Sysco 2013 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2013 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

|

|

SYSCO CORPORATION-Form10-K34

PARTII

ITEM7Management’s Discussion and Analysis ofFinancial Condition and Results of Operations

Commercial Paper and Revolving Credit Facility

We have a Board-approved commercial paper program allowing us to issue short-term unsecured notes in an aggregate amount not to exceed $1.3billion.

In December2011, we terminated our previously existing revolving credit facility that supported the company’s U.S. and Canadian commercial paper

programs. At the same time, Sysco and one of its subsidiaries, Sysco International, ULC, entered into a new $1.0billion credit facility supporting the

company’s U.S. and Canadian commercial paper programs. This facility provides for borrowings in both U.S. and Canadian dollars. Borrowings by Sysco

International, ULC under the credit agreement are guaranteed by Sysco, and borrowings by Sysco and Sysco International, ULC under the credit agreement

are guaranteed by all the wholly-owned subsidiaries of Sysco that are guarantors of the company’s senior notes and debentures. The original facility in

the amount of $1.0billion expires on December29,2016. In December2012, a portion of the facility was extended for an additional year. This extended

facility, which expires on December29,2017, is for $925.0million of the original $1.0billion facility, but is subject to further extension.

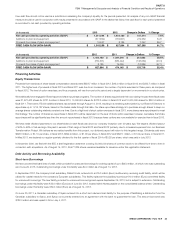

As of June29,2013, commercial paper issuances outstanding were $95.5million. As of August14,2013, commercial paper issuances outstanding

were $76.0million. During scal 2013,2012 and 2011, aggregate outstanding commercial paper issuances and short-term bank borrowings ranged from

approximately zero to $330.0million, zero to $563.1million, and zero to $330.3million, respectively. During scal 2013,2012 and 2011, our aggregate

commercial paper issuances and short-term bank borrowings had a weighted average interest rate of 0.16%, 0.16% and 0.25%, respectively.

Fixed Rate Debt

Included in current maturities of long-term debt as of June29,2013 are the 4.6% senior notes totaling $200.0million, which mature in March2014. It is

our intention to fund the repayment of these notes at maturity through cash on hand, cash ow from operations, issuances of commercial paper, senior

notes or a combination thereof.

In February2012, we led with the SEC an automatically effective well-known seasoned issuer shelf registration statement for the issuance of an indeterminate

amount of common stock, preferred stock, debt securities and guarantees of debt securities that may be issued from time to time.

In June2012, we repaid the 6.1% senior notes totaling $200.0million at maturity utilizing a combination of cash ow from operations and commercial

paper issuances.

In May2012, we entered into an agreement with a notional amount of $200.0million to lock in a component of the interest rate on our then forecasted debt

offering. We designated this derivative as a cash ow hedge of the variability in the cash out ows of interest payments on a portion of the then forecasted

June2012 debt issuance due to changes in the benchmark interest rate. In June2012, in conjunction with the issuance of the $450.0million senior notes

maturing in scal 2022, we settled the treasury lock, locking in the effective yields on the related debt. Upon settlement, we received cash of $0.7million,

which represented the fair value of the swap agreement at the time of settlement. This amount is being amortized as an offset to interest expense over the

10-year term of the debt, and the unamortized balance is re ected as a gain, net of tax, Accumulated other comprehensive loss.

In June2012, we issued 0.55% senior notes totaling $300.0million due June12,2015 (the 2015 notes) and 2.6% senior notes totaling $450.0million

due June12,2022 (the 2022 notes) under its February2012 shelf registration. The 2015 and 2022 notes, which were priced at 99.319% and 98.722% of

par, respectively, are unsecured, are not subject to any sinking fund requirement and include a redemption provision which allows Sysco to retire the notes

at any time prior to maturity at the greater of par plus accrued interest or an amount designed to ensure that the note holders are not penalized by early

redemption. Proceeds from the notes will be utilized over a period of time for general corporate purposes, which may include acquisitions, re nancing of

debt, working capital, share repurchases and capital expenditures.

In February2013, we repaid the 4.2% senior notes totaling $250.0million at maturity utilizing a combination of cash ow from operations and cash on hand.

In August2013, we entered into an interest rate swap agreement that effectively converted $500million of xed rate debt maturing in scal 2018 to oating

rate debt. This transaction was entered into with the goal of reducing overall borrowing cost and was designated as a fair value hedge against the changes

in fair value of xed rate debt resulting from changes in interest rates.

Total Debt

Total debt as of June29,2013 was $3.0billion of which approximately 88% was at xed rates with a weighted average of 4.7% and an average life of 13

years, and the remainder was at oating rates with a weighted average of 1.4% and an average life of one year. Certain loan agreements contain typical

debt covenants to protect note holders, including provisions to maintain the company’s long-term debt to total capital ratio below a speci ed level. We are

currently in compliance with all debt covenants.

Other

As part of normal business activities, we issue letters of credit through major banking institutions as required by certain vendor and insurance agreements.

In addition, in connection with our audits in certain tax jurisdictions, we have posted of letters of credit in order to proceed to the appeals process. As of

June29,2013, letters of credit outstanding were $42.2million.