Humana 2002 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2002 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

Humana Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

At December 31, 2002, we had approximately $108.8 million of capital losses to carryforward, primarily

related to the sale of our workers’ compensation business in 2000. These capital loss carryforwards, if unused to

offset future capital gains, will expire in 2005. A valuation allowance has been established for a portion of these

deferred tax assets. During 2002, the capital loss valuation allowance was increased by $24.5 million after we

reevaluated probable capital gain realization in the allowable carryforward period based upon our capital gain

experience beginning in 2000 and consideration of alternative tax planning strategies.

Based on our historical taxable income record and estimates of future capital gains and profitability, we

have concluded that future operating income and capital gains will be sufficient to give rise to tax expense and

capital gains to recover all deferred tax assets, net of the valuation allowance.

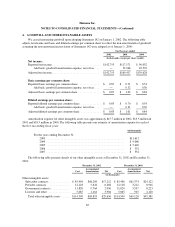

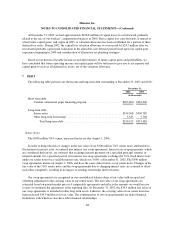

7. DEBT

The following table presents our short-term and long-term debt outstanding at December 31, 2002 and 2001:

December 31,

2002 2001

(in thousands)

Short-term debt:

Conduit commercial paper financing program ....................... $265,000 $263,000

Long-term debt:

Seniornotes .................................................. $334,368 $309,789

Other long-term borrowings ..................................... 5,545 5,700

Total long-term debt ....................................... $339,913 $315,489

Senior Notes

The $300 million 7¼% senior, unsecured notes are due August 1, 2006.

In order to hedge the risk of changes in the fair value of our $300 million 7¼% senior notes attributable to

fluctuations in interest rates, we entered into interest rate swap agreements. Interest rate swap agreements, which

are considered derivatives, are contracts that exchange interest payments on a specified principal amount, or

notional amount, for a specified period. Our interest rate swap agreements exchange the 7¼% fixed interest rate

under our senior notes for a variable interest rate, which was 3.06% at December 31, 2002. The $300 million

swap agreements mature on August 1, 2006, and have the same critical terms as our senior notes. Changes in the

fair value of the 7¼% senior notes and the swap agreements due to changing interest rates are assumed to offset

each other completely, resulting in no impact to earnings from hedge ineffectiveness.

Our swap agreements are recognized in our consolidated balance sheet at fair value with an equal and

offsetting adjustment to the carrying value of our senior notes. The fair value of our swap agreements are

estimated based on quoted market prices of comparable agreements and reflects the amounts we would receive

(or pay) to terminate the agreements at the reporting date. At December 31, 2002, the $34.9 million fair value of

our swap agreements is included in other long-term assets. Likewise, the carrying value of our senior notes has

been increased $34.9 million to its fair value. The counterparties to our swap agreements are major financial

institutions with which we also have other financial relationships.

68