Humana 2002 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2002 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

CMS regulations require submission of quarterly and annual financial statements. In addition, CMS requires

certain disclosures to CMS and to Medicare+Choice beneficiaries concerning operations of a health plan

contracted under the Medicare+Choice program. CMS’s rules require disclosure to members upon request of

information concerning financial arrangements and incentive plans between an HMO and physicians in the

HMOs’ networks. These rules also require certain levels of stop-loss coverage to protect contracted physicians

against major losses relating to patient care, depending on the amount of financial risk they assume. The

reporting of certain health care data contained in HEDIS is another important CMS disclosure requirement.

Our Medicaid products are regulated by the applicable state agency in the state in which we sell a Medicaid

product and by the Health Insurance Administration in Puerto Rico, in conformance with federal approval of the

applicable state plan, and are subject to periodic reviews by these agencies. The reviews are similar in nature to

those performed by CMS.

Laws in each of the states and the Commonwealth of Puerto Rico in which we operate our HMOs, PPOs and

other health insurance-related services regulate our operations, including the scope of benefits, rate formulas,

delivery systems, utilization review procedures, quality assurance, complaint systems, enrollment requirements,

claim payments, marketing and advertising. The HMO, PPO and other health insurance-related products we offer

are sold under licenses issued by the applicable insurance regulators. Under state laws, our HMOs and health

insurance companies are audited by state departments of insurance for financial and contractual compliance, and

our HMOs are audited for compliance with health services standards by respective state departments of health.

Most states’ laws require such audits to be performed at least once every three years.

Our licensed subsidiaries are subject to regulation under state insurance holding company and

Commonwealth of Puerto Rico regulations. These regulations generally require, among other things, prior

approval and/or notice of new products, rates, benefit changes, and certain material transactions, including

dividend payments, purchases or sales of assets, intercompany agreements and the filing of various financial and

operational reports.

Certain of our subsidiaries operate in states that regulate the payment of dividends, loans or other cash

transfers to Humana Inc., our parent company, require minimum levels of equity, and limit investments to

approved securities. The amount of dividends that may be paid to Humana Inc. by these subsidiaries, without

prior approval by state regulatory authorities, is limited based on the entity’s level of statutory income and

statutory capital and surplus. In most states, prior notification is provided before paying a dividend even if

approval is not required.

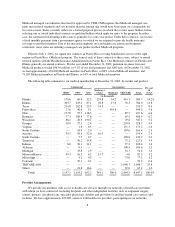

As of December 31, 2002, we maintained aggregate statutory capital and surplus of $1,006.9 million in our

state regulated health insurance subsidiaries. Each of these subsidiaries was in compliance with applicable

statutory requirements which aggregated $576.0 million. Although the minimum required levels of equity are

largely based on premium volume, product mix, and the quality of assets held, minimum requirements can vary

significantly at the state level. Certain states rely on risk-based capital requirements, or RBC, to define the

required levels of equity. RBC is a model developed by the National Association of Insurance Commissioners to

monitor an entity’s solvency. This calculation indicates recommended minimum levels of required capital and

surplus and signals regulatory measures should actual surplus fall below these recommended levels. Some states

are in the process of phasing in these RBC requirements over a number of years. If RBC were fully implemented

by all states at December 31, 2002, each of our subsidiaries would be in compliance, and we would have

$358.8 million of aggregate capital and surplus above the minimum level required under RBC.

One TRICARE subsidiary under the Regions 3 and 4 contract with the Department of Defense is required to

maintain current assets at least equivalent to its current liabilities. We were in compliance with this requirement

at December 31, 2002.

Our management works proactively to ensure compliance with all governmental laws and regulations

affecting our business.

14