Sysco 2015 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2015 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

SYSCO CORPORATION-Form10-K52

PARTII

ITEM8Financial Statements and Supplementary Data

The determination of the company’s provision for income taxes requires signi cant judgment, the use of estimates and the interpretation and application

of complex tax laws. The company’s provision for income taxes primarily re ects a combination of income earned and taxed in the various U.S. federal

and state, as well as various foreign jurisdictions. Jurisdictional tax law changes, increases or decreases in permanent differences between book and tax

items, accruals or adjustments of accruals for tax contingencies or valuation allowances, and the company’s change in the mix of earnings from these

taxing jurisdictions all affect the overall effective tax rate.

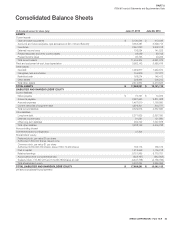

Acquisitions

Acquisitions of businesses are accounted for using the acquisition method of accounting, and the nancial statements include the results of the acquired

operations from the respective dates of acquisition.

The purchase price of the acquired entities is allocated to the net assets acquired and liabilities assumed based on the estimated fair value at the dates of

acquisition, with any excess of cost over the fair value of net assets acquired, including intangibles, recognized as goodwill. The balances included in the

consolidated balance sheets related to recent acquisitions are based upon preliminary information and are subject to change when nal asset and liability

valuations are obtained. Subsequent changes to the preliminary balances are re ected retrospectively, if material. Material changes to the preliminary

allocations are not anticipated by management.

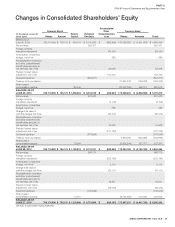

Noncontrolling interest

In scal 2015, Sysco acquired a 50% interest in a foodservice company in Costa Rica. It was determined that consolidation of the entity was appropriate

and, therefore, the nancial position, results of operations and cash ows for this company have been included in Sysco’s nancial statements. The value

of the 50% noncontrolling interest is considered redeemable due to certain features of the investment agreement and has been presented as mezzanine

equity, which is outside of permanent equity, in the consolidated balance sheets. The income attributable to the noncontrolling interest is located within

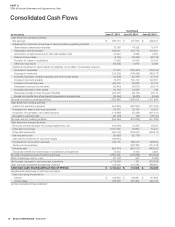

other expense (income), net in the consolidated results of operations, as this amount is not material. The non-cash add back for the change in the value

of the noncontrolling interest is located within Other non-cash items on the consolidated cash ows.

NOTE2 Changes in Accounting

Presentation of an Unrecognized Tax Bene t When a Net Operating Loss Carryforward, a Similar

Tax Loss, or a Tax Credit Carryforward Exists

In July 2013, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2013-11, “Presentation of an Unrecognized Tax

Bene t When a Net Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists.” This update amends ASC 740, “Income Taxes,”

to require that in certain cases, an unrecognized tax bene t, or portion of an unrecognized tax bene t, should be presented in the nancial statements as

a reduction to a deferred tax asset for a net operating loss carryforward, a similar tax loss, or a tax credit carryforward when such items exist in the same

taxing jurisdiction. The amendments in this update are effective for scal years, and interim periods within those years, beginning after December15, 2013,

which was scal 2015 for Sysco. The company’s adoption of this guidance did not have a material impact on the company’s balance sheets, results of

operations or cash ows.

Simplifying the Presentation of Debt Issuance Costs

In April 2015, the FASB issued ASU 2015-03, Interest - Imputation of Interest (Subtopic 835-30): Simplifying the Presentation of Debt Issuance Costs.

The update requires debt issuance costs related to a recognized debt liability be presented in the balance sheet as a direct deduction from the carrying

amount of the related debt liability, instead of being presented as an asset. Debt disclosures will include the face amount of the debt liability and the effective

interest rate. The update requires retrospective application and represents a change in accounting principle. We adopted this standard for the scal year

ended June 27, 2015. Although the new guidance had no impact on the company’s results of operations, the debt issuance costs presented as assets

within the company’s consolidated balance sheet as of June 28, 2014, of $26.8 million has been reclassi ed as reductions of the related debt liability as

a result of early adoption.

Practical Expedient for the Measurement Date of an Employer’s De ned Bene t Obligation

and Plan Assets

In April 2015, the FASB issued ASU 2015-04, “Compensation-Retirement Bene ts (Topic 715), Practical Expedient for the Measurement Date of an

Employer’s De ned Bene t Obligation and Plan Assets.” The amendments in this ASU provide a practical expedient for employers with scal year-ends

that do not fall on a month-end by permitting those employers to measure de ned bene t plan assets and obligations as of the month-end that is closest

to the entity’s scal year-end. Sysco early adopted this standard in scal 2015 using a June 30

th

measurement date as a practical expedient. The adoption

did not have a material impact on the nancial position of Sysco.