Humana 2002 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2002 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

through February 26, 2003, we had purchased 2.2 million more shares for an aggregate purchase price of

$20.8 million, or $9.31 per share. The total remaining share repurchase authorization as of February 26, 2003

was $5.2 million.

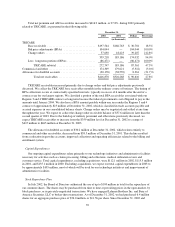

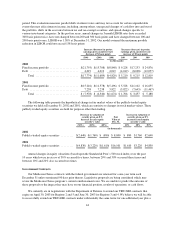

Debt

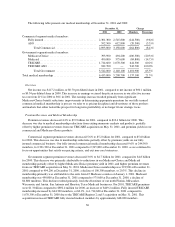

The following table presents our short-term and long-term debt outstanding at December 31, 2002 and 2001:

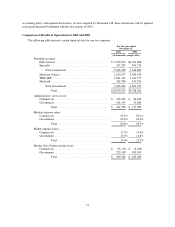

December 31,

2002 2001

(in thousands)

Short-term debt:

Conduit commercial paper financing program ............................... $265,000 $263,000

Long-term debt:

Seniornotes .......................................................... $334,368 $309,789

Other long-term borrowings ............................................. 5,545 5,700

Total long-term debt ............................................... $339,913 $315,489

Senior Notes

The $300 million 7¼% senior, unsecured notes are due August 1, 2006.

In order to hedge the risk of changes in the fair value of our $300 million 7¼% senior notes attributable to

fluctuations in interest rates, we entered into interest rate swap agreements. Interest rate swap agreements, which

are considered derivatives, are contracts that exchange interest payments on a specified principal amount, or

notional amount, for a specified period. Our interest rate swap agreements exchange the 7¼% fixed interest rate

under our senior notes for a variable interest rate, which was 3.06% at December 31, 2002. The $300 million

swap agreements mature on August 1, 2006, and have the same critical terms as our senior notes. Changes in the

fair value of the 7¼% senior notes and the swap agreements due to changing interest rates are assumed to offset

each other completely, resulting in no impact to earnings from hedge ineffectiveness.

Our swap agreements are recognized in our consolidated balance sheet at fair value with an equal and

offsetting adjustment to the carrying value of our senior notes. The fair value of our swap agreements are

estimated based on quoted market prices of comparable agreements and reflects the amounts we would receive

(or pay) to terminate the agreements at the reporting date. At December 31, 2002, the $34.9 million fair value of

our swap agreements is included in other long-term assets. Likewise, the carrying value of our senior notes has

been increased $34.9 million to its fair value. The counterparties to our swap agreements are major financial

institutions with which we also have other financial relationships.

Credit Agreements

We maintain two unsecured revolving credit agreements consisting of a $265 million, 4-year revolving

credit agreement and a $265 million, 364-day revolving credit agreement with a one-year term out option. A one

year term out option converts the outstanding borrowings, if any, under the credit agreement to a one year term

loan upon expiration. The 4-year revolving credit agreement expires in October 2005. In October 2002, we

renewed the 364-day revolving credit agreement which expires in October 2003, unless extended.

There were no balances outstanding under either agreement at December 31, 2002. Under these agreements,

at our option, we can borrow on either a competitive advance basis or a revolving credit basis. The revolving

credit portion of both agreements bear interest at either a fixed rate or floating rate based on LIBOR plus a

spread. The spread, which varies depending on our credit ratings, ranges from 80 to 125 basis points for our

4-year agreement, and 85 to 137.5 basis points for our 364-day agreement. We also pay an annual facility fee

40