Humana 2002 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2002 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

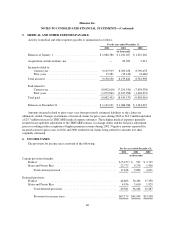

Humana Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

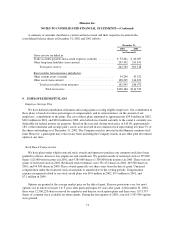

Credit Agreements

We maintain two unsecured revolving credit agreements consisting of a $265 million, 4-year revolving

credit agreement and a $265 million, 364-day revolving credit agreement with a one-year term out option. A one

year term out option converts the outstanding borrowings, if any, under the credit agreement to a one year term

loan upon expiration. The 4-year revolving credit agreement expires in October 2005. In October 2002, we

renewed the 364-day revolving credit agreement which expires in October 2003, unless extended.

There were no balances outstanding under either agreement at December 31, 2002. Under these agreements,

at our option, we can borrow on either a competitive advance basis or a revolving credit basis. The revolving

credit portion of both agreements bear interest at either a fixed rate or floating rate based on LIBOR plus a

spread. The spread, which varies depending on our credit ratings, ranges from 80 to 125 basis points for our

4-year agreement, and 85 to 137.5 basis points for our 364-day agreement. We also pay an annual facility fee

regardless of utilization. This facility fee, currently 25 basis points, may fluctuate between 15 and 50 basis

points, depending upon our credit ratings. The competitive advance portion of any borrowings under either credit

agreement will bear interest at market rates prevailing at the time of borrowing on either a fixed rate or a floating

rate basis, at our option.

These credit agreements contain customary restrictive and financial covenants as well as customary events

of default, including financial covenants regarding the maintenance of net worth, and minimum interest coverage

and maximum leverage ratios. The terms of each of these credit agreements also include standard provisions

related to conditions of borrowing, including a customary material adverse effect clause which could limit our

ability to borrow. We have not experienced a material adverse effect and we know of no circumstances or events

which would be reasonably likely to result in a material adverse effect. We do not believe the material adverse

effect clause poses a material funding risk to Humana in the future. The minimum net worth requirement was

$1,163.4 million at December 31, 2002 and increases by 50% of consolidated net income each quarter. The

minimum interest coverage ratio is generally calculated by dividing interest expense into earnings before interest

and tax expense, or EBIT. The maximum leverage ratio is generally calculated by dividing debt into earnings

before interest, taxes, depreciation and amortization expense, or EBITDA. EBIT and EBITDA used to calculate

compliance with these financial covenants is based upon four consecutive quarters. The current minimum interest

coverage ratio of 3.5, increases to 4.0 effective December 31, 2003. The current maximum leverage ratio of 2.75

declines to 2.5 effective December 31, 2003. At December 31, 2002, our net worth of $1,606.5 million, interest

coverage ratio of 13.7, and leverage ratio of 1.7 were all in compliance with the applicable requirements.

Additionally, we would have been in compliance assuming the more restrictive future financial covenant

requirements were applicable at December 31, 2002.

Commercial Paper Programs

We maintain indirect access to the commercial paper market through our conduit commercial paper

financing program. Under this program, a third party issues commercial paper and loans the proceeds of those

issuances to us so that the interest and principal payments on the loans match those on the underlying commercial

paper. The $265 million, 364-day revolving credit agreement supports the conduit commercial paper financing

program of up to $265 million. The weighted average interest rate on our conduit commercial paper borrowings

was 1.76% at December 31, 2002. The carrying value of these borrowings approximates fair value as the interest

rate on the borrowings varies at market rates.

We also maintain and may issue short-term debt securities under a commercial paper program when market

conditions allow. The program is backed by our credit agreements described above. Aggregate borrowing under

both the credit agreements and commercial paper program cannot exceed $530 million.

69