Humana 2002 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2002 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

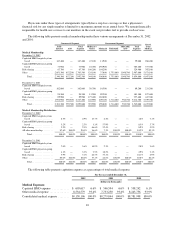

|

|

Health Care Reform

There continue to be diverse legislative and regulatory initiatives at both the federal and state levels to

address aspects of the nation’s health care system.

Federal

In 2000, Congress passed the Medicare, Medicaid and State Childrens Health Benefits Improvement and

Protection Act, or BIPA, amending certain provisions of the Balanced Budget Act of 1997, and certain provisions

of the Medicare, Medicaid and State Children’s Health Insurance Program Balanced Budget Refinement Act of

1999. The Balanced Budget Act changed the way health plans are compensated for Medicare members by

eliminating over five years amounts paid for graduate medical education, increasing the blend of national cost

factors applied in determining local reimbursement rates over a six-year phase-in period and directing CMS to

implement a risk adjusted mechanism on its monthly member payment to Medicare plans over the same period.

These changes have had the effect of reducing reimbursement in high cost metropolitan areas with a large

number of teaching hospitals. Congress has subsequently lengthened this timetable to allow the risk adjusted

mechanism to be fully implemented by 2007. BIPA, among other things, enacted modest increases to the

payment formula for Medicare+Choice plans. While we believe that these increases and modifications restore

some Medicare+Choice reimbursement, pending legislative and regulatory initiatives could cause us to again

consider increasing enrollee out-of-pocket costs, modifying benefits or exiting markets. On January 1, 2002, we

exited our Medicare product in 5 counties in Kentucky and 1 county in Illinois affecting approximately

22,000 members. On January 1, 2003, we exited certain counties in several of our markets, affecting about

10,000 members. These county exits were the result, in part, of lower CMS reimbursement rates. We are working

with CMS to develop other alternative offerings. For example, we are participating in a Medicare+Choice pilot

program offering a private fee-for-service product in DuPage County, Illinois and a PPO product in Pinellas

County, Florida.

On November 21, 2000, the Department of Labor published its final regulation on claims and appeals

review procedures under ERISA. The claims procedure regulation applies to all employee benefit plans governed

by ERISA, whether benefits are provided through insurance products or are self-funded. As a result, the new

claims and appeals review regulation impacts nearly all employer and union-sponsored health and disability

plans, except church and government plans. Similar to legislation recently passed by many states, the new ERISA

claims and appeals procedures impose shorter and more detailed procedures for processing and reviewing claims

and appeals. According to the Department of Labor, however, its ERISA claims and appeals regulation does not

preempt state insurance and utilization review laws that impose different procedures or time lines, unless

complying with the state law would make compliance with the new ERISA regulation impossible. Unlike its state

counterparts, the ERISA claims and appeals rule does not provide for independent external review to decide

disputed medical questions. Instead, the federal regulation will generally make it easier for claimants to avoid

state-mandated internal and external review processes and to file suit in federal court. The new ERISA claims

and appeals rules generally became effective July 1, 2002 or the first day of the first plan year beginning after

July 1, 2002, whichever is later. In any case, health plans must comply with the new rules with respect to all

claims filed on or after January 1, 2003.

The Health Insurance Portability and Accountability Act of 1996, or HIPAA, includes administrative

provisions directed at simplifying electronic data interchange through standardizing transactions, establishing

uniform health care provider, payer and employer identifiers and seeking protections for confidentiality and

security of patient data. Under the new HIPAA standard transactions and code sets rules, we must make

significant systems enhancements and invest in new technological solutions. The compliance date for standard

transactions and code sets rules has been extended to October 17, 2003 based on our submission of a compliance

plan, including work plan and implementation strategy to the Secretary of Health and Human Services. Under the

new HIPAA privacy rules, by April 14, 2003 we must comply with a variety of requirements concerning the use

and disclosure of individuals’ protected health information, establish rigorous internal procedures to protect

health information and enter into business associate contracts with those companies to whom protected health

15