Proctor and Gamble 2013 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2013 Proctor and Gamble annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

68 The Procter & Gamble Company

Amounts in millions of dollars except per share amounts or as otherwise specified.

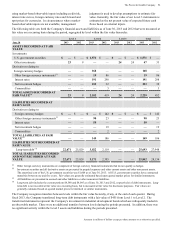

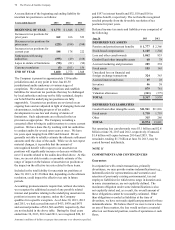

Net Periodic Benefit Cost. Components of the net periodic benefit cost were as follows:

Pension Benefits Other Retiree Benefits

Years ended June 30 2013 2012 2011 2013 2012 2011

AMOUNTS RECOGNIZED IN NET PERIODIC BENEFIT COST

Service cost $ 300 $ 267 $ 270 $ 190 $ 142 $ 146

Interest cost 560 611 588 260 276 270

Expected return on plan assets (587)(573)(492)(382)(434)(431)

Prior service cost /(credit) amortization 18 21 18 (20)(20)(18)

Net actuarial loss amortization 213 102 154 199 99 96

Special termination benefits 39 —— 18 27 3

Curtailments, settlements and other 46— ———

GROSS BENEFIT COST 547 434 538 265 90 66

Dividends on ESOP preferred stock ——— (70)(74)(79)

NET PERIODIC BENEFIT COST/(CREDIT) 547 434 538 195 16 (13)

CHANGE IN PLAN ASSETS AND BENEFIT

OBLIGATIONS RECOGNIZED IN AOCI

Net actuarial loss /(gain) - current year 264 2,009 (1,594)1,516

Prior service cost/(credit) - current year 104 (44)——

Amortization of net actuarial loss (213)(102)(199)(99)

Amortization of prior service (cost) / credit (18)(21)20 20

Settlement / curtailment cost (4)(6)——

Currency translation and other (2)(234)1(36)

TOTAL CHANGE IN AOCI 131 1,602 (1,772)1,401

NET AMOUNTS RECOGNIZED IN PERIODIC BENEFIT

COST AND AOCI 678 2,036 (1,577)1,417

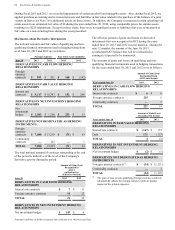

Amounts expected to be amortized from AOCI into net periodic benefit cost during the year ending June 30, 2014, are as

follows:

Pension Benefits Other Retiree Benefits

Net actuarial loss $ 210 $ 118

Prior service cost/(credit) 24 (20)

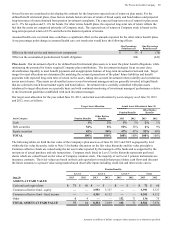

Assumptions.We determine our actuarial assumptions on an annual basis. These assumptions are weighted to reflect each

country that may have an impact on the cost of providing retirement benefits. The weighted average assumptions for the

defined benefit and other retiree benefit calculations, as well as assumed health care trend rates, were as follows:

Pension Benefits Other Retiree Benefits

Years ended June 30 2013 2012 2013 2012

ASSUMPTIONS USED TO DETERMINE BENEFIT OBLIGATIONS(1)

Discount rate 4.0% 4.2% 4.8% 4.3%

Rate of compensation increase 3.2% 3.3% —% —%

ASSUMPTIONS USED TO DETERMINE NET PERIODIC BENEFIT COST(2)

Discount rate 4.2% 5.3% 4.3% 5.7%

Expected return on plan assets 7.3% 7.4% 8.3% 9.2%

Rate of compensation increase 3.3% 3.5% —% —%

ASSUMED HEALTH CARE COST TREND RATES

Health care cost trend rates assumed for next year —% —% 7.3% 8.0%

Rate to which the health care cost trend rate is assumed to decline (ultimate trend rate) —% —% 5.0% 5.0%

Year that the rate reaches the ultimate trend rate —% —% 2020 2019

(1) Determined as of end of year.

(2) Determined as of beginning of year and adjusted for acquisitions.