Humana 2002 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2002 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

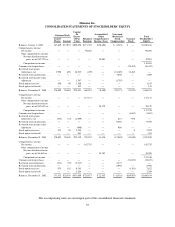

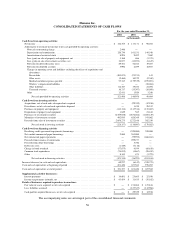

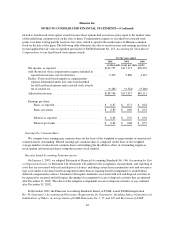

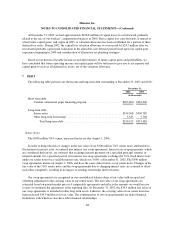

Humana Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Losses are recognized for a long-lived asset to be held and used in our operations when the undiscounted future

cash flows expected to result from the use of the asset is less than its carrying value. We recognize an impairment

loss based on the excess of the carrying value over the fair value of the asset. A long-lived asset held for sale is

reported at the lower of the carrying amount or fair value less costs to sell. Depreciation expense is not

recognized on assets held for sale. Losses are recognized for a long-lived asset to be abandoned when it ceases to

be used. In addition, we periodically review the estimated lives of all long-lived assets for reasonableness. See

Note 14 for a discussion related to our 2002 impairment.

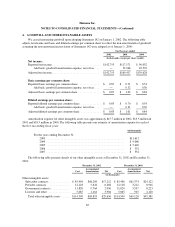

Goodwill and Other Intangible Assets

Goodwill represents the unamortized excess of cost over the fair value of the net tangible and other

intangible assets acquired. Statement of Financial Accounting Standards No. 142, Goodwill and Other Intangible

Assets, or Statement 142, requires goodwill no longer be amortized to earnings, but instead be tested at least

annually for impairment at a level of reporting referred to as the reporting unit and more frequently if adverse

events or changes in circumstances indicate that the asset may be impaired. A reporting unit is one level below

our Commercial and Government segments. The Commercial segment’s two reporting units consist of fully and

self-insured medical and specialty. The Government segment’s three reporting units consist of Medicare+Choice,

TRICARE and Medicaid. Goodwill was assigned to the reporting unit that was expected to benefit from a

specific acquisition. If goodwill was expected to benefit multiple reporting units, we allocated goodwill in

connection with our transitional impairment test as of January 1, 2002 based upon the reporting units’ relative

fair value. This process resulted in the allocation of $633.2 million of goodwill to the Commercial segment and

$143.7 million of goodwill to the Government segment.

We ceased amortizing goodwill upon adopting Statement 142 on January 1, 2002. Statement 142 requires a

two-step process to review goodwill for impairment. The first step is a screen for potential impairment, and the

second step measures the amount of impairment, if any. Impairment tests are performed, at a minimum, in the

fourth quarter of each year supported by our long-range business plan and annual planning process. Impairment

tests completed for 2002 did not result in an impairment loss.

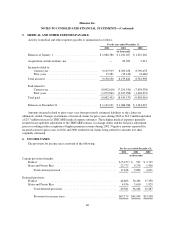

Medical and Other Expenses Payable and Medical Cost Recognition

Medical costs include claim payments, capitation payments, allocations of certain centralized expenses and

various other costs incurred to provide health insurance coverage to members, as well as estimates of future

payments to hospitals and others for medical care provided prior to the balance sheet date. Capitation payments

represent monthly contractual fees disbursed to primary care physicians and other providers who are responsible

for providing medical care to members. We estimate the costs of our future medical claims and other medical

expense payments using actuarial methods and assumptions based upon claim payment patterns, medical cost

inflation, historical developments such as claim inventory levels and claim receipt patterns, and other relevant

factors, and record medical claims reserves for future payments. We continually review estimates of future

payments relating to medical claims costs for services incurred in the current and prior periods and make

necessary adjustments to our reserves.

We reassess the profitability of our contracts for providing health insurance coverage to our members when

current operating results or forecasts indicate probable future losses. We establish a premium deficiency liability

in current operations to the extent that the sum of a geographic market’s expected future medical costs, claim

adjustment expenses, and maintenance costs exceeds related future premiums under contract for all lines of

business. Anticipated investment income is not considered for purposes of computing the premium deficiency.

Losses recognized as a premium deficiency result in a beneficial effect in subsequent periods as operating losses

under these contracts are charged to the liability previously established. There were no premium deficiency

60