GE 2010 Annual Report Download - page 119

Download and view the complete annual report

Please find page 119 of the 2010 GE annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

GE 2010 ANNUAL REPORT 117

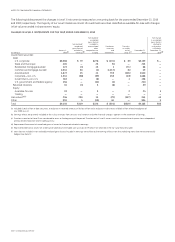

NONACCRUAL FINANCING RECEIVABLES

The following table provides further information about Commercial financing receivables that are classified as nonaccrual. Of our

$5,463 million of nonaccrual financing receivables at December 31, 2010, $1,016 million are currently paying in accordance with their

contractual terms.

COMMERCIAL (a)

Nonaccrual financing receivables at Nonearning financing receivables at

December 31, January 1, December 31, December 31, January 1, December 31,

(Dollars in millions) 2010 2010

(b) 2009 2010 2010 (b) 2009

CLL

Americas $3,206 $3,776 $3,484 $2,571 $3,437 $3,155

Europe 1,415 1,441 1,441 1,241 1,441 1,441

Asia 616 559 576 406 559 576

Other 9 24 24 8 24 24

Total CLL 5,246 5,800 5,525 4,226 5,461 5,196

Energy Financial Services 78 183 183 62 78 78

GECAS — 153 153 — 153 153

Other 139 95 95 102 72 72

Total $5,463 $6,231 $5,956 $4,390 $5,764 $5,499

Allowance for losses percentage 37.4% 35.8% 36.5% 46.6% 38.7% 39.6%

(a) During the first quarter of 2010, we transferred the Consumer business in Italy from Consumer to CLL. Prior period amounts were reclassified to conform to the current-

period presentation.

(b) Reflects the effects of our adoption of ASU 2009-16 & 17 on January 1, 2010.

IMPAIRED LOANS

The following table provides information about loans classified as impaired and specific reserves related to Commercial.

COMMERCIAL (a)

With no specific allowance With a specific allowance

Recorded Unpaid Average Recorded Unpaid Average

investment principal investment in investment principal Associated investment in

December 31, 2010 (In millions) in loans balance loans in loans balance allowance loans

CLL

Americas $2,030 $2,127 $1,547 $1,699 $1,744 $ 589 $1,754

Europe 802 674 629 566 566 267 563

Asia 119 117 117 338 303 132 334

Other — — 9 — — — —

Total CLL 2,951 2,918 2,302 2,603 2,613 988 2,651

Energy Financial Services 54 61 76 24 24 6 70

GECAS 24 24 50 — — — 31

Other 58 57 30 106 99 37 82

Total $3,087 $3,060 $2,458 $2,733 $2,736 $1,031 $2,834

(a) We recognized $88 million of interest income for the year ended December 31, 2010, principally on a cash basis. A substantial majority of this amount was related to income

recognized in our CLL—Americas business.

CREDIT QUALITY INDICATORS

Substantially all of our Commercial financing receivables portfolio

is secured lending and we assess the overall quality of the port-

folio based on the potential risk of loss measure. The metric

incorporates both the borrower’s credit quality along with any

related collateral protection.

Our internal risk ratings process is an important source of

information in determining our allowance for losses and repre-

sents a comprehensive, statistically validated approach to

evaluate risk in our financing receivables portfolios. In deriving

our internal risk ratings, we stratify our Commercial portfolios

into twenty-one categories of default risk and/or six categories of

loss given default to group into three categories: A, B and C. Our

process starts by developing an internal risk rating for our

borrowers, which is based upon our proprietary models using

data derived from borrower financial statements, agency ratings,

payment history information, equity prices and other commercial

borrower characteristics. We then evaluate the potential risk of

loss for the specific lending transaction in the event of borrower

default, which takes into account such factors as applicable

collateral value, historical loss and recovery rates for similar

transactions, and our collection capabilities. Our internal risk

ratings process and the models we use are subject to regular

monitoring and validation controls. The frequency of rating

updates is set by our credit risk policy, which requires annual

Audit Committee approval. The models are updated on a regular

basis and statistically validated annually, or more frequently as

circumstances warrant.