Humana 2002 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2002 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

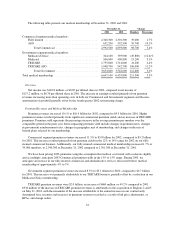

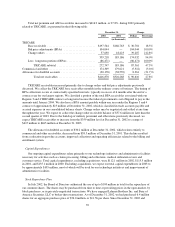

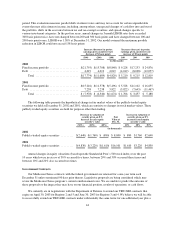

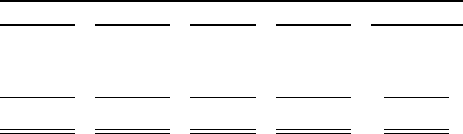

Contractual Obligations and Off-Balance Sheet Arrangements

We are contractually obligated to make payments for years subsequent to December 31, 2002 as follows:

Payments Due by Period

Total 1Year 2-3 Years 4-5 Years After 5 Years

(in thousands)

Debt....................................... $604,913 $265,623 $ 1,283 $335,482 $ 2,525

Operating leases ............................. 264,491 63,471 87,990 54,989 58,041

Total .................................. $869,404 $329,094 $89,273 $390,471 $60,566

Debt payments could be accelerated upon violation of debt covenants. We believe the likelihood of a debt

covenant violation is remote. We lease facilities, computer hardware, and other equipment under long-term

operating leases that are noncancelable and expire on various dates through 2017. We sublease facilities or

partial facilities to third party tenants for space not used in our operations which partially mitigates our operating

lease commitments. An operating lease is a type of off-balance sheet arrangement. Assuming we acquired the

asset, rather than leased, we would have recognized a liability for the financing of these assets. See also Note 12

to the consolidated financial statements.

Our 5-year and 7-year airplane operating leases which are included above provide for a residual value

guarantee of no more than $17.9 million at the end of the lease terms which expire December 29, 2004 for the

5-year leases and January 1, 2010 for the 7-year lease. We have the right to exercise a purchase option with

respect to the leased equipment or the equipment can be sold to a third party. If we decide not to exercise our

purchase option at the end of the lease, we must pay the lessor a maximum amount of $13.1 million related to the

5-year leases and $4.8 million related to the 7-year lease. The amount will be reduced by the net sales proceeds

of the airplanes to a third party. A $3.5 million gain in connection with a 1999 sale/leaseback transaction is being

deferred until the residual value guarantee is resolved at the end of the lease term. We do not believe that we will

have any payment obligation at the end of the lease because we will exercise the purchase obligation, or the net

proceeds from the sale of the airplanes will exceed the maximum amount payable to the lessor.

We have $23.8 million in undrawn letters of credit outstanding at December 31, 2002. Letters of credit

totaling $10.9 million have been issued to ensure our payment to a beneficiary for assumed obligations of our

wholly owned captive insurance subsidiary related to pre-1993 professional liability risks for which the

beneficiary remains directly liable. Other letters of credit totaling $12.9 million were issued to ensure our

payment to various beneficiaries for miscellaneous contractual obligations. These letters of credit renew

automatically on an annual basis unless the beneficiary otherwise notifies us. In February 2003, a $5.0 million

letter of credit supporting miscellaneous contractual obligations of ours expired without renewal. Over the past

10 years, we have not had to fund any letters of credit.

Through indemnity agreements approved by the state regulatory authorities, certain of our regulated

subsidiaries generally are guaranteed by Humana Inc., our parent company, in the event of insolvency for

(1) member coverage for which premium payment has been made prior to insolvency; (2) benefits for members

then hospitalized until discharged; and (3) payment to providers for services rendered prior to insolvency.

Other Liquidity Factors

Our investment grade credit rating at December 31, 2002 was Baa3 according to Moody’s Investors

Services, Inc., or Moody’s and BBB, according to Standard & Poor’s Corporation, or S&P. A downgrade to Ba2

or lower by Moody’s and BB or lower by S&P would give the counterparty of one of our interest rate swap

agreements with a $100 million notional amount, the right, but not the obligation, to cancel the interest rate swap

agreement. If cancelled, we would pay or receive an amount based on the fair market value of the swap

42