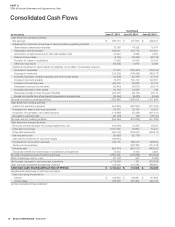

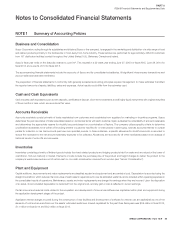

Sysco 2015 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2015 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

SYSCO CORPORATION-Form10-K 39

PARTII

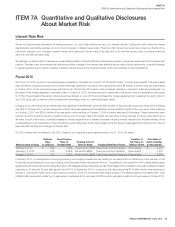

ITEM 7AQuantitative and Qualitative Disclosures About Market Risk

ITEM 7A Quantitative and Qualitative Disclosures

About Market Risk

Interest Rate Risk

We do not utilize nancial instruments for trading purposes. Our use of debt directly exposes us to interest rate risk. Floating rate debt, where the interest

rate uctuates periodically, exposes us to short-term changes in market interest rates. Fixed rate debt, where the interest rate is xed over the life of the

instrument, exposes us to changes in market interest rates re ected in the fair value of the debt and to the risk that we may need to re nance maturing

debt with new debt at higher rates.

We manage our debt portfolio to achieve an overall desired position of xed and oating rates and may employ interest rate swaps as a tool to achieve that

position. The major risks from interest rate derivatives include changes in the interest rates affecting the fair value of such instruments, potential increases

in interest expense due to market increases in oating interest rates and the creditworthiness of the counterparties in such transactions.

Fiscal 2015

As of June 27, 2015, we had no commercial paper outstanding. Total debt as of June 27, 2015 was $7.3 billion, of which approximately 74% was at xed

rates of interest, including the impact of our interest rate swap agreement. Included in the total debt amount is $5.0 billion in senior notes that were issued

in October 2014, for the proposed merger with US Foods. The October 2014 senior notes contained mandatory redemption features providing that, on

the earlier of the merger agreement termination date or October 8, 2015, we were required to redeem all of the senior notes at a redemption price equal

to 101% of the principal of the senior notes plus accrued interest. In June 2015, we terminated the merger agreement and redeemed the senior notes in

July 2015 using cash on hand and the proceeds from borrowings under our commercial paper facility.

In August 2013, we entered into an interest rate swap agreement that effectively converted $500.0 million of xed rate debt maturing in scal 2018 to oating

rate debt. In October 2014, we also entered into interest rate swap agreements that effectively converted $500.0 million of the new senior notes maturing

on October 2, 2017 and $750.0 million of the new senior notes maturing on October 2, 2019 to oating rate debt (2014 swaps). These transactions were

entered into with the goal of reducing overall borrowing cost. The major risks from interest rate derivatives include changes in interest rates affecting the

fair value of such instruments, potential increases in interest expense due to market increases in oating interest rates and the creditworthiness of the

counterparties in such transactions. These transactions were designated as fair value hedges since the swaps hedge against the change in fair value of

xed rate debt resulting from changes in interest rates.

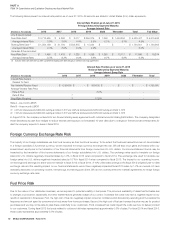

Our 2014 swaps were terminated in July 2015. Details of our outstanding swap agreements at June 27, 2015, are below:

Maturity Date of Swap

Notional

Value

(in millions)

Fixed Coupon

Rate on

Hedged Debt

Floating Interest

Rateon Swap Floating Rate Reset Terms

Location of

FairValue on

Balance Sheet

Fair Value of

Asset (Liability)

(in thousands)

October 2, 2017 $ 500 1.45% Three-month LIBOR Every three months in arrears Other assets $ 2,419

February 12, 2018 500 5.25% Six-month LIBOR Every six months in advance Other assets 4,275

October 2, 2019 750 2.35% Three-month LIBOR Every three months in advance Other assets 5,903

In January 2014, in contemplation of securing nancing and hedging interest rate risk relating to our assumption or re nancing of the net debt of US

Foods that was scheduled to occur upon closing of the proposed merger (discussed in Note 4, “Acquisitions”), we entered into two forward starting swap

agreements with notional amounts totaling $2.0 billion. We designated these derivatives as cash ow hedges of the variability in the cash out ows of interest

payments on 10-year and 30-year debt issued in scal 2015. In September 2014, in conjunction with the pricing of the $1.25 billion senior notes maturing on

October 2, 2024 and $1 billion senior notes maturing October 2, 2044, we terminated these swaps, locking in the effective yields on the related debt. Cash

of $58.9 million was paid to settle the 10-year swap in September 2014, and cash of $129.9 million was paid to settle the 30-year swap in October 2014.