Proctor and Gamble 2013 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2013 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

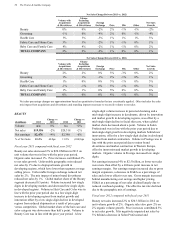

38 The Procter & Gamble Company

cash in 2012 primarily for the acquisition of New Chapter, a

vitamins supplement business.

Proceeds from Divestitures and Other Asset Sales.

Proceeds from asset sales contributed $584 million in cash in

2013 mainly due to the divestitures of our bleach business in

Italy and the Braun household appliances business. Proceeds

from asset sales contributed $2.9 billion to cash in 2012

mainly due to the sale of our snacks business.

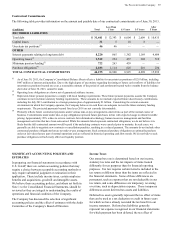

Financing Cash Flows

Dividend Payments. Our first discretionary use of cash is

dividend payments. Dividends per common share increased

7% to $2.29 per share in 2013. Total dividend payments to

common and preferred shareholders were $6.5 billion in

2013 and $6.1 billion in 2012. In April 2013, the Board of

Directors declared an increase in our quarterly dividend

from $0.5620 to $0.6015 per share on Common Stock and

Series A and B ESOP Convertible Class A Preferred Stock.

This represents a 7% increase compared to the prior

quarterly dividend and is the 57th consecutive year that our

dividend has increased. We have paid a dividend in every

year since our incorporation in 1890.

Long-Term and Short-Term Debt. We maintain debt levels

we consider appropriate after evaluating a number of factors,

including cash flow expectations, cash requirements for

ongoing operations, investment and financing plans

(including acquisitions and share repurchase activities) and

the overall cost of capital. Total debt was $31.5 billion as of

June 30, 2013 and $29.8 billion as of June 30, 2012. Our

total debt increased in 2013 mainly due to debt issuances

and an increase in commercial paper outstanding, partially

offset by bond maturities.

Treasury Purchases. Total share repurchases were $6.0

billion in 2013 and $4.0 billion in 2012.

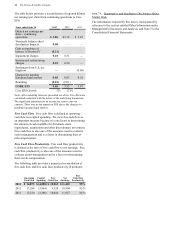

Liquidity

At June 30, 2013, our current liabilities exceeded current

assets by $6.0 billion, largely due to short-term borrowings

under our commercial paper program. We anticipate being

able to support our short-term liquidity and operating needs

largely through cash generated from operations.

Additionally, a portion of our cash is held off-shore by

foreign subsidiaries. The Company regularly assesses its

cash needs and the available sources to fund these needs and

we do not expect restrictions or taxes on repatriation of cash

held outside of the United States to have a material effect on

our overall liquidity, financial condition or the results of

operations for the foreseeable future. We utilize short- and

long-term debt to fund discretionary items, such as

acquisitions and share repurchases. We have strong short-

and long-term debt ratings, which have enabled and should

continue to enable us to refinance our debt as it becomes due

at favorable rates in commercial paper and bond markets. In

addition, we have agreements with a diverse group of

financial institutions that, if needed, should provide

sufficient credit funding to meet short-term financing

requirements.

On June 30, 2013, our short-term credit ratings were P-1

(Moody's) and A-1+ (Standard & Poor's), while our long-

term credit ratings are Aa3 (Moody's) and AA- (Standard &

Poor's), both with a stable outlook.

We maintain bank credit facilities to support our ongoing

commercial paper program. The current facility is an $11.0

billion facility split between a $7.0 billion 5-year facility and

a $4.0 billion 364-day facility, which expire in August 2018

and August 2014, respectively. The 364-day facility can be

extended for certain periods of time as specified in, and in

accordance with, the terms of the credit agreement. These

facilities are currently undrawn and we anticipate that they

will remain largely undrawn for the foreseeable future.

These credit facilities do not have cross-default or ratings

triggers, nor do they have material adverse events clauses,

except at the time of signing. In addition to these credit

facilities, we have an automatically effective registration

statement on Form S-3 filed with the SEC that is available

for registered offerings of short- or long-term debt securities.

Guarantees and Other Off-Balance Sheet Arrangements

We do not have guarantees or other off-balance sheet

financing arrangements, including variable interest entities,

which we believe could have a material impact on financial

condition or liquidity.