Sysco 2015 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2015 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

SYSCO CORPORATION-Form10-K 67

PARTII

ITEM 8Financial Statements and Supplementary Data

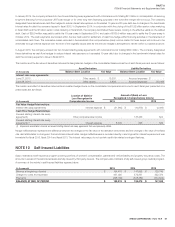

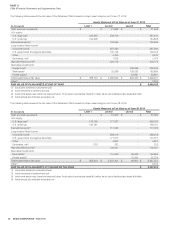

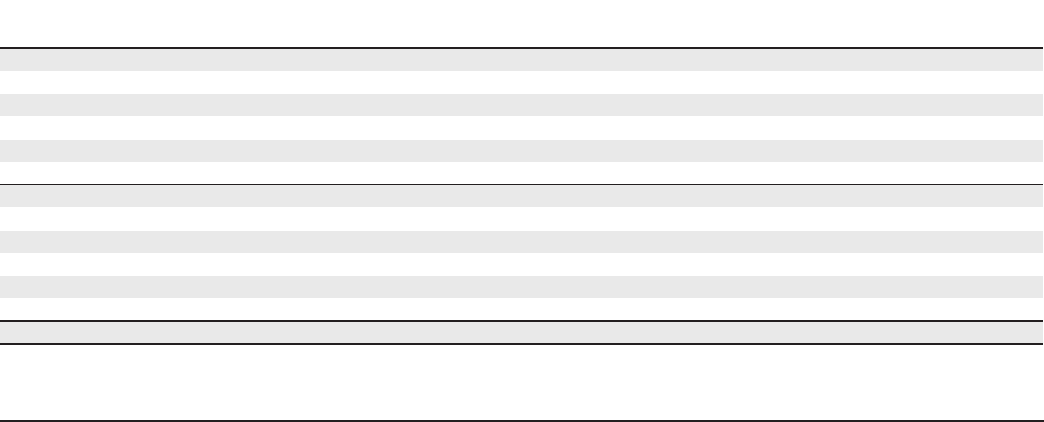

The following table sets forth a summary of changes in the fair value of the Retirement Plan’s Level 3 assets for each scal year:

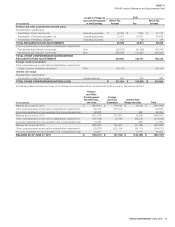

(Inthousands)

Real Estate

Funds

Private Equity

Funds Hedge Funds

Total Level3

Measurements

Balance, June 29, 2013 $ 64,845 $ 14,375 $ - $ 79,220

Actual return on plan assets:

Relating to assets still held at the reporting date 3,044 1,931 - 4,975

Relating to assets sold during the period 3,307 1,767 - 5,074

Purchases and sales, net (35,793) 13,131 - (22,662)

Transfers in and/or out of Level 3 - - - -

Balance, June 28, 2014 $ 35,403 $ 31,204 $ - $ 66,607

Actual return on plan assets:

Relating to assets still held at the reporting date 8,122 2,438 12,265 22,825

Relating to assets sold during the period 1,062 1,780 - 2,842

Purchases and sales, net 93,696 17,469 323,000 434,165

Transfers in and/or out of Level 3 - - - -

BALANCE, JUNE 27, 2015 $ 138,283 $ 52,891 $ 335,265 $ 526,439

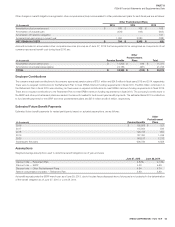

NOTE15 Multiemployer Employee Bene t Plans

De ned Bene t Pension Plans

Sysco contributes to several multiemployer de ned bene t pension plans in the U.S. and Canada based on obligations arising under collective bargaining

agreements covering union-represented employees. Sysco does not directly manage these multiemployer plans, which are generally managed by boards of

trustees, half of whom are appointed by the unions and the other half appointed by Sysco and the other employers contributing to the plan. Approximately 10%

of Sysco’s current employees are participants in such multiemployer plans as of June 27, 2015.

The risks of participating in these multiemployer plans are different from single-employer plans in the following aspects:

•Assets contributed to the multiemployer plan by one employer may be used to provide bene ts to employees of other participating employers.

•If a participating employer stops contributing to the plan, the unfunded obligations of the plan may be borne by the remaining participating employers.

•

If Sysco chooses to stop participating in some of its multiemployer plans, Sysco may be required to pay those plans an amount based on the underfunded

status of the plan, referred to as a withdrawal liability.

Based upon the information available from plan administrators, management believes that several of these multiemployer plans are underfunded. In addition,

pension-related legislation in the U.S. requires underfunded pension plans to improve their funding ratios within prescribed intervals based on the level of

their underfunding. As a result, Sysco expects its contributions to these plans to increase in the future. In addition, if a U.S. multiemployer de ned bene t

plan fails to satisfy certain minimum funding requirements, the Internal Revenue Service (IRS) may impose a nondeductible excise tax of 5% on the amount

of the accumulated funding de ciency for those employers contributing to the fund.

Withdrawal Activity

Sysco has voluntarily withdrawn from various multiemployer pension plans. There were no withdrawal liability provisions recorded in scal 2015, $1.5million

in scal 2014 and $41.9 million in scal 2013. As of June 27, 2015, Sysco had no liabilities recorded related to certain multiemployer de ned bene t

plans for which Sysco’s voluntary withdrawal had already occurred and had $1.4 million liabilities as of June 28, 2014. Recorded withdrawal liabilities are

estimated at the time of withdrawal based on the most recently available valuation and participant data for the respective plans; amounts are subsequently

adjusted to the period of payment to re ect any changes to these estimates. If any of these plans were to undergo a mass withdrawal, as de ned by the

Pension Bene t Guaranty Corporation, within the two plan years following the plan year in which we completely withdraw from that plan, Sysco could have

additional liability. The company does not currently believe any mass withdrawals are probable to occur in the applicable two-plan year time frame relating

to the plans from which Sysco has voluntarily withdrawn.

Potential Withdrawal Liability

Under current law regarding multiemployer de ned bene t plans, a plan’s termination, Sysco’s voluntary withdrawal, or the mass withdrawal of all contributing

employers from any underfunded multiemployer de ned bene t plan would require Sysco to make payments to the plan for Sysco’s proportionate share

of the multiemployer plan’s unfunded vested liabilities. Generally, Sysco does not have the greatest share of liability among the participants in any of the

plans in which it participates. Sysco believes that one of the above-mentioned events is reasonably possible for certain plans in which it participates and