Humana 2002 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2002 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

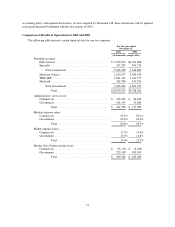

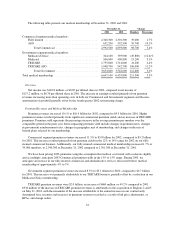

|

|

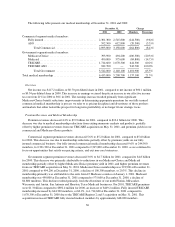

Divestitures

During 2000, we completed transactions to divest our workers’ compensation, north Florida Medicaid and

Medicare supplement businesses. We estimated and recorded a $117.2 million loss in 1999 related to these

divestitures. There was no subsequent change in the estimated loss. Divested assets, consisting primarily of

investment securities and reinsurance recoverables, totaled $651.9 million. Divested liabilities, consisting

primarily of workers’ compensation and other reserves, totaled $437.6 million. Cash proceeds received in 2000

were $97.1 million, net of direct transaction costs. Revenue associated with these businesses prior to divestiture

for 2000 totaled $102.9 million or less than 1% of our consolidated 2000 revenues. Pretax losses totaled

$8.4 million in 2000 related to these businesses.

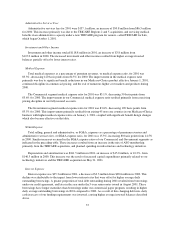

Recently Issued Accounting Pronouncements

On January 1, 2003, we adopted Statement of Financial Accounting Standards No. 146, Accounting for Exit

or Disposal Activities, or Statement 146. Statement 146 addresses the recognition, measurement, and reporting of

costs that are associated with exit and disposal activities, including certain lease termination costs and severance-

type costs under a one-time benefit arrangement rather than an ongoing benefit arrangement or an individual

deferred-compensation contract. Statement 146 requires liabilities associated with exit and disposal activities to

be expensed as incurred and will impact the timing of recognition for exit or disposal activities that are initiated

after December 31, 2002. The effect of the adoption is dependent on exit or disposal activities, if any, initiated

after December 31, 2002.

In November 2002, the Financial Accounting Standards Board, or FASB, issued FASB Interpretation

No. 45, Guarantor’s Accounting and Disclosure Requirements for Guarantees, Including Indirect Guarantees of

Indebtedness of Others, an interpretation of FASB Statements No. 5, 57, and 107 and Rescission of FASB

Interpretation No. 34, or FIN 45. Fin 45 requires that upon issuance of a guarantee, the entity must recognize a

liability for the fair value of the obligation it assumes under that guarantee. FIN 45 requires disclosure about each

guarantee even if the likelihood of the guarantor’s having to make any payments under the guarantee is remote.

The provisions for initial recognition and measurement are effective on a prospective basis for guarantees that are

issued or modified after December 31, 2002. We do not expect the adoption of the recognition provision of

FIN 45 will have a material impact on our financial position, results of operations or cash flows. The disclosure

provisions of FIN 45 are effective for our December 31, 2002 financial statements. See “Liquidity” section and

Note 12 in our consolidated financial statements for guarantee disclosures.

In January 2003, the FASB issued Interpretation No. 46, Consolidation of Variable Interest Entities, an

interpretation of ARB 51, or FIN 46. The primary objectives of FIN 46 are to provide guidance on the

identification of entities for which control is achieved through means other than through voting right (variable

interest entities, or VIEs) and how to determine when and which business enterprise should consolidate the VIE

(the primary beneficiary). The provisions of FIN 46 are effective immediately for VIEs created after January 31,

2003 and no later than July 1, 2003 for VIEs created before February 1, 2003. In addition, FIN 46 requires that

both the primary beneficiary and all other enterprises with a significant variable interest make additional

disclosure in filings issued after January 31, 2003. The adoption of FIN 46 is not expected to have a material

impact on our financial position, results of operations or cash flows.

In January 2003, the FASB issued Statement No. 148, Accounting for Stock-Based Compensation—

Transition and Disclosure, or Statement 148. This Statement amends FASB Statement No. 123, Accounting for

Stock-Based Compensation, to provide alternative methods of transition for a voluntary change to the fair value

based method of accounting for stock-based employee compensation. In addition, Statement 148 amends the

disclosure requirements of Statement 123 to require prominent disclosures in both annual and interim financial

statements about the method of accounting for stock-based employee compensation and the effect of the method

used on reported results. See Notes 2 and 9 in our consolidated financial statements for our stock option

30