Sysco 2015 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2015 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

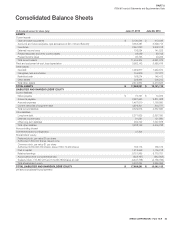

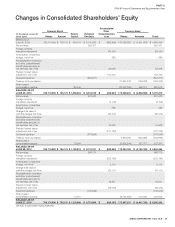

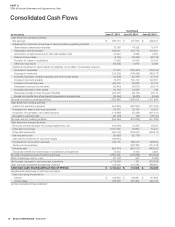

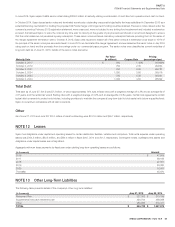

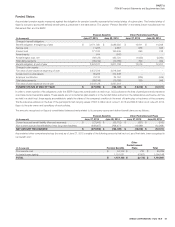

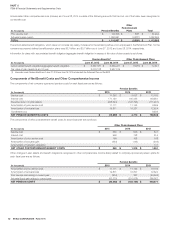

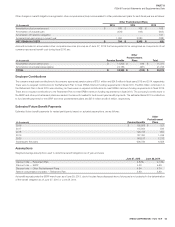

SYSCO CORPORATION-Form10-K 53

PARTII

ITEM8Financial Statements and Supplementary Data

NOTE3 New Accounting Standards

Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity

In April 2014, the FASB issued ASU 2014-08, “Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity.” This update

amends ASC 205, “Presentation of Financial Statements,” and ASC 360, “Property, Plant, and Equipment,” primarily to change the criteria for when a

disposal is required to be reported as a discontinued operation. A disposal of a component of an entity or a group of components of an entity is required

to be reported in discontinued operations if the disposal represents a strategic shift that has or will have a major effect on the entity’s operations or nancial

results. The amendments in this update specify presentation and disclosure requirements for discontinued operations as well as disclosure requirements

for other disposals that do not qualify as discontinued operations. The amendments in this update are effective for all disposals or classi cations as held

for sale, including upon acquisition, of a component of an entity that occur within annual periods beginning on or after December 15, 2014 and interim

periods within those years, which is scal 2016 for Sysco. Early adoption is permitted. Sysco will implement on any related transactions, prospectively.

Revenue from Contracts with Customers

In May 2014, the FASB issued ASU 2014-09, “Revenue from Contracts with Customers.” This update creates ASC 606, “Revenue from Contracts with

Customers,” and supersedes the revenue recognition requirements in ASC 605, “Revenue Recognition.” Additionally, other sections of the ASC were

amended to be consistent with the guidance in this update. The core principle of ASC 606 is that an entity should recognize revenue to depict the transfer

of promised goods or services to customers in an amount that re ects the consideration to which the entity expects to be entitled in exchange for those

goods and services. A ve-step revenue recognition model is to be applied to achieve this core principle. ASC 606 also speci es comprehensive disclosures

to help users of nancial statements understand the nature, amount, timing and uncertainty of revenue that is recognized. The amendments in this update

are effective for annual periods beginning after December 15, 2017, including interim periods within that reporting period, which is scal 2019 for Sysco.

Early adoption is not permitted. Sysco is currently evaluating the impact this update will have on its nancial statements.

Disclosure of Uncertainties About an Entity’s Ability to Continue as a Going Concern

In August 2014, the FASB issued ASU No. 2014-15, “Disclosure of Uncertainties About an Entity’s Ability to Continue as a Going Concern.” This ASU

provides guidance on determining when and how to disclose going-concern uncertainties in the nancial statements. The new standard requires management

to perform interim and annual assessments of an entity’s ability to continue as a going concern within one year of the date the nancial statements are

issued. An entity must provide certain disclosures if conditions or events raise substantial doubt about the entity’s ability to continue as a going concern.

This guidance is effective for scal years—and interim periods within those scal years—beginning after December 15, 2016, with early adoption permitted.

The Company is currently reviewing the provisions of the new standard and whether it will early adopt.

NOTE4 Acquisitions

During scal 2015, in the aggregate, the company paid cash of $115.9 million, net of cash acquired, for acquisitions made during scal 2015 and for

contingent consideration related to acquisitions made in previous scal years. During scal 2015, Sysco acquired for cash a broadline company in Ontario,

Canada; a joint venture interest in a foodservice distribution company in Mexico; a joint venture interest in a foodservice distribution company in Costa

Rica and a specialty seafood company in New Jersey. The scal 2015 acquisitions were immaterial, individually and in the aggregate, to the consolidated

nancial statements.

Certain acquisitions involve contingent consideration that may include earnout agreements that are typically payable over periods of up to three years only

in the event that certain operating results are attained. As of June 27, 2015, aggregate contingent consideration amounts outstanding relating to completed

acquisitions were $39.0 million, of which $29.4 million was recorded as earnout liabilities as of June 27, 2015.

In the second quarter of scal 2014, the company announced an agreement to merge with US Foods, Inc. (US Foods). In February 2015, following

completion of its regulatory review of the proposed merger, the US Federal Trade Commission (FTC) led a motion with the U.S. District Court for the

District of Columbia (the Court) seeking a preliminary injunction to prevent the parties from closing the merger, which the Court granted on June 23, 2015.

On June 26, 2015, the parties terminated the merger agreement, as a result of which Sysco was obligated to pay $300 million to the owners of US Foods.

During the review period with the FTC, Sysco created a divestiture package, comprised of the sale of 11 US Foods facilities to Performance Food Group

(PFG), which was contingent on the closing of the merger. This divestiture agreement entitled PFG to receive a $25 million termination fee if the sale of the

divestiture package was terminated before July 6, 2015, with each of Sysco and US Foods responsible for one half of the applicable fee. Sysco accrued

for termination payments totaling $312.5 million in scal 2015 and paid these amounts in scal 2016.