GE 2010 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2010 GE annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

GE 2010 ANNUAL REPORT 113

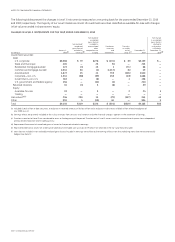

The following table provides information about the fair value

of our derivatives, by contract type, separating those accounted

for as hedges and those that are not.

2010 2009

Fair value Fair value

December 31 (In millions) Assets Liabilities Assets Liabilities

DERIVATIVES ACCOUNTED

FOR AS HEDGES

Interest rate contracts $ 5,959 $ 2,675 $ 4,477 $ 3,469

Currency exchange

contracts 2,965 2,533 4,273 2,361

Other contracts 5 — 16 4

8,929 5,208 8,766 5,834

DERIVATIVES NOT ACCOUNTED

FOR AS HEDGES

Interest rate contracts 294 552 974 892

Currency exchange

contracts 1,602 846 1,639 658

Other contracts 531 50 478 136

2,427 1,448 3,091 1,686

NETTING ADJUSTMENTS (a) (3,867) (3,857) (3,851) (3,860)

Total $ 7,489 $ 2,799 $ 8,006 $ 3,660

Derivatives are classified in the captions “All other assets” and “All other liabilities” in

our financial statements.

(a) The netting of derivative receivables and payables is permitted when a legally

enforceable master netting agreement exists. Amounts included fair value

adjustments related to our own and counterparty non-performance risk. At

December 31, 2010 and 2009, the cumulative adjustment for non-performance

risk was a loss of $10 million and a gain of $9 million, respectively.

FAIR VALUE HEDGES

We use interest rate and currency exchange derivatives to hedge

the fair value effects of interest rate and currency exchange rate

changes on local and non-functional currency denominated

fixed-rate debt. For relationships designated as fair value hedges,

changes in fair value of the derivatives are recorded in earnings

within interest and other financial charges, along with offsetting

adjustments to the carrying amount of the hedged debt. The

following table provides information about the earnings effects

of our fair value hedging relationships for the years ended

December 31, 2010 and 2009.

2010

2009

Gain (loss) Gain (loss) Gain (loss) Gain (loss)

Year ended on hedging on hedged on hedging on hedged

December 31 (In millions) derivatives items derivatives items

Interest rate contracts $2,387 $(2,924) $(5,194) $4,998

Currency exchange

contracts 47 (60) (1,106) 1,093

Fair value hedges resulted in $(550) million and $(209) million of ineffectiveness in

2010 and 2009, respectively. In 2010 and 2009, there were insignificant amounts and

$(225) million excluded from the assessment of effectiveness, respectively.

CASH FLOW HEDGES

We use interest rate, currency exchange and commodity deriva-

tives to reduce the variability of expected future cash flows

associated with variable rate borrowings and commercial pur-

chase and sale transactions, including commodities. For

derivatives that are designated in a cash flow hedging relation-

ship, the effective portion of the change in fair value of the

derivative is reported as a component of AOCI and reclassified

LOAN COMMITMENTS

Notional amount

December 31 (In millions) 2010 2009

Ordinary course of business

lending commitments

(a)(b) $ 4,507 $ 6,676

Unused revolving credit lines

(c)

Commercial

(d) 23,779 31,760

Consumer—principally credit cards 227,006 229,386

(a) Excluded investment commitments of $1,990 million and $2,659 million as of

December 31, 2010 and 2009, respectively.

(b) Included a $972 million commitment as of December 31, 2009, associated with

a secured financing arrangement that could have increased to a maximum of

$4,998 million based on the asset volume under the arrangement. This

commitment was terminated during the third quarter of 2010.

(c) Excluded inventory financing arrangements, which may be withdrawn at our

option, of $11,840 million and $13,889 million as of December 31, 2010 and

2009, respectively.

(d) Included commitments of $16,243 million and $17,643 million as of December 31,

2010 and 2009, respectively, associated with secured financing arrangements that

could have increased to a maximum of $20,268 million and $23,992 million at

December 31, 2010 and 2009, respectively, based on asset volume under the

arrangement.

Derivatives and hedging

As a matter of policy, we use derivatives for risk management

purposes, and we do not use derivatives for speculative purposes.

A key risk management objective for our financial services busi-

nesses is to mitigate interest rate and currency risk by seeking to

ensure that the characteristics of the debt match the assets they

are funding. If the form (fixed versus floating) and currency

denomination of the debt we issue do not match the related

assets, we typically execute derivatives to adjust the nature and

tenor of funding to meet this objective. The determination of

whether we enter into a derivative transaction or issue debt

directly to achieve this objective depends on a number of

factors, including market related factors that affect the type

of debt we can issue.

The notional amounts of derivative contracts represent the

basis upon which interest and other payments are calculated and

are reported gross, except for offsetting foreign currency forward

contracts that are executed in order to manage our currency risk

of net investment in foreign subsidiaries. Of the outstanding

notional amount of $347,000 million, approximately 86% or

$300,000 million, is associated with reducing or eliminating the

interest rate, currency or market risk between financial assets

and liabilities in our financial services businesses. The remaining

derivative activities primarily relate to hedging against adverse

changes in currency exchange rates and commodity prices

related to anticipated sales and purchases and contracts contain-

ing certain clauses which meet the accounting definition of a

derivative. The instruments used in these activities are desig-

nated as hedges when practicable. When we are not able to apply

hedge accounting, or when the derivative and the hedged item

are both recorded in earnings currently, the derivatives are

deemed economic hedges and hedge accounting is not applied.

This most frequently occurs when we hedge a recognized foreign

currency transaction (e.g., a receivable or payable) with a deriva-

tive. Since the effects of changes in exchange rates are reflected

currently in earnings for both the derivative and the transaction,

the economic hedge does not require hedge accounting.