid-single digits in developed regions. Shave

Care volume increased low single digits due to low single-

digit growth in developing regions, primarily behind market

growth and innovation expansion, partially offset by a low

single-digit decrease in developed regions primarily due to

market contraction in Western Europe. Global market share

of the blades and razors category was up less than half a

point. Volume in Appliances decreased double digits due to

the sale of the Braun household appliances business,

competitive activity and market contraction. Organic

volume in Appliances declined high single digits. Global

market share of the appliances category decreased nearly

half a point.

Net earnings increased 2% to $1.8 billion due to a 120-basis

point increase in net earnings margin, partially offset by the

decrease in net sales. Net earnings margin increased

primarily due to gross margin expansion. Gross margin

increased due to pricing and manufacturing cost savings.

SG&A as a percentage of net sales decreased nominally as

increased marketing spending was offset by reduced

overhead costs.

Fiscal year 2012 compared with fiscal year 2011

Grooming net sales increased 1% to $8.3 billion in 2012 on

a 1% increase in unit volume. Organic sales were up 2%.

Price increases contributed 2% to net sales growth.

Unfavorable geographic and product mix decreased net sales

by 1% mainly due to disproportionate growth in developing

markets, which have lower than segment average selling

prices. Unfavorable foreign exchange decreased net sales

growth by 1%. Global market share of the Grooming

segment decreased 0.2 points. Volume grew mid-single

digits in developing regions due to initiative activity and

market growth and decreased low single digits in developed

regions primarily due to competitive activity. Volume in

Shave Care was up low single digits due to mid-single-digit

growth in developing regions behind initiatives, Fusion

ProGlide geographic expansion and market growth, partially

offset by a low single-digit decrease in developed regions

due to market contraction and the impact of competitive

activity. Global market share of the blades and razors

category was unchanged. Volume in Appliances decreased

mid-single digits due to market contraction in Western

Europe and the impact of competitive activity. Global

market share of the dry shave category was down over 2

points.

Net earnings increased 2% to $1.8 billion due to higher net

sales and a 10-basis point increase in net earnings margin.

The net earnings margin increase was driven by a decrease

in SG&A as a percentage of net sales, largely offset by gross

margin contraction. SG&A as a percentage of net sales

decreased due to reductions in both overhead and marketing

spending. Gross margin decreased primarily due to an

increase in commodity costs and unfavorable geographic and

product mix, partially offset by price increases.