GE 2010 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2010 GE annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

100 GE 2010 ANNUAL REPORT

Plan fiduciaries set investment policies and strategies for the trust

and oversee its investment allocation, which includes selecting

investment managers and setting long-term strategic targets. The

primary long-term strategic investment objective is balancing

investment risk and return. Target allocation percentages are

established at an asset class level by plan fiduciaries. Target alloca-

tion ranges are guidelines, not limitations, and occasionally plan

fiduciaries will approve allocations above or below a target range.

Trust assets invested in short-term securities must generally

be invested in securities rated A1/P1 or better, except for 15% of

such securities that may be rated A2/P2 and other short-term

securities as may be approved by the plan fiduciaries. According

to statute, the aggregate holdings of all qualifying employer

securities (e.g., GE common stock) and qualifying employer real

property may not exceed 10% of the fair value of trust assets at

the time of purchase. GE securities represented 4.5% and 3.7%

of trust assets at year-end 2010 and 2009, respectively.

Retiree life plan assets were $1,125 million and $1,138 million

at December 31, 2010 and 2009, respectively. Equity and debt

securities amounting to $942 million and $959 million represented

approximately 78% and 80% of total investments at December 31,

2010 and 2009, respectively. The plans’ investments were classi-

fied as 39% Level 1, 39% Level 2 and 22% Level 3 at December 31,

2010. The plans’ investments were classified as 42% Level 1,

37% Level 2 and 21% Level 3 at December 31, 2009. The changes

in Level 3 investments were insignificant for the years ended

December 31, 2010 and 2009.

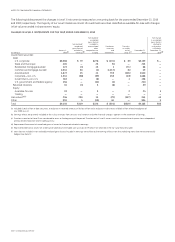

RETIREE BENEFIT ASSET (LIABILITY)

December 31 (In millions) 2010 2009

Funded status

(a)

$(10,885) $(11,637)

Liability recorded in the Statement

of Financial Position

Retiree health plans

Due within one year $ (644) $ (691)

Due after one year (8,922) (9,790)

Retiree life plans (1,319) (1,156)

Net liability recognized $(10,885) $(11,637)

Amounts recorded in shareowners’

equity (unamortized)

Prior service cost $ 3,523 $ 4,154

Net actuarial loss (gain) (671) 272

Total $ 2,852 $ 4,426

(a) Fair value of assets less APBO, as shown in the preceding tables.

In 2011, we estimate that we will amortize $630 million of prior

service cost and $110 million of net actuarial gain from shareown-

ers’ equity into retiree benefit plans cost. Comparable amortized

amounts in 2010 were $631 million of prior service cost and

$22 million of net actuarial gains.

ESTIMATED FUTURE BENEFIT PAYMENTS

2016 –

(In millions) 2011 2012 2013 2014 2015 2020

Gross $845 $840 $840 $840 $845 $4,255

Expected Medicare

Part D subsidy 5 5 5 5 5 20

Net $840 $835 $835 $835 $840 $4,235

Changes in the accumulated postretirement benefit obligation

for retiree benefit plans follow.

ACCUMULATED POSTRETIREMENT BENEFIT OBLIGATION (APBO)

(In millions) 2010 2009

Balance at January 1 $12,775 $11,949

Service cost for benefits earned 241 442

Interest cost on benefit obligations 699 709

Participant contributions 55 50

Plan amendments — (37)

Actuarial loss (gain)

(a)(b) (942) 504

Benefits paid

(c) (818) (842)

Balance at December 31

(d) $12,010 $12,775

(a) For 2010, included the effects of healthcare reform provisions on our Medicare-

approved prescription drug plan.

(b) For 2009, included a $152 million reduction in APBO as a result of our agreement

with Comcast Corporation to transfer the NBCU business to a newly formed entity

in which we will own a 49% interest.

(c) Net of Medicare Part D subsidy of $72 million and $83 million in 2010 and 2009,

respectively.

(d) The APBO for the retiree health plans was $9,566 million and $10,481 million at

year-end 2010 and 2009, respectively.

A one percentage point change in the assumed healthcare cost

trend rate would have the following effects.

(In millions) 1% increase 1% decrease

APBO at December 31, 2010 $1,012 $(858)

Service and interest costs in 2010 91 (76)

PLAN ASSETS

The fair value of the classes of retiree benefit plans’ investments

is presented below. The inputs and valuation techniques used to

measure the fair value of assets are consistently applied and

described in Note 1.

FAIR VALUE OF PLAN ASSETS

(In millions) 2010 2009

Balance at January 1 $1,138 $1,175

Actual gain on plan assets 139 111

Employer contributions 611 644

Participant contributions 55 50

Benefits paid

(a) (818) (842)

Balance at December 31 $1,125 $1,138

(a) Net of Medicare Part D subsidy.

ASSET ALLOCATION

2010 2010

Target Actual

December 31 allocation allocation

Equity securities 37–77 % (a) 44

Debt securities (including cash equivalents) 11–41 34

Private equities 3–13 13

Real estate 2–12 5

Other 0–10 4

(a) Target allocations were 19–39% for U.S. equity securities and 18–38% for non-U.S.

equity securities.

(b) Actual allocations were 25% for U.S. equity securities and 19% for non-U.S.

equity securities.

% (b)